By Wolf Richter for WOLF STREET.

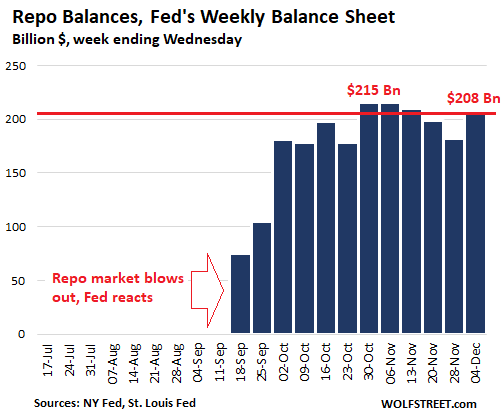

The total amount of repurchase agreements (“repos”) on the Fed’s balance sheet as of December 4, released today, declined over the past month to $209 billion, from $215 billion a month ago. These repos included:

- $70 billion in overnight repos, issued on Wednesday morning that unwound today; all prior overnight repos had already unwound.

- $88 billion in multi-day repos with maturities of up to two weeks;

- $50 billion in 42-day repos; of which $25 billion were issued on November 25 and $25 billion on December 2. They will unwind early next year.

Before the repo market blew out in mid-September, the repos on the Fed’s balance sheet were zero. This chart shows the weekly balances of repos on the Fed’s balance sheet as of each Wednesday:

In these “repo operations,” the Fed buys Treasury securities, mortgage-backed securities issued by Fannie Mae and Freddie Mac, and government “Agency” securities, under an agreement whereby the counter parties have to repurchase those securities on a set date at a set (higher) price. The interest rate is determined by the difference between the price the Fed buys the securities at, and the pre-set higher price it sells the securities back to the original counter party.

Via these operations, the Fed effectively lends to the repo market at rates that are within its target range for the federal funds rate. Today’s overnight repo operations had a rate of 1.55%. This is a way to push all repo rates down into the Fed’s range. And it guarantees that companies that borrow in the repo market, including mortgage REITs and others, can borrow at these ultra-low rates.

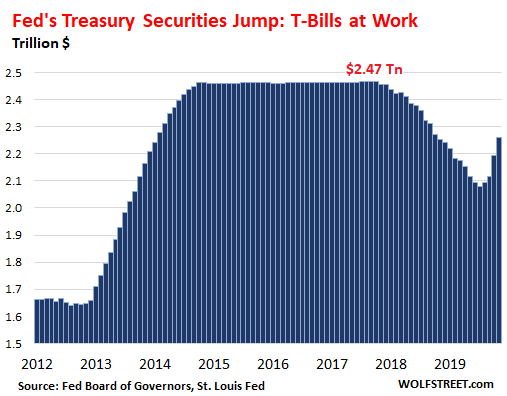

Fed goes hog-wild with T-Bills.

During the month of November through the balance sheet as of December 4, the total amount of Treasury securities jumped by $65 billion, mostly short-term Treasury bills (T-Bills) with maturities of one year or less. This raised the balance of Treasury securities to $2.26 billion.

There had been no T-bills on the Fed’s balance sheet for the last few years. But earlier this year, the Fed changed strategy and switched to replacing some of its maturing longer-dated securities with T-bills. Then following the repo market blow-out, it decided to douse its Wall Street cronies with cheap cash. Under this program, it said it would add $60 billion a month in T-bills. Since July, it has piled on $179 billion in Treasury securities, including $77 billion in October and $65 billion in November, the biggest monthly increases since the depth of the Financial Crisis.

Only this time, there was no crisis. All that happened was that the repo market had had a hissy-fit and that rates spiked. And instead of letting the market take care of it, and let some risk-takers eat dust for taking these risks, the Fed is bailing them out. When it comes to bailing out its crybaby cronies on Wall Street, even when there isn’t a crisis, the Fed stops before nothing:

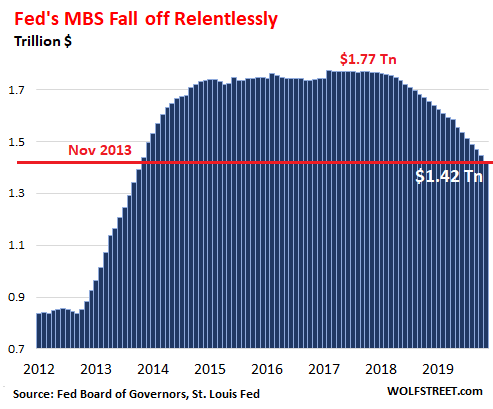

Fed continues to shed Mortgage-Backed Securities

The Fed has stated many times that it wants to get rid of its holdings of MBS. And it’s progressing with the plan. In November, the Fed shed $22 billion in MBS, exceeding the self-imposed cap of $20 billion per month for the seventh month in a row. Over the past seven months, it has shed $160 billion in MBS, or about $22.8 billion a month on average. Its holdings are now down to $1.42 trillion, below where they had first been in November 2013:

Holders of MBS, including the Fed, receive pass-through principal payments as the underlying mortgages are paid down or are paid off. About 95% of the MBS on the Fed’s balance sheet mature in 10 years or more, and the current runoff is almost entirely due to these pass-through principal payments.

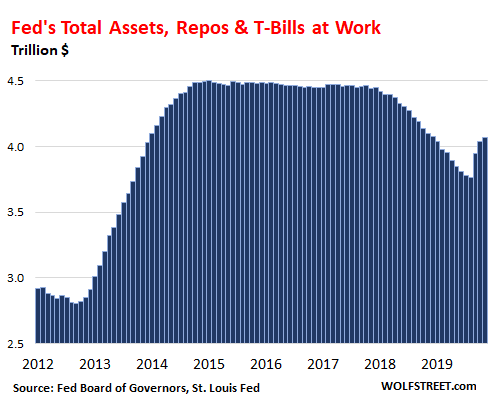

Total assets on the Fed’s balance sheet

The net effect of the surge in Treasury securities, the drop in MBS, and the small decline in repo balances along with some other factors, is that total assets rose by $26 billion from the prior month, to $4.07 trillion, having jumped by $304 billion in three months, the fastest since the post-Lehman months in early 2009:

Even though the Fed is dousing its crybaby cronies with cash and is bailing them out in the repo market, it is not targeting long-term interest rates, which it had done during QE. Instead, it is unloading MBS with long maturities and is piling on short-term T-bills, which has allowed long-term rates to tick higher from the lows last summer before this freak show began.