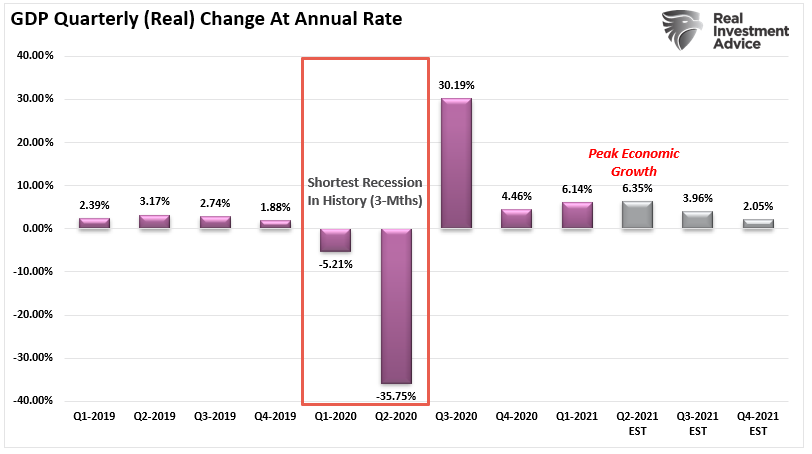

Was the second quarter the peak of economic growth and earnings? If estimates are correct and the year-over-year “base effect” fades, such suggests risk to current earnings estimates.

The chart from a “Grossly Defective Product,” utilizes the Atlanta Fed’s current estimates for Q2-2021 GDP. The full-year estimates are from JP Morgan. Notably, the economy quickly slows to 2% heading into 2022.

Estimates of growth are misleading for two reasons.

- As shown above, growth gets reported as an “annualized” rate. The 6.4% growth in Q2 assumes the 1.6% actual growth will repeat over the next 3-quarters. (1.6% x 4-quarters = 6.4%) Historically, such a feat never occurs.

- Secondly, the surge in Q2 growth is a function of the contraction in Q2-2020. As such, the growth rate gets exacerbated. (This is the “base effect.”) That growth rate will fall sharply in Q3 as the base effect reverses.

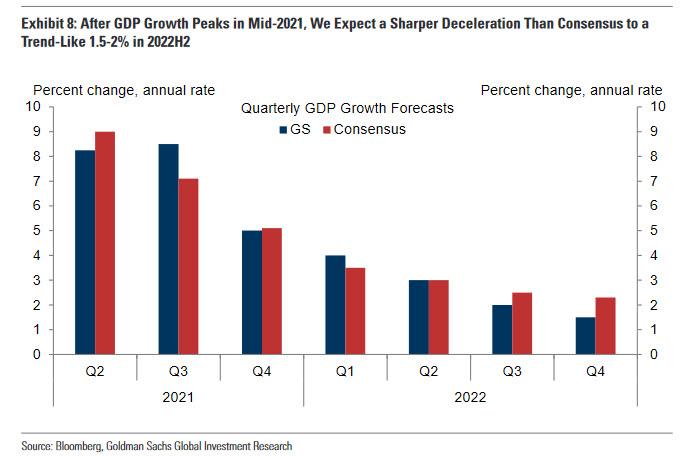

Such was a point made by Goldman Sacks recently, as noted by Zerohedge:

“Goldman cut its 2021 second half consumption growth forecast, resulting in 1% downgrade to its GDP growth forecasts for Q3 and Q4 to +8.5% and +5.0%, respectively. Such is because it is becoming apparent the service sector recovery in the US is unlikely to be as robust as the bank had expected. That is odd considering the trillions in monetary and fiscal stimulus that have entered into the economy.

But while Goldman’s expected 2021 slowdown is manageable, it gets far worse in 2022, when the sluggishness is expected to truly hammer the growth rate, which Goldman now expected to shrink to a trend-like 1.5% – 2% by the second half of 2022, a far ‘sharper deceleration than consensus expects.”‘

While Goldman’s outlook may shock the more “effervescent bulls,” it aligns well with our previous analysis over the past 12-months.

