Back in 2011, former HUD and Freddie Mac Chief Economist Michael Lea wrote an article entitled “Do We Need the 30-Year Fixed-Rate Mortgage?” We argued that plain vanilla ARMs (without teaser rates and other tricked-up products during the housing bubble) offered consumers advantages over fixed-rate mortgages (FRMs).

The answer to that question has just been answered: adjustable rate mortgages as a percentage of all mortgages has fallen to its lowest level since financial crisis and The Great Recession.

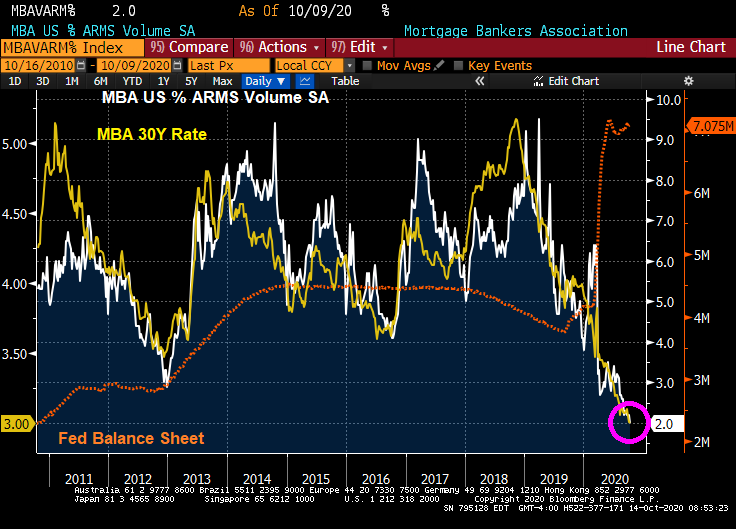

The reason? First, consumers flock towards ARMs when mortgage rates decline. In part, thanks to The Federal Reserve’s interest rate policies (as shown below).

Lea and I argued that there are certain advantages to ARMs for consumers (see paper at link), such as a lower mortgage rate on average.

Also, empirically mortgage rates on average fall negating the “fear factor” of mortgage rates rising on an ARM reset.

The latest mortgage applications volumes from the Mortgage Bankers Association shows that the ARM% has dwindled to 2%.

Yes, it is A Farewell To ARMs, but not as Ernest Hemingway envisioned.