Authored by Lance Roberts via RealInvestmentAdvice.com,

Market Rallies To All-Time Highs

With the 4th of July weekend upon us, this week’s newsletter will be slightly shorter than usual. Such will ensure you “pitmasters” can get to work doing what you do best.

As we discussed last week, the market not only got off the mat and rallied back to new highs. That action continued through this week.

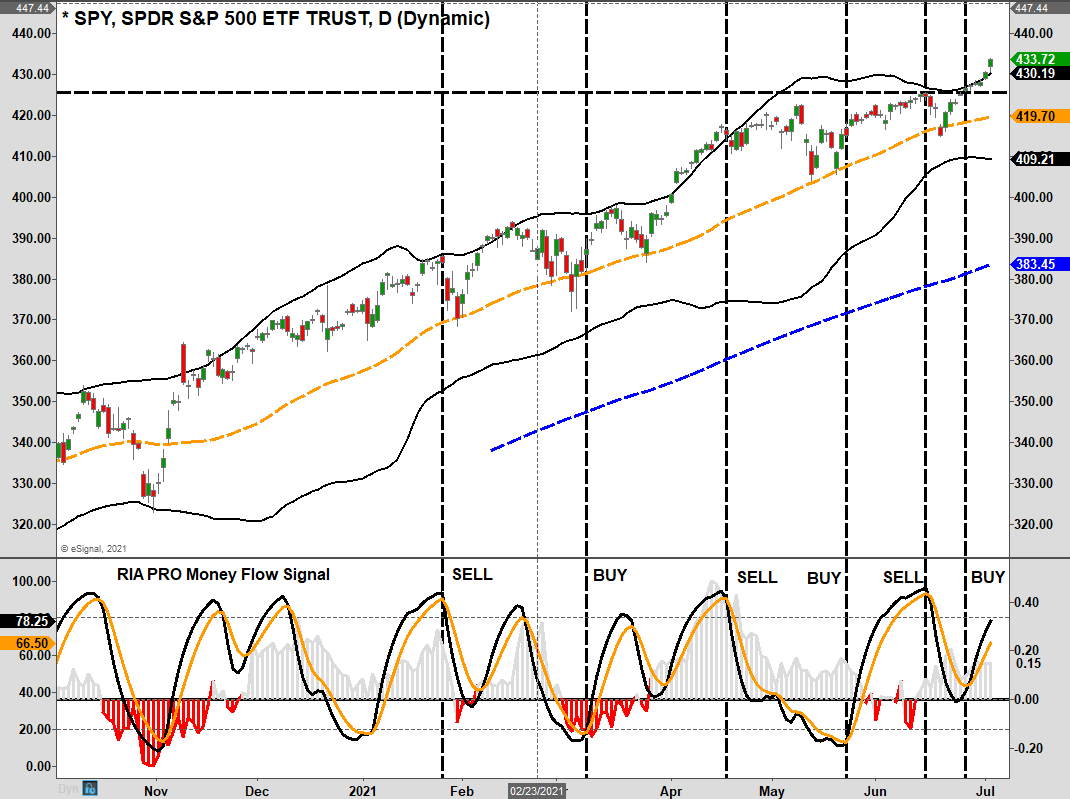

The technical backdrop is not great. With the market back to 2-standard deviations above the 50-dma, conviction weak, and investors extremely bullish, the market remains set up for additional weakness.

However, we are in the first two weeks of July which tends to be bullishly biased. After increasing our equity exposure previously, we will give the market the benefit of seasonality for now.

Complacency Concerns

With the “money flow buy signal” not yet back to a typical peak, such suggests another week or so of upside is likely. However, as noted, we suspect there is not much upside in the market for current levels.

