When it comes to the topic of banking risk, well…one can only lean back in a chair, sigh and say: “Where to begin?”

A Rich and Deep History of the Absurd

Banks, and hence banking risk, come in a wide variety of flavors, largely because bank mismanagement and short-sighted absurdity comes with equal frequency. As such, a fuller discussion on banking risk would necessitate hundreds of pages and hundreds of examples.

From the woefully arrogant and even more woefully mismanaged central banks, to the equally arrogant and mismanaged commercial banks, the long history of almost unbelievable hubris, risk, and over-bonused (and over-touted) bank leadership is almost endless.

Perhaps this is what prompted Henry Ford to observe that if ordinary citizens actually knew how banks operated (i.e. from fractional reserve banking to arms-length derivative deals with over-levered hedge funds), there would be immediate revolution in the streets.

Although such observations may seem like an exaggeration bordering upon the sensational, one only needs to look beneath the surface of things to realize that reality (and banking risk) is indeed stranger than fiction.

In prior reports, we’ve written about banking risks that date banks centuries, even millennia.

In short, it’s never difficult to put a finger on the map of history, locate any major moment of financial crisis and then find a banker (be he in a toga, French silk ruffles or an Armani suit) sulking in a corner somewhere, head down and hoping not to be recognized or caught.

This is simply because global history, as well as the history of bankers and major financial disasters, from the money lenders of the Old Testament to the S&L Crisis of the 1980’s or the Lehman Moments of 2008, are, sadly, all too common, all too familiar, and all too inevitable.

Again, volumes can be, and have been, written on such a sordid, but all-too-confirmed, trail of absurd banking practices leading to horrific consequences for nations, financial systems and of course, individual investors.

Modern Banking Risk: No Less Absurd

Today’s level of banking absurdity, and hence banking risk, of course is no exception.

The amount of non-performing loans (NPL’s) sure to stream out of the post-COVID (and self-inflicted) gunshot wound to small businesses and commercial real estate owners and tenants are just one among many risks facing the current banking system, which, as we’ve written elsewhere, is quietly (and not surprisingly) coming under greater and greater governmental command control.

In fact, the level of banking risk which lies beneath the so-called bank “recovery” from the Great Financial Crisis of 2008 is higher than most pundits, sell-siders and media pablum-sellers would otherwise have the vast majority of investors believe.

After all, good news, even artificial news and artificial bubbles, sell stocks and make investors (and bankers) happy.

The spin behind healthy banking news is no different, which is to say, no less mis-reported and bullishly comforting.

As all bankers wishing to remain employed know, the financial world spins on calming stories, tweaked data and comforting delusion. Today, such market delusion (in everything from Tesla stocks to negative yielding bonds), as well as banking risk, has never been higher.

As markets distorted by desperate central bank policies reach record highs on balance- sheet challenged, debt-soaked securities, the mad crowds continue to chase return, completely blind to risks hiding in plain sight.

In fact, and due to modern uses of leverage and equally modern weapons of mass destruction in the form of financial derivatives colliding with a central-bank-created debt tsunami the likes of which the world has never seen, banking risk has never, not ever been this high.

And yet the vast majority of TikTok savvy and Tweet-educated investors have zero idea of the risks lurking beneath the current market wave.

Market sentiment, despite a global pandemic and historically unprecedented debt crisis, has never been higher.

As I like to say: The ironies do abound.

But rather than pen hundreds of pages of this banking history here, let’s just consider one screaming, flashing, neon-red symbol of banking risk that is hiding in plain sight this very second.

That is, let’s toe-dip into that clever, banker-invented timebomb otherwise known as the global derivatives market.

The OTC Derivatives Trade: The Real Killer Virus

One does not need to pass a FINRA exam or spend years working the prop desks at a major commercial bank to understand the broad strokes of the otherwise extremely (and intentionally) complex, opaque and non-reported world of derivative instruments circulating like an Ebola virus through the modern banking system.

The fancy lads call this the OTC market—or “Over the Counter” derivatives trade.

“Over the Counter,” by the way, is just a euphemistic way of saying a highly, highly illiquid trade, one not executed on an exchange, but conducted instead among over-paid bankers and other institutional counter parties on a daily basis.

