via Zerohedge:

Having been told numerous times that banks “are in far better condition now than before the crisis,” we should not be at all surprised that all major banks passed The Fed’s “adverse scenario” stress test.

As The FT reports, US banks would lose $410bn if there were another severe global recession, but would maintain enough capital to keep lending to companies and individuals, according to US regulators. Eighteen of the country’s largest banks all passed the first round of their annual stress tests on Friday, as Federal Reserve figures showed the US financial services industry is well-enough capitalised to weather a worst-case scenario economic downturn.

Wondering how terrifying the adverse scenario is… well it is certainly a big drop BUT expectations that it will all be forgotten in a couple of years seems a little ambitious if we ever see these kind of collapses again…

Randal Quarles, the vice-chairman of the Fed in charge of banking oversight, said on Friday:

“The results confirm that our financial system remains resilient. The nation’s largest banks are significantly stronger than before the crisis and would be well-positioned to support the economy even after a severe shock.”

So why did The Fed abandon its normalization of the balance sheet?

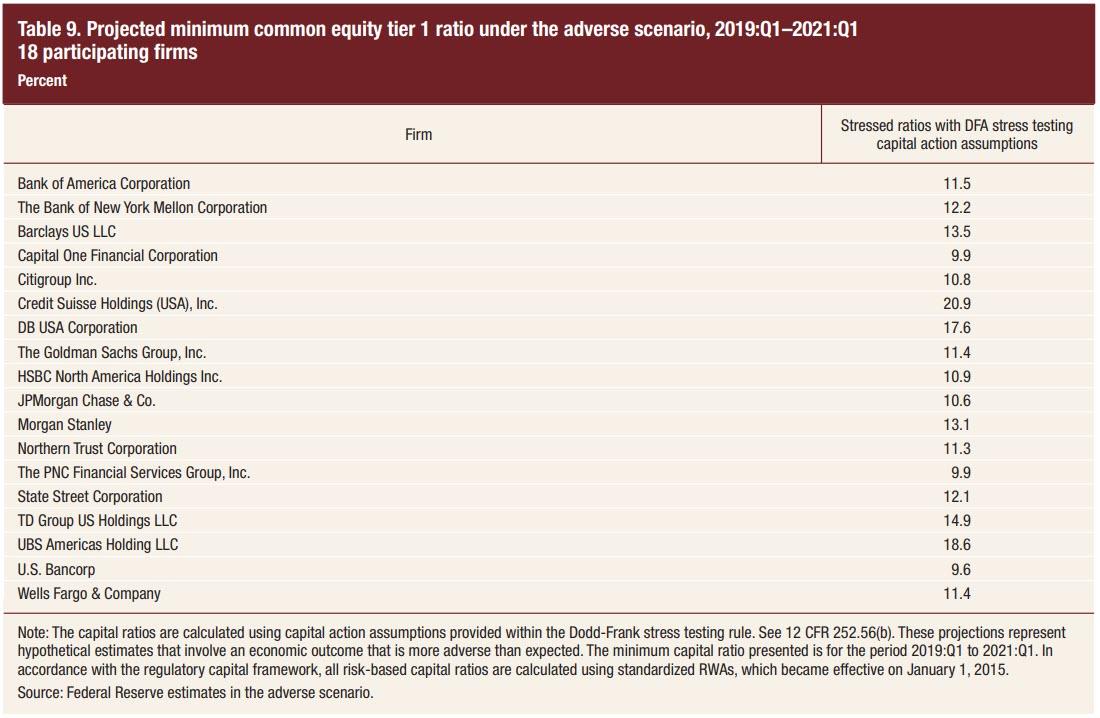

As Bloomberg reports, results posted so far show banks are getting better at coping with what’s become one of the most rigorous supervisory efforts: They maintained a collective common equity Tier 1 ratio that was double the regulatory minimum even at the depths of the theoretical recession. Lenders have been building capital for years, and while this year’s exam was harsher on credit-card loans, trading losses were down from last year at four of the five biggest Wall Street firms.

Goldman Sachs and Morgan Stanley improved on last year’s poor results in the first round of the latest Federal Reserve stress tests, a sign they may have more flexibility to boost payouts to shareholders.

The nation’s largest and most complex banks have strong capital levels that would allow them to stay well above their minimum requirements after being tested against a severe hypothetical recession, according to the results of supervisory stress tests released Friday by the Federal Reserve Board.

The most severe hypothetical scenario projects $410 billion in total losses for the 18 participating bank holding companies. This scenario featured a global recession with the U.S. unemployment rate rising by more than 6 percentage points to 10 percent, accompanied by a large decline in real estate prices and elevated stress in corporate loan markets.

The firms’ aggregate common equity tier 1 capital ratio, which compares high-quality capital to risk-weighted assets, would fall from an actual level of 12.3 percent in the fourth quarter of 2018 to a minimum level of 9.2 percent. Since 2009, the common equity capital at the 18 firms has increased by more than $680 billion.

“The results confirm that our financial system remains resilient,” Vice Chairman Randal K. Quarles said. “The nation’s largest banks are significantly stronger than before the crisis and would be well-positioned to support the economy even after a severe shock.”

Loan losses in this year’s stress test are broadly comparable to those from past years. Credit card loans showed the highest losses, followed by commercial and industrial loans.

Capital is critical to banking organizations, the financial system, and the economy, because it acts as a cushion to absorb losses and helps to ensure that losses are borne by shareholders. The Board uses its own independent projections of losses and incomes for each firm and the results are not forecasts or expected outcomes.

Only the largest and most complex banks were tested this year. As previously announced, smaller and less complex banks were not tested this year and are currently on a two-year cycle, consistent with the Economic Growth, Regulatory Relief, and Consumer Protection Act. The firms tested this year represent about 70 percent of the assets of all banks operating in the U.S.

Friday’s stress tests are one component of the Federal Reserve’s analysis during its annual Comprehensive Capital Analysis and Review (CCAR), which assesses the capital planning processes and capital adequacy of large bank holding companies and includes an evaluation of their planned capital distributions, such as dividend payments and share repurchases. CCAR results will be released on Thursday, June 27, at 4:30 p.m. EDT.

Meanwhile, US banks have been dramatically underperforming the market as rates and the yield curve have collapsed…

Probably nothing.

* * *

Full Report below: