It’s happening again. The Fed is threatening the financial markets with tighter money, and those markets are reacting like addicts being shoved through the front door of a rehab center. They’re not happy, and they have good reason – actually two good reasons – to be alarmed.

First, tighter monetary policy will blow up all the trades that depend on perfection going forward – which is to say pretty much all the trades currently in place in stocks, bonds, real estate, cryptos, you name it.

Second, the markets know this is all just a game, and can’t believe they’re being forced to play yet again. Going back to at least the 1990s, tight money has always led to crises of one type or another, and the Fed has always panicked (after a humiliating period of indecision) and reversed course, fixing the junkie a nice full syringe of monetary heroin.

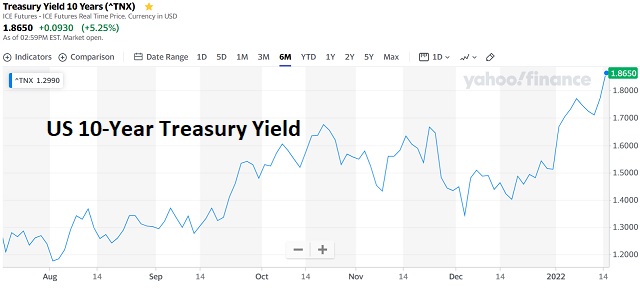

So the question, as always, is, What’s the number? How far will interest rates have to rise and/or stocks fall before the Fed caves? That will only be clear in retrospect, of course, but it’s a safe bet that current trends, if allowed to continue, will take us there shortly. Consider the 10 year Treasury chart, which screams “break-out” as it nears the 2 handle. Even if 2% isn’t The Number, it’s definitely headline material and as such might have an exaggerated impact on stock prices.

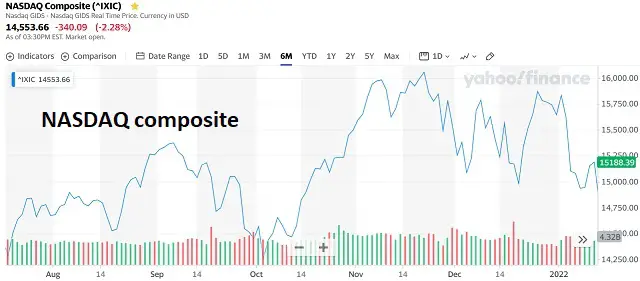

Speaking of wildly overvalued tech stocks, the NASDAQ is behaving erratically, as one would expect with interest rates looking spiky. So far, though, Big Tech has held up pretty well and even after today’s brutal beat-down remains above its 6-month lows. Here again, there is a number that will do the trick. It’s just somewhere below the current level.

Using the above educated guesses, it’s possible to sketch out a year-ahead scenario where some important interest rates have a few more big weeks and pierce their overhead handles, causing tech stocks to drop and pull down the rest of the equity complex. And there we’ll be, enduring simultaneous bear markets in stocks and bonds, with – thanks to mortgage rates being tied to the 10-year yield – houses not far behind. That’s a triple-threat the Fed has never, not once, been able to withstand in the living memories of most American voters.

Imagine the reaction of a whole generation of traders who have never heard a firm “no” from the monetary authorities, suddenly confronted with all their trades going wrong at once. You probably can’t imagine it, but the Fed emphatically can. Which is why they can never, ever let it happen. Even in a world of double-digit inflation.