You know, the so-called “experts” …

The gross value of this OTC derivatives market is nearly impossible to define, as the various contracts, swaps and options that compose this tangled web of obfuscation and arbitraged markets are in fact valued (marked) by the banks and counterparties themselves, not the open market.

That’s clever, no?

But hey, if you’re going to be guarding (i.e. valuing) your own hen house, it helps to be a clever fox, and bankers are certainly foxy.

Keeping Derivatives Simple

Conservatively, however, it’s fair to say that the current OTC derivatives market is in the neighborhood of $1.5 quadrillion in size, a number I’m not even sure how to type on this page.

Yet despite such an almost fantastical valuation and size, none of these zeroes are reported on the balance sheets of the fancy banks who trade them. Like I said, bankers are clever little foxes.

So, how do these little foxes get away with this? How do they hide the risk and size of these trades from their own books?

This too, involves a bit of complicated banker (and book-keeping) lingo which would make both your eyes (and mine) glaze over if entirely unpacked here.

But as Einstein liked to say, if you can’t explain even the most complex concepts to a five-year-old, you aren’t a very good teacher.

Simple Arbitrage, Simple Leverage, Simply Crazy

First, we need to address that lovely little banking term known as “arbitrage,” which basically boils down to buying and selling the same asset simultaneously and pocketing the difference—hopefully, a profit.

Recently, for example, I purchased a horse saddle on line, and then decided to sell it to another buyer hours later for more than I originally contracted. Voila: arbitrage.

In that brief period, however, between when I bought the saddle for $X and then contracted to sell it for $X + $100, I was in what the fancy lads at places like Deutsche Bank or Goldman Sachs call an “open position”—or stated more simply: I was between trapezes.

That is, if I didn’t get the saddle delivered when I needed it, I’d fail on its subsequent delivery to the next buyer, who would be angry to say the least.

Such failure to perform is what those same fancy lad bankers call “counter-party risk.”

Fortunately, I delivered the saddle as contracted and the counter-party risk was minimal. Easy peasy.

It’s the same for banks buying and selling futures contracts, swaps, call options, put options and all those other shrewd derivative instruments they arbitrage to the tune of billions every second…but with one minor exception: Unlike my simple horse saddle purchase, those fancy lad bankers use 100:1 to 300:1 leverage to buy and sell their sexy little contracts.

A Side-Market Premised on Only Good Times

In normal market conditions, counterparties to these grossly levered derivatives perform as expected. All goes well, and trillions pass between computer screens on arbitrage desks from London to New York, Frankfurt to Tokyo.

But derivative trades are a lot like water skiers being dragged behind a speeding boat: If the boat rides straight and steady, and the water has no ripples, the skiers (i.e. counterparties) glide blissfully, rapidly and safely across a sea of easy money.

But this, of course, is where the entire concept as well as reality of the derivatives trade gets scary, and frankly, just plain absurd, for its entire survival and risk-less future assumes that speed boats never turn sharply, seas never get rough and accidents never happen.

In short, the derivatives trade depends on a best-case scenario of perpetually smooth riding and smooth seas to avoid fatal risk among counterparties.

But as anyone, and I mean anyone, who has traded or studied markets for more than a half hour knows, nothing about financial markets is a perpetually smooth ride free of frequent ripples or an occasional tidal wave.

Despite such obvious common sense, the entire derivatives market (and its buying and selling of premiums, counterparty-spreads etc.) is premised on the self-delusional fantasy that seas are always smooth and water skiers never fall.

A Ticking Timebomb

Thus, despite massive amounts of leverage, massively low “OTC” liquidity (every market crisis, by the way, is at heart a liquidity crisis), massive counterparty risk, and massively obvious macro risks (as evidenced in everything from broken central bank policies, supply chain disruptions, and geopolitical risks to zombie credit markets marching daily toward default), the un-noticed and un-reported ($1.5 quadrillion+) derivative trade just keeps ticking away at a major commercial bank near you—ticking, that is, like a financial timebomb.

Timebomb?

Yes. Time. Bomb.

But if this seems sensational, once again, let’s just do the math and resort to numbers not adjectives.

Take the example of Deutsche Bank, that oh-so notorious bad boy of the otherwise media-ignored derivatives sand lot.