A Decline In Spending

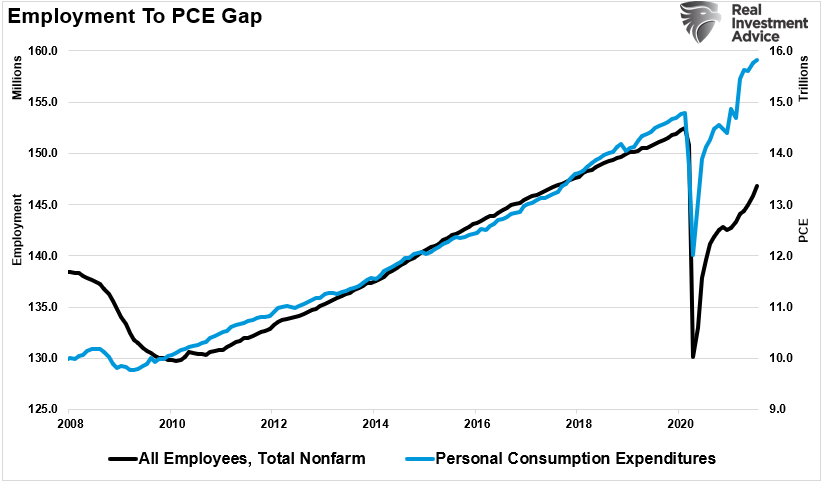

The immediate boost to economic growth in Q3-2020 through Q2-2021 was the massive amount of Federal expenditures. From the expansion of unemployment benefits to direct checks to households, the increase in consumption was evident. However, such did not translate to more robust economic growth or employment. The chart below is from “Inflation Doesn’t Come From Artificial Growth.”

“Sustainable, demand-driven inflation, requires sustainable wages to support higher prices. Due to the artificial stimulus, personal consumption expenditures are 7% higher than pre-pandemic norms while employment is ~6-million jobs lower.”

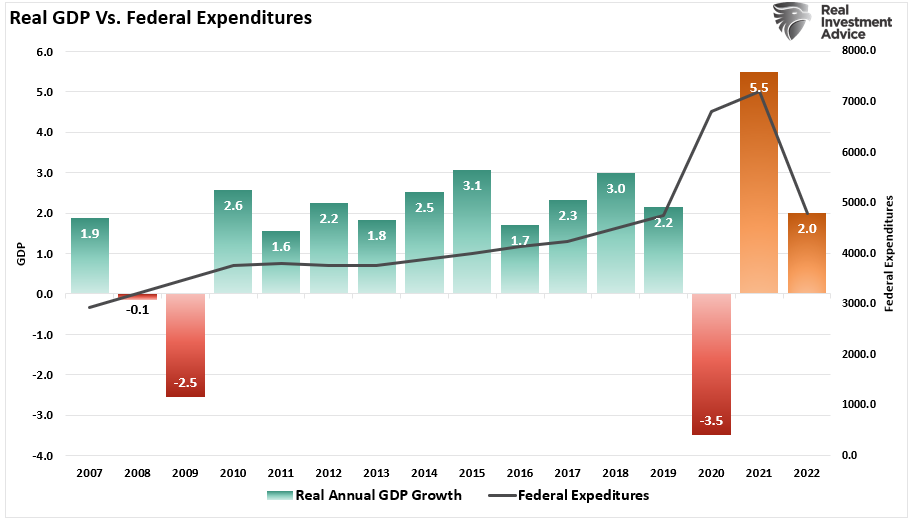

The challenge now is that Federal spending will decline sharply. While there may be an eventual infrastructure plan, that spending will get spread over 10-years. More importantly, as we will review next, Federal spending harms economic growth.

Given the decline in Federal spending and the potential taper of “quantitative easing,“ a reversal in growth is evident. The only question is if current estimates remain overly optimistic.

However, let’s review the previous analysis on why Federal spending has minimal impacts on growth.