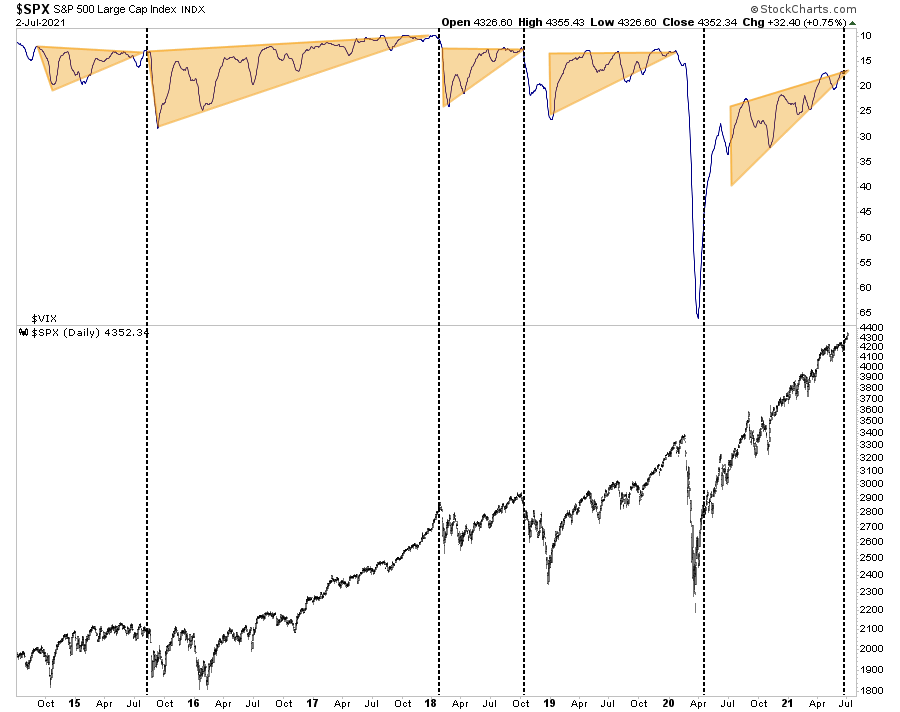

Lastly, we discussed the high level of complacency in the markets previously. To wit:

“Currently, complacency has reached more extreme levels. As noted last week, the 15-day moving average of VIX, on an inverted scale, suggests a correction is likely. By this measure, the correction should begin somewhere around July 21st – August 10th.”

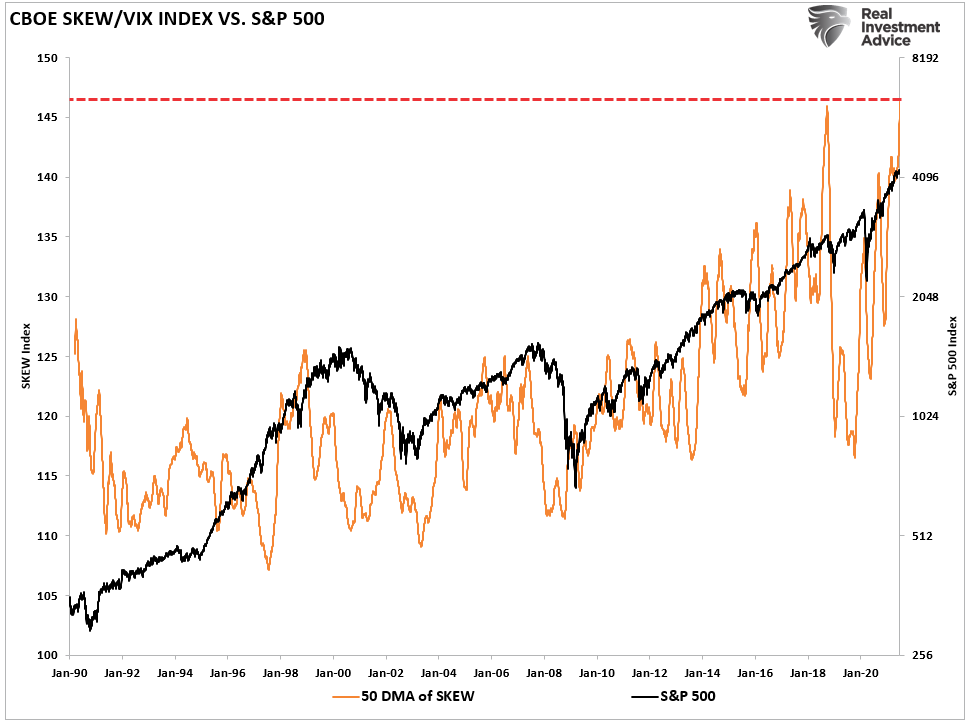

The same gets confirmed by the exceptionally high reading of the SKEW index.

