It was a doozie, but it shouldn’t have come as a surprise. Here’s why.

By Don Quijones, Spain, UK, & Mexico, editor at WOLF STREET.

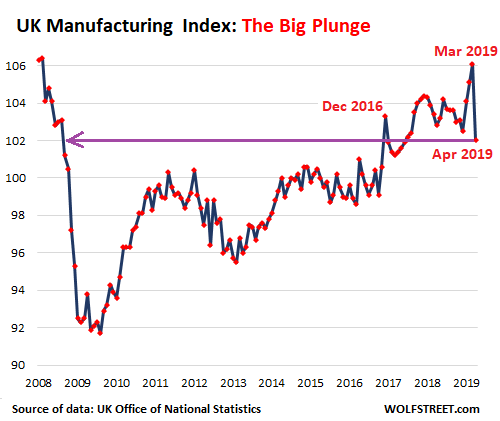

Production output in the UK dropped by 2.7% in April from March, and GDP fell by 0.4% in just one month, according to the latest figures by the Office of National Statistics. The manufacturing sector provided the largest contribution to the downturn, with the manufacturing index plunging 3.9% in April, from March, its biggest monthly fall since June 2002. In April, after three months of sharp increases, it had almost finally reached its pre-Financial-Crisis peak. The plunge in April took the index down 0.8% for the 12-month period, and took it back to 2017 levels.

The data was seized upon by pro-remain media outlets as evidence of the crushing impact of Brexit on the UK economy. The Guardian called it a “Brexit hangover” while a headline in The Independent shrieked that a “Brexit paralysis” has set in after the economy “shrinks by four times as much as predicted.”

But it was always inevitable that April, the month after the official, and now come-and-gone, Brexit date of March 29 would be a bad month for the UK economy. Companies had stockpiled record amounts of inventories for months on end ahead of the Brexit date, which would naturally cause production and business and the economy in general to increase before Brexit and plunge for about a month or two after.

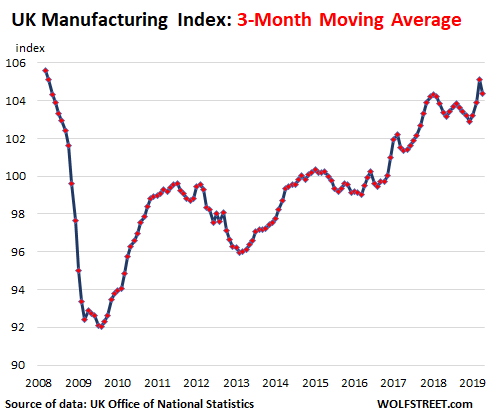

The April figures, if taken in isolation, may seem semi-cataclysmic and perhaps even deserving of the doom-and-gloom laden vernacular employed by certain media, but the three-month moving average shows a different story: A big boost from late 2018 through March, and then a dip in April that unwound only half of the prior month’s gain:

The hardest hit sector during April’s downturn, the transport equipment industry, which encompasses motor vehicles, trailers and semi-trailers, saw its manufacturing output plunge by 24%. It’s the largest monthly fall since January 1974 when the UK economy was reeling from the effects of a major global oil crisis. But if you average the data out over the three months from February through April, the contraction is a much less dramatic 2.7%.

These manufacturers had scheduled months ahead of the March 29 hard-Brexit date a shutdown of their manufacturing operations to last a week or more over fears they could not get parts and components from the EU in time, due to border chaos. When Brexit was delayed at the last minute, it was too late to un-schedule the scheduled shutdown.

The three automakers with the largest manufacturing base in the UK — BMW, Jaguar Land Rover, and Honda — had announced in early April that they would close their factories in April from between a week to up to a month to mitigate potential disruption from a no-deal Brexit (we reported on this).

And while auto manufacturing is certainly down in the UK — its output has been falling for 11 straight months — it’s largely the result of slowing demand in key international markets, including the EU, China and the US, as well as the collapse of diesel vehicle sales in the UK. Jaguar Land Rover has been agonized by these conditions for a while.

The automotive manufacturing sector is only a relatively small part of the UK economy. Some European economies are getting hit even harder by the auto slowdown, in particular Germany whose outsized dependence on auto manufacturing for exports quickly becomes a source of weakness when the auto sector goes into decline globally, as is happening right now.

Other manufacturing sectors that performed poorly in April had followed similar strategies to avoid getting caught in border chaos. In April, output in the pharmaceutical products industry shrank by 8.7%, among chemical producers by 5.8%, and among metal producers 4.1%. But like other manufacturers, the had increased production volume sharply in preparation for Brexit chaos that then never came.

Pharmaceutical companies, like automotive manufacturers, spent the months leading up to the UK’s scheduled withdrawal date of March 29 frantically stockpiling goods and trying to bring forward orders. Some manufacturers even brought forward production stoppages normally scheduled for the summer holiday period to April in the hope of minimizing the impact of the UK’s departure from the customs union and single market.

When the withdrawal date was postponed, first to April 12, then to the end of October, many of those companies had fewer orders to fulfill and used some of their stockpiled goods to meet the orders they did have. Manufacturers that had opted to bring their summer shutdown forward suddenly found that not only did they unnecessarily lose millions in forgone production in April but their vulnerability to future shocks has also increased, since it will be much harder for them to justify planning another shutdown for the next deadline, in four and a half months’ time.

This is just one example of the huge costs of the acute uncertainty unleashed when the UK government and parliament decided not to leave the EU on March 29. If anything, the uncertainty is greater today than it was at any other time. Logistics firms on both sides of the English Channel have spent (and earned) billions of pounds and euros helping companies get ready for Brexit, but now no one — not even the UK government — knows whether there will be a Brexit, what form it will take, or when it will happen, if indeed it does.

Companies have little choice but to spend large resources in terms of time, money, and lost opportunity in preparing for complex eventualities that may not end up materializing. The longer this goes on, the more harm it will do. Now another pile of the money is being spent on contingency planning for the next Brexit deadline, which may get punted further into the future anyway. While a no-deal Brexit is still the default option and could be the preferred choice of the next prime minister, the temptation to further extend the deadline as the big day approaches, in classic can-kicking style, will grow.

it will be tough to break the impasse, which is largely the result of the intense unpopularity of the proposed Withdrawal Agreement among both ‘remain’ and ‘leave’ camps. As this uncertainty drags on, the cost, in terms of economic pain for UK-based businesses that are having to prepare for this uncertainty, is likely to be huge. By Don Quijones.