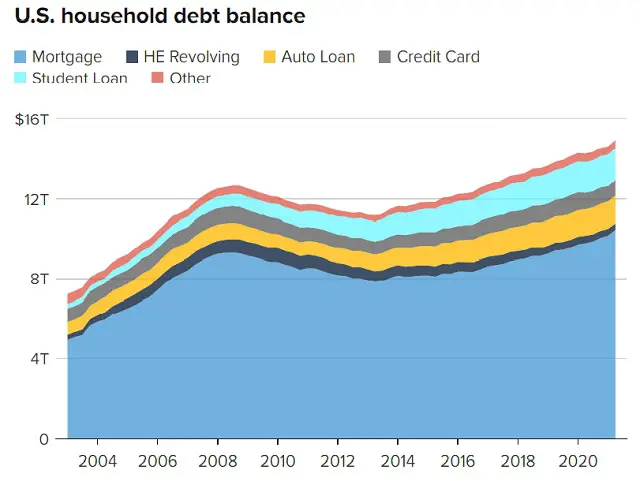

This week, US household debt jumped by the most in 14 years to a new all-time record. The last time it did something like this was in 2007, just as the housing mania was cresting and the Great Recession was looming.

The biggest part of the recent gain was from mortgages (it’s official, we’re in housing bubble 2.0). But credit cards and auto loans are rocking too.

So you’d think that we’d have all the basic ways for the unsophisticated to borrow money pretty much covered. But no, it turns out that the world is so in need of new credit sources that it’s resurrecting the layaway plan, which pre-financialization Americans used to buy things they couldn’t immediately afford. Amazingly, this old-as-the-hills “buy now pay later” concept is being hailed as an innovation, and the companies “pioneering” it are attracting Silicon Valley-level capital. Consider:

Square to buy Australia’s Afterpay in $29 billion deal as ‘buy now, pay later’ trend takes off

Square plans to buy Australian fintech company Afterpay as