A Negative Multiplier

There is almost no multiplier effect with Federal Spending. The study, linked article above, by the Mercatus Center at George Mason University by economists Jones and De Rugy states:

“The multiplier looks at the return in economic output when the government spends a dollar. If the multiplier is above one, it means that government spending draws in the private sector and generates more private consumer spending, private investment, and exports to foreign countries. If the multiplier is below one, the government spending crowds out the private sector, hence reducing it all.

The evidence suggests that government purchases probably reduce the size of the private sector as they increase the size of the government sector. On net, incomes grow, but privately produced incomes shrink.”

Personal consumption expenditures and business investment are vital inputs into the economic equation. As such, we should not ignore the reduction of privately produced incomes. Furthermore, according to the best available evidence, the study found:

“There are no realistic scenarios where the short-term benefit of stimulus is so large that the government spending pays for itself. In fact, the positive impact is small, and much smaller than economic textbooks suggest.”

Notably, politicians spend money based on political ideologies rather than sound economic policy. Therefore, the findings should not surprise you. However, the conclusion of the study is most telling.

“If you think that the Federal Reserve’s current monetary policy is reasonably competent, then you actually shouldn’t expect the fiscal boost from all that spending to be large. In fact, it could be close to zero.

This is, of course, all before taking future taxes into account. When economists like Robert Barro and Charles Redlick studied the multiplier, they found once you account for future taxes required to pay for the spending, the multiplier could be negative.”

Not Surprising

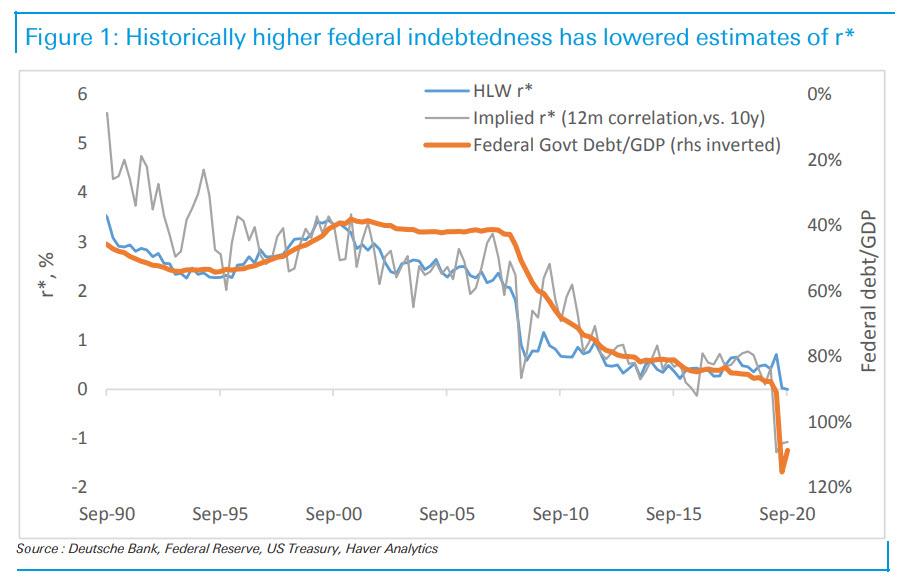

What should not surprise you is that non-productive debt does not create economic growth. As Stuart Sparks of Deutsche Bank noted previously:

“History teaches us that although investments in productive capacity can in principle raise potential growth and r* in such a way that the debt incurred to finance fiscal stimulus is paid down over time (r-g<0), it turns out that there is little evidence that it has ever been achieved in the past.

The chart below illustrates that a rising federal debt as a percentage of GDP has historically been associated with declines in estimates of r* – the need to save to service debt depresses potential growth. The broad point is that aggressive spending is necessary, but not sufficient. Spending must be designed to raise productive capacity, potential growth, and r*. Absent true investment, public spending can lower r*, passively tightening for a fixed monetary stance.”