“One such indicator is the CBOE SKEW index. The index measures the perceived tail risk of the distribution of S&P 500 investment returns over a 30-day horizon. It is similar to the VIX index, but instead of measuring implied volatility based on a normal distribution, it measures the implied risk of future returns realizing outlier behavior.

A SKEW value of 100 indicates the options market perceives a low risk of outlier returns. Conversely,values above 100 reflect an increased perception of risk for future outlier events.”

We are clearly above 100 currently.

The bulls are indeed in charge of the markets currently, but the clock is ticking.

As Good As It Gets

There is much at risk in the market as we head into the 3rd quarter and begin Q2-reporting for the S&P 500 index. For clarity, we need to review the “second-derivative” effect.

“In calculus, the second derivative, or the second-order derivative, of a function f is the derivative of the derivative of f.” – Wikipedia

In English, the “second derivative” measures how the rate of change of a quantity is itself changing.

I know, still confusing.

Here is a simplistic example.

Assume the economy is $1000 in value in Year 1. Then, in Year 2, there is a 50% recession. However, in Year 3, the economy grows back to $1000. And, in Year 4, the economy remains at $1000.

The “second derivative” effect is evident in years 3 and 4. In year 3, the economy recovers by $500, a 100% increase from Year 2’s level of $500. However, in Year 4, the growth rate falls to zero as the economy remains at $1000.