Like all major commercial banks trading in home-made derivative instruments, Deutsche Bank values its exposure not based upon the leverage used or the true dollar amounts at risk, but rather based upon derivative contracts whose value, as well as risk, is not “marked” (i.e. placed on the balance sheet) until the contracts themselves are exercised.

The book keepers at banks like Deutsche Bank call this the “net” value of their derivative trade.

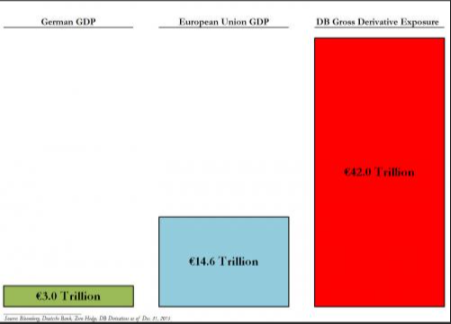

In the case of Deutsche Bank, whose overall balance sheet asset valuation last year was around $800B, the ledger regarding its “net” derivative exposure was a measly $1B. In short, not the least bit scary at all for a mega bank’s balance sheet or risk profile.

But here’s the rub: The “net” value of derivative exposure reported on the books by banks like Deutsche Bank deliberately and completely ignores the truer derivative exposure and valuation known among the fancy lads as the “gross” derivative value, which more accurately accounts for the actual amount of leverage, premium spreads and counterparty obligations behind their trades.

Again, this more accurate “gross” valuation (and risk exposure) is not marked on the balance sheets of these water-skiing banks…

Turning back to the Deutsche Bank example, we discover that this bank, with a total balance sheet asset value of $800B, marks its “net” derivative value down as $1B, yet neglects to report its “gross” derivative exposure of $40T.

Please: Read that last line again. It’s not a typo.

That right; the “gross” (yet legally unreported) derivative exposure at Deutsche Bank is $40T, despite an enterprise asset value of just $800B for the entire bank itself. In fact, Deutsche Bank’s derivatives exposure is greater than 3X total GDP for the entire European Union.

That’s Banking Risk

So, do you still think there’s no banking risk out there?

The horrific, yet entirely ignored reality is that the current banking system is literally nothing more than a balance-sheet mosquito roosting on a nuclear bomb of levered derivatives exposure set to explode the moment any number of potential and “nuclear” red buttons go off in an otherwise completely distorted global market.

In fact, the list of potential “red-button” moments pointed at this derivative mega-bomb is so long, that the odds of a derivatives implosion, and hence banking implosion, is not just high, it’s closer to 100%.

For the sake of brevity, just consider the following potential red-button triggers:

-Counter-party risk (mere hints of which we’ve seen at Long Term Capital Management, Lehman Brothers, AIG or Bear Sterns in the past, or more recently in headline-making leverage factories like Archegos Capital, whose recent derivative swap trade (co-authored by commercial banks) lost over $10B in shareholder money almost overnight.

-Supply Chain interruptions (as already hinted by oil futures trading negative, or actual gold deliveries failing in the COMEX market);

-Central Banks imploding under the weight of their own balance sheets and losing control of interest rates, which turn zombie bond pits into cemeteries;

-Any black swan, happening at any time.

In short, if there is any counter-party error (ripple or tidal wave) of any genuine and collective magnitude in this over-levered minefield known as the global derivatives market, the silly little net derivatives exposures on the seemingly yet deceptively “safe” balance sheets of the major commercial banks could morph into a gross exposure, and hence a gross loss, of greater than 5X the total valuation of the banks themselves.

After all, the Deutsche Bank is hardly the only bank playing this dangerous game of derivative-roulette. One can easily add JP Morgan, Goldman, Wells Fargo, Soc Gen, BNP or Morgan Stanley to the list.

Needless to say, the cost of bailing out these Too Big to Fail (TBTF) banks in such a derivative implosion would dwarf the TBTF bailouts of 2008, and force central banks to create even more currency destroying dollars out of thin air to save the banking sinners while leading to even more centralized, government control of our banking system.

When, not if, a crisis occurs in this toxic commercial banking system sitting above a home-made derivatives time bomb, do you want to hold your gold, or any precious metal asset, in such esteemed, globally recognized and balance-sheet savvy commercial banks?

Decades ago, we created Matterhorn Asset Management so you wouldn’t have to.