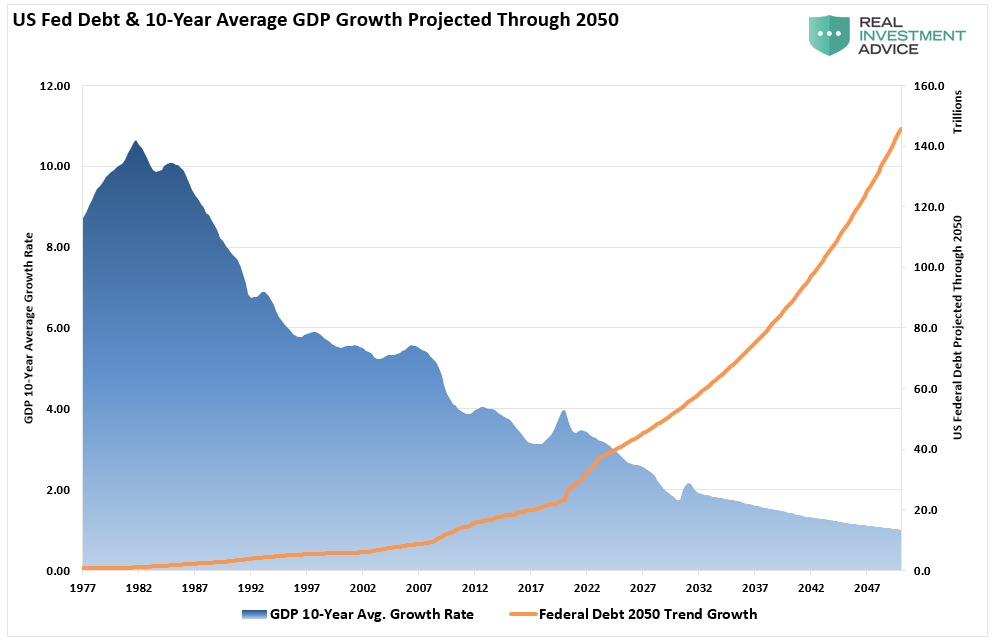

A long-term historical look confirms the same. Since 1977, the 10-year average GDP growth rate steadily declined as debt increased. Thus, using the historical growth trend of GDP, the increase of debt will lead to slower economic growth rates in the future.

Given the historical correlation of debt to GDP growth, such suggest future outcomes will be no different.

A Revision To Earnings

Given that corporate earnings and profits are derived ultimately from economic activity (personal consumption and business investment), it is unlikely the currently lofty expectations will get met.

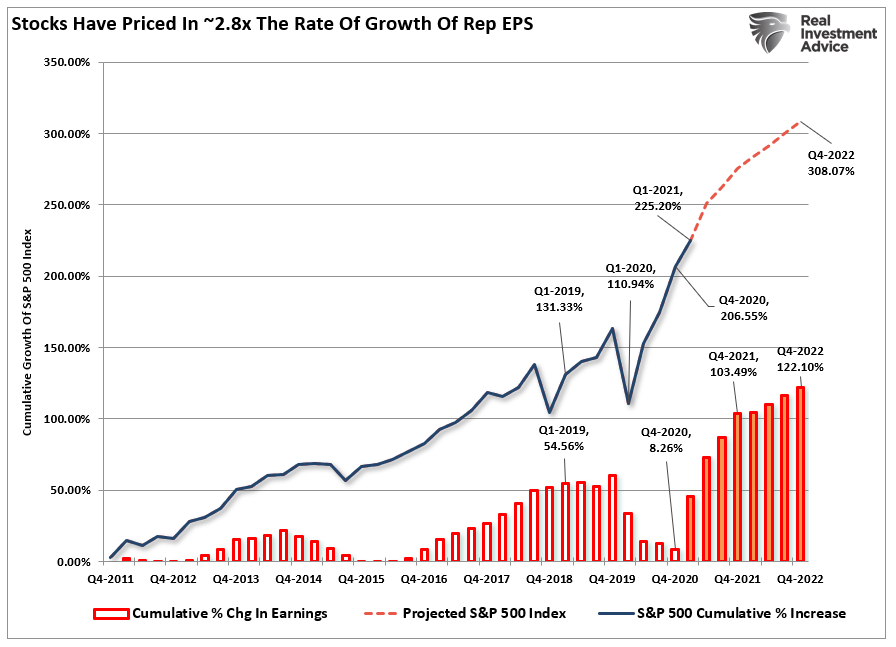

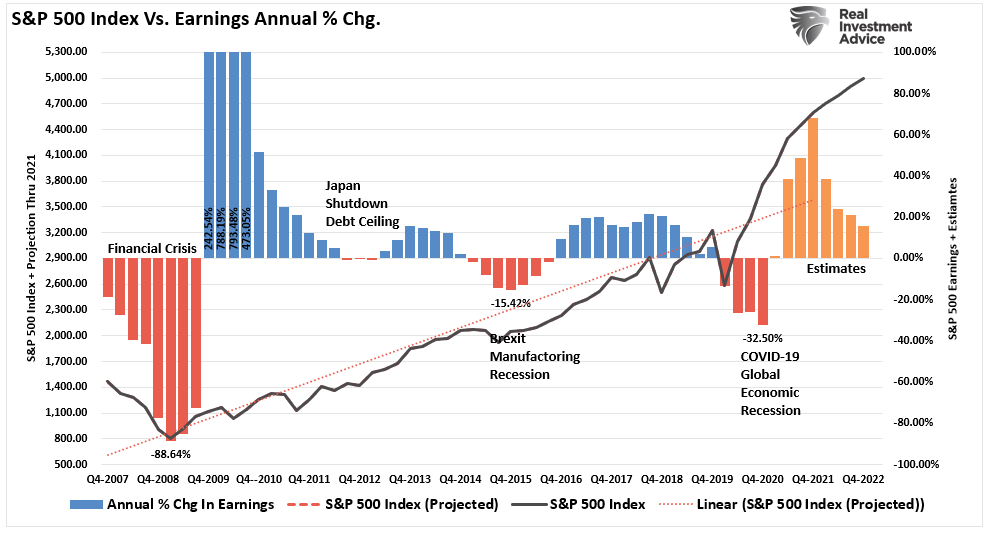

The problem for investors currently. Analysts’ assumptions are always high, and markets are trading at more extreme valuations, which leaves little room for disappointment. Using analyst’s price target assumptions of 4700 for 2020 and current earnings expectations, the S&P is trading 2.6x earnings growth.

Such puts the current P/E at 25.6x earnings in 2020, which is still expensive by historical measures.

That also puts the S&P 500 grossly above its linear trend line as earnings growth begins to revert.

Through the end of this year, companies will guide down earnings estimates for a variety of reasons:

- Economic growth won’t be as robust as anticipated.

- Potentially higher corporate tax rates could reduce earnings.

- The increased input costs due to the stimulus can’t get passed on to consumers.

- Higher interest rates increasing borrowing costs which impact earnings.

- A weaker consumer than currently expected due to reduced employment and weaker wages.

- Global demand weakens due to a stronger dollar impacting exports.

Such will leave investors once again “overpaying” for earnings growth that fails to materialize.

Conclusion

While none of this suggests the market will “crash” tomorrow, it is supportive of the idea that future returns will be substantially weaker in the future.

There are few, if any, Wall Street analysts expecting a recession currently. Instead, most are confident of a forthcoming economic growth cycle. Yet, at this time, there are few catalysts supportive of such a resurgence.

- Economic growth outside of China remains weak

- Employment growth is going to slow.

- There is no massive disaster currently to spur a surge in government spending and reconstruction.

- There isn’t another stimulus package like tax cuts to fuel a boost in corporate earnings.

- With the deficit expected to push $4 Trillion, there will only be an incremental boost from additional deficit spending this year.

- Unfortunately, it is also just a function of time until a recession occurs.

Wall Street is notorious for missing significant turning points in markets and leaving investors scrambling for the exits.

While no one on Wall Street told you to be wary of the markets in 2018, we did. Of course, we also warned you early in 2020. but it largely fell on deaf ears as “F.O.M.O.” clouded basic investment logic.

It is pretty likely before we get to the end of 2022, it will happen again.