A Coming Change

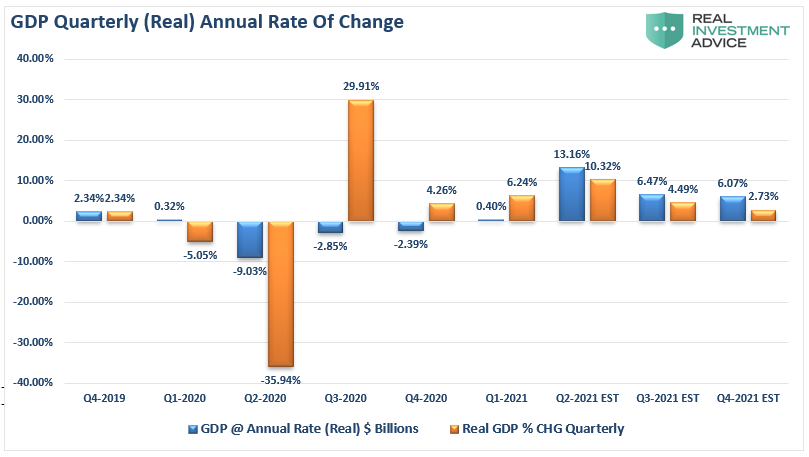

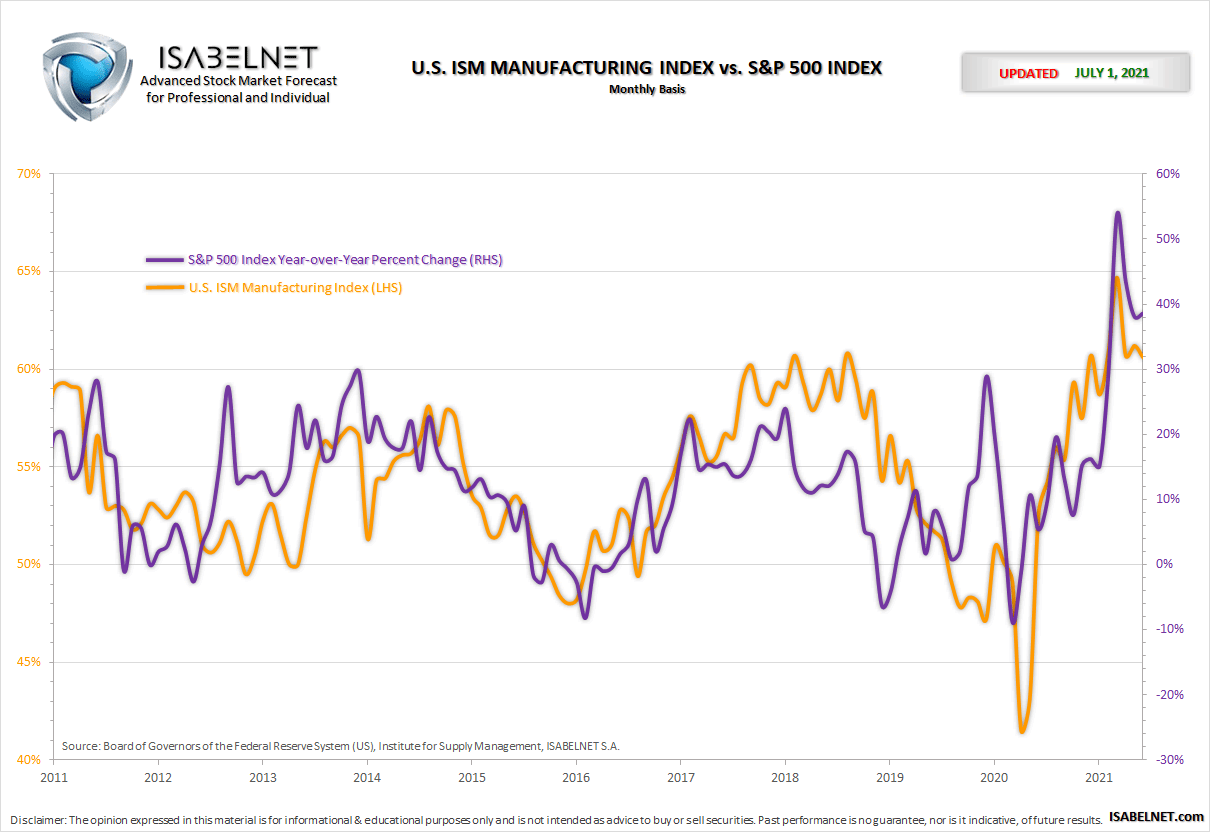

Why am I telling you this? Because we are at that point in the recovery cycle. Over the next couple of months, we will see the most significant numbers of the recovery cycle as we compare Q2-2021 to Q2-2020, which was the depth of the economic shutdown. As shown in the chart below, we will see a robust GDP report, but such will be the cycle’s peak.

The manufacturing activity indices have already peaked, which has a high correlation to the annual change in the S&P 500 index.

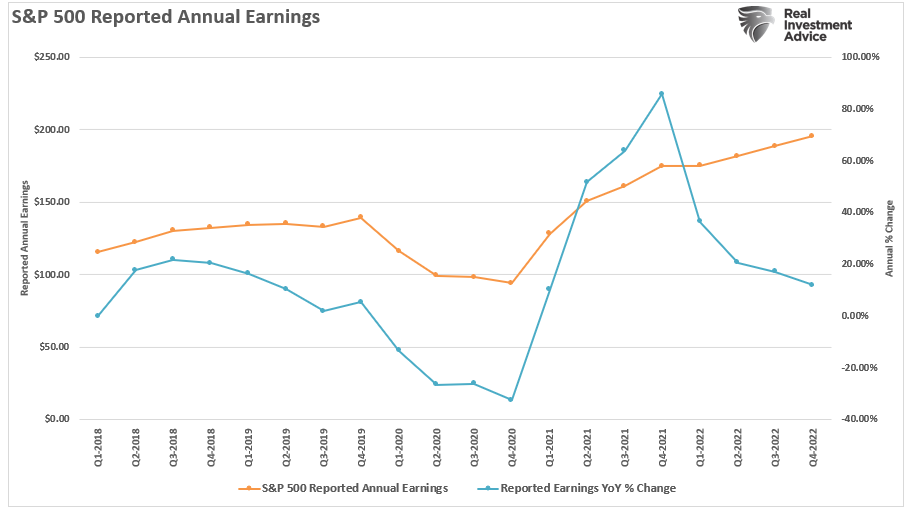

We will also see a peak in the annual rate of change in earnings as the economy slows. (Note: Current earnings estimates are exceptionally optimistic. By the end of 2021, the peak in earnings growth will likely move forward.)

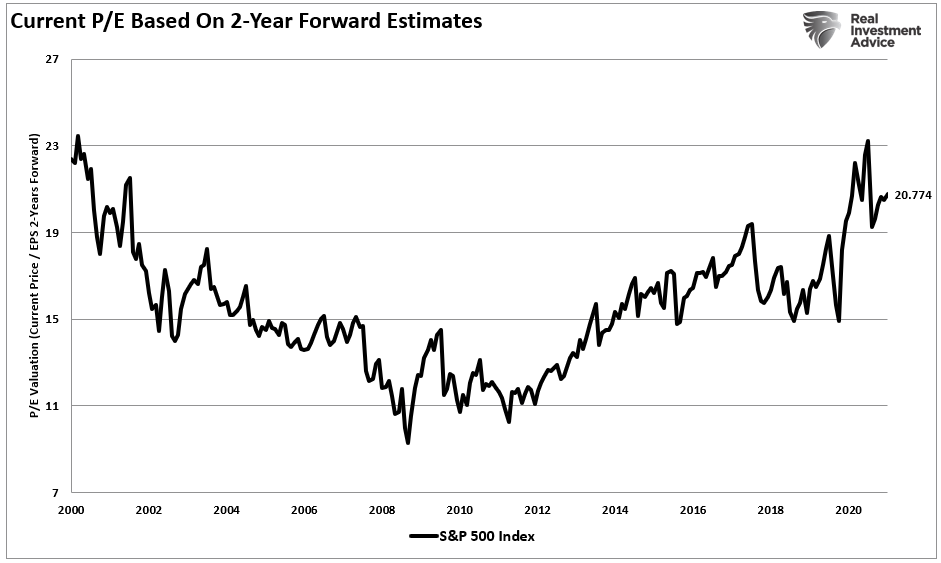

With valuations highly elevated on a two-year forward basis, when earnings are eventually revised lower with slower economic growth, valuations will rise. (You will often see media types compare forward P/E’s to current reported P/E’s, suggesting markets are cheap. However, that is not apples to apples as you are comparing forward to trailing P/E’s. As shown, two-year forward P/E’s are at the highest level since the “Dot.com” peak.)

The point here is that much of the growth in the economy is currently “priced in” to expectations. When things are as “good as they can get,” that is usually the point where things inevitably start to go wrong.

With no more stimulus coming from the Government and 9-million people coming off of unemployment benefits by September, a “fiscal cliff” is fast approaching. Such could well lead to a disappointment in expectations in a market currently priced for perfection.

Fully Invested Bears

The problem in discussing “investment risk” is that such commentary is summarily dismissed as being “bearish,” By extension, such means I am either sitting in cash or short the market. In either event, I have “missed out” on the last advance. However, now, the discussion of “risk” is even more futile due to the Fed’s massive interventions.

Such reminds me of something famed Morgan Stanley strategist Gerard Minack said once:

“The funny thing is there is a disconnect between what investors are saying and what they are doing. No one thinks all the problems the global financial crisis revealed have been healed. But, when you have an equity rally as you’ve seen for the past four or five years, everybody has had to participate.

What you’ve had are fully invested bears.”

The idea of “fully invested bears” defines the reality of the markets we live with today. Despite the understanding that the markets are overly bullish, extended, and valued, portfolio managers must stay invested or suffer potential “career risk” for underperformance.

The reason I bring this up is because of this comment from the legendary Leon Cooperman.

"I have a strong feeling the cycle we're going through won't end well but I have no idea where it ends," hear the full details of what Lee Cooperman told @BeckyQuick at yesterday's @cnbcevents #FASummit at https://t.co/Rc4p9phRer. pic.twitter.com/NnjIezNOvN

— Squawk Box (@SquawkCNBC) June 30, 2021

The clip is fascinating because Becky Quick refers to Leon as a “fully-invested bear” as he states:

“You have to be in the market right now.”

The Two Big Risks

There are two inter-related risks to the market currently. The Fed and “inflation.”

As Leon correctly notes, companies should be able to pass on inflated materials costs to their consumers:

“Everybody is worried about inflation. Inflation is a positive for common stocks because inflation in companies’ costs works its way into selling prices, which lift the nominal level of revenues and earnings.”

In theory, that is true, but as noted above, with the “fiscal cliff” approaching, there is a risk that consumers can’t absorb as much “inflation” as he hopes. Moreover, as I showed previously, the gap between CPI and PPI already indicates that companies are retaining inflation.

The other problem is the Fed. The markets will not react kindly to the Fed moving to curb inflationary pressures.

In either case, the risk to markets remains elevated. While I certainly agree you “have to be invested in the markets currently,” we are also fully aware of the risks.

Yes, that makes us “fully invested bears.”