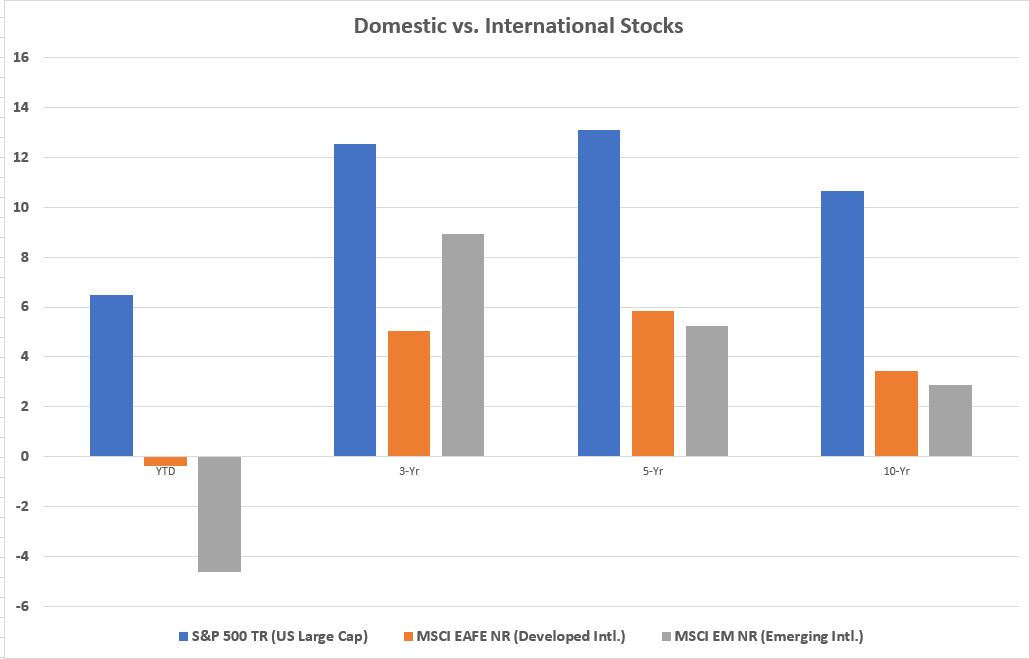

Domestic stocks outperformed international stocks for a long time. On a year-to-date basis, the S&P 500 Index was up more than 6% through July, while the MSCI EAFE Index was down slightly and the MSCI EM Index was down more than 4%. The international stock returns are after translation to the dollar, so they assume a U.S .investors bought them without using a currency hedge and received the dual return of the stocks in their local markets and the return of the local currency relative to the U.S. dollar.

In every instance (YTD, 3-, 5-, and 10-year periods), the international stocks performed better in their local markets before translation to the dollar. That means the dollar has been appreciating for a while. It has also been appreciating a lot recently.

There have been years over the past decade when international outperformed domestic. Last year was such a year. The S&P 500 produced a 21.83% return, while the MSCI EAFA delivered a 25.03% return and the MSCI EM Index delivered a whopping 37.28% return. But the recent long term has clearly favored U.S. stocks.

In the past emerging markets were said to be “coupled” with the developed world. If the developed world stopped spending, emerging markets suffered greatly. Also, there was coupling in the sense that emerging markets currencies would plunge when the dollar strengthened, and they’d have to spend all their reserves to prop up their currencies. Emerging markets countries borrowed debt in dollars or other developed world currencies, and dollar appreciation put an extra burden on them.

Has decoupling occurred now? Will the dollar’s rise crush emerging markets again, or have things changed? Are emerging markets able to stand alone now? Nobody knows. Clearly Turkey has been on a borrowing binge that it’s paying for now. But it’s not clear that’s the case with other developing countries.

It’s the dollar, stupid

Still, the FT’s John Authers writes of a “fragile five,” referring to five countries whose currencies are succumbing to a strong dollar — Turkey, India, Indonesia, Brazil, and South Africa. The currencies of these five countries also came under pressure during the “Taper Tantrum” of 2013 when Ben Bernanke talked of tapering his QE purchases.

Authers also notes that the price of gold tells us that the U.S. – or the U.S. dollar – is the cause of the current crisis. Gold has been depreciating; it has “behaved exactly like an emerging market currency, and has endured a true correction, dropping more than 10 per cent from the high it set early in the year.” All currencies depreciating relative to the dollar helps keep inflation in check, but it’s bad for the U.S. trade deficit. It doesn’t encourage American exports.

Authers wonders if the Fed will postpone future rate hikes the way it postponed reducing its bond purchases to temper the anticipation regarding the end of QE. This may indicate if emerging markets turbulence becomes calm.

On the other hand, perhaps Authers is putting too much faith in the Fed’s ability to assuage fears about rate hikes and the dollar. A recent MarketWatch article noted that emerging markets governments drain their dollar reserves in an effort to bolster their currencies. That means there are potentially “fewer dollars available for interest payments, pushing investors to demand richer yields as compensation for holding riskier debt.” The article reported that dollars custodied by the New York Fed for foreign central banks had decreased by $60 billion to $3.04 trillion in May, off from its peak f $3.11 trillion in March. Given that emerging markets countries borrow in dollars (and other developed market currencies), this could spell more trouble. Time will tell.