Business Insider published a piece this week called “China’s hopes of becoming the world’s largest economy are hitting a major roadblock“:

China’s economy is growing at its slowest pace in nearly three decades, and some economists say the worst is yet to come.

Growth potential in China is expected to slow to 5.5% from the current level of 6.5% between 2021 and 2025, according to new estimates from analysts at JPMorgan. That could fall to 4.5% by 2030, a pace that would make it difficult to surpass the US as the largest economy.

“This means that China will remain the second largest economy much longer than expected,” the analysts said in a research note Wednesday. “The transition to slower potential growth could be volatile and requires balancing reforms to move to a more domestically driven growth model with deleveraging and public-sector restructuring.”

Officials in Beijing have sought to shore up confidence through a series of stimulus measures rolled out in recent months, including tax cuts, changes to the amount of cash banks must hold as reserves, and various incentives to boost spending.

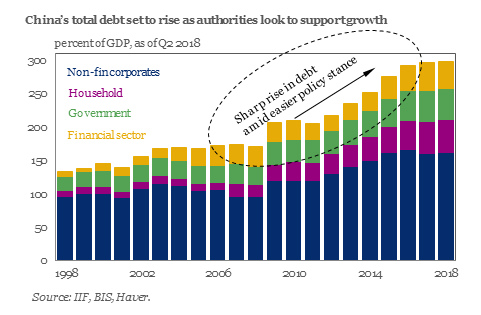

But those programs could have little room to expand in an economy that has struggled to crack down on relatively high levels of debt in recent years. In 2018, China’s debt-to-gross-domestic-product ratio climbed above 250%.

A January New York Times piece explains how China is no longer the growth engine that it once was:

For years, no matter what was happening elsewhere, global companies bet billions upon billions of dollars that China’s consumers would keep spending money.

Now, just when the world economy could use their financial firepower, they are no longer so quick to open their wallets.

The latest sign of a slowdown in spending in China came Wednesday, when Apple unexpectedly slashed its financial forecast, citing disappointing iPhones sales in the country. The weakness followed reams of other data — declining car sales, lagging retail spending, a slumping property market, a tougher job market — that suggest Chinese consumers may be losing their once unshakable confidence.

That could have a big impact on a world looking for engines of growth, on companies that counted on China’s continuing expansion and on global investors who have long viewed China as a steady source of profits.

As I have been warning for several years, China is experiencing a credit and asset bubble like Japan was in the 1980s. China’s powerful credit expansion in the past decade (as the chart below shows) is one of the main reasons why the global economy recovered from the Great Recession. China’s credit bubble of the past decade will prove to be a one-shot deal – in the next global economic downturn, there won’t be another large economy like China to binge on debt and create a temporary growth party that bails everyone else out.

An economic stagnation or slowdown in China is the least of our worries, I’m afraid. I am worried about a full-blown popping of their credit and asset bubble (like Japan in the early-1990s), which would reverberate around the world. In that scenario, Western exports to China would plunge, commodity-exporting economies from Australia to emerging markets would suffer, and the global economy would experience another severe recession if not an outright depression. The world has played with fire over the past decade and it’s just a matter of time before we all pay the price.