by UPFINA

The retail investor group needs to be distinguished. There are always retail investors in the market. Many of them who have been investing for years have done well. The makeup of retail investors changes during manias as those looking to make fast money far outnumbers those in it for the long haul. Branding all retail investors as ‘dumb money’, as many tend to do, is harsh. We aren’t saying the outperformance this year makes retail great. That won’t continue because they are going with risky strategies and investing in hot companies they don’t understand.

Broadly speaking, new speculators don’t have a firm grasp on genomics unless they come from the medical field. In Robinhood’s year in review, they mentioned over 3.2 million people read their educational articles as daily visits were up 260%. Over 2 million people invested with fractional shares.

Engaging with new content to learn about investing is great. Broadening the number of people who invest in stocks is also great. However, we all know the motivation behind this movement is quick profits and the fact that people were forced to stay home. If many story stocks didn’t have triple digit gains, retail wouldn’t be interested. Retail is also causing these large gains by piling into the hottest names. By definition the popular stocks have the most investor capital. That isn’t a sustainable investing strategy. Beating the market by triple doesn’t matter if you lose money the next year. It’s simply impossible for the vast majority of new investors to do well if they have the wrong mindset.

ARK Innovation Fund Goes Parabolic

The point in discussing ARK Invest is to gage the euphoria in retail buying rather than to say they are good or bad investors. When everyone piles into any security, it becomes a measurement of sentiment. That’s why bitcoin is also a measurement of sentiment as it hits record highs in late 2020. Speculators are feeling greedy. They are willing to place big bets on margin on pretty much anything that has gone up a lot.

Recently hit 69% above its 200 DMA. For perspective, some prior assets at their peak:

Silver in '11 = 75%

NDX in '00 = 60%

Crude in '08 = 45%

NKY in '87-'89 = 30% pic.twitter.com/BzIbZ9IskL— Jonathan Krinsky,CMT (@jkrinskypga) December 28, 2020

The ARK Innovation fund is symbolic of the magnitude of the speculation by retail investors which has never been matched in human history because the access to trading accounts has been democratized and the government is giving out stimulus checks. The latest check is for $600, but it could be raised to $2,000. As you can see from the chart above, the ARK Innovation fund is 63% above its 200 day moving average. It was just 69% above its 200 day moving average which means it has increased quickly. For context, the Nasdaq peaked at only 60% above its 200 day moving average at the peak of the tech bubble in 2000. On a related note, the Russell 2000 is on an 8 week winning streak which is its longest since February 2019.

The IPO Mania Of 2020

2020 has provided speculators with dual gambling opportunities through SPACs and IPOs. The fact that SPACs have garnered so much capital and attention while IPOs also had a record year is impressive. As you can see from the chart below, IPOS did $178 billion in volume in 2020 which is the record high by far. We are experiencing the hottest market for new growth companies since 2000. Companies with only a glimmer of a potential business are doing SPACs which is just like the IPOs of the late 1990s.

🇺🇸 #IPO | Almost 500 companies listed in the U.S. in 2020, raised a combined $178.2 billion, a record amount, according to data compiled by Bloomberg. pic.twitter.com/APNleMVXqd

— Christophe Barraud🛢🐳 (@C_Barraud) December 28, 2020

Earnings Are Actually Good

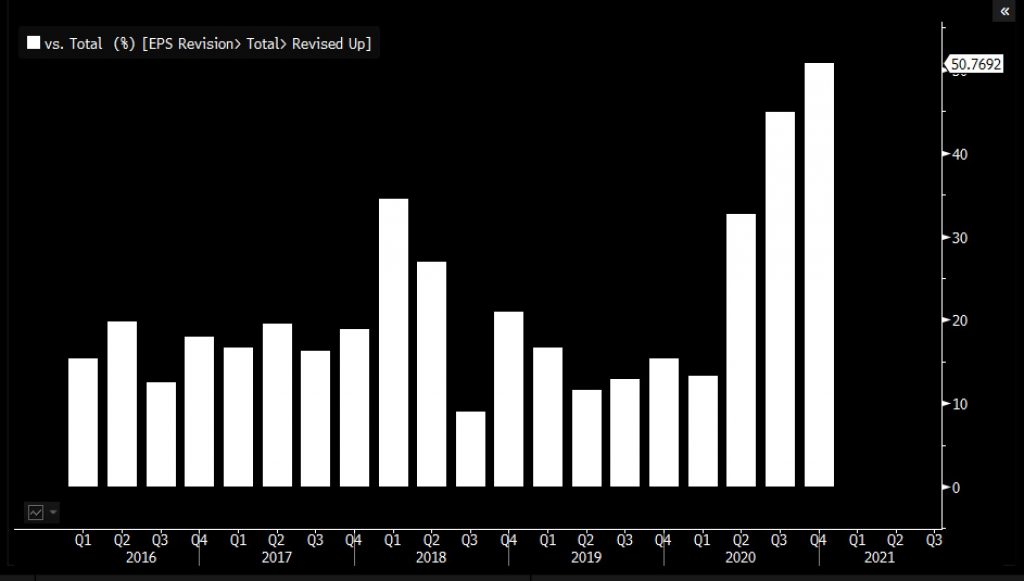

There is some backing to this rally especially from the legitimate companies that actually make money and aren’t based off an idea which generates no sales. As you can see form the chart below, 50.8% of the S&P 500 firms which issued Q4 guidance increased it which is the most in at least a decade. That’s very impressive because the economy slowed at the end of Q4 as deaths were the worst of the pandemic in December.

2021 EPS estimates have increased for 10 straight weeks. They usually fall at this time of year. 2021 EPS estimates rose from $159 to $167. The problem is the market still trades at 22 times earnings. Tesla’s insanely high multiple just makes the market look even more expensive. Apple hit a record high on Monday giving it a 34.5 PE multiple based on 2021 estimates. That’s very high for a firm that is set to grow EPS in the high single digits. You would think it would trade closer to 20 times estimates.

Growth Dominates Value

In this market, either your stock is deemed a winner or it is a loser. Winners with high growth get multiples above 30 or even 40 in many cases. The losers get multiples in the high single digits as investors expect their businesses to die within a few years. As you can see from the chart below, low economic growth and technology enabling disruption have allowed growth firms to dominate value firms in sales, earnings, and free cash flow growth in the past 13 years. Let’s keep in mind that this macro setting makes some innovations look better than they are because short term stock gains cloud people’s judgment.

The Market Is Filled To The Brim

As you can see from the chart below, the initial part of the tech bust in 2000 had the rest of the market rallying slightly while tech crashed. Then eventually, the whole market fell, with growth stocks falling the most. This time could be the same. Imagine a scenario where growth stocks peak early next year, but cyclical stocks rally because of the reopening and the stimulus. We could see the whole market fall after the stimulus runs out and cyclical stocks get expensive.

Year 2000 pic.twitter.com/VkuaZCT1uf

— Plan Maestro (@PlanMaestro) January 20, 2018

Conclusion

Retail isn’t made up of all speculators who are ‘dumb money.’ However, in manias like we have now, dumb money in retail outweighs the experienced investors. There are millions of them and they have a decent amount of capital because they have made so much this year. This has been an amazing year for ARK Invest, IPOs, and SPACs. Earnings estimates have risen, but the market still sports a high PE ratio. Growth firms have beaten value firms in key metrics in the past 13 years. We could see growth stocks underperform for a few months before the whole market falls like in the early 2000s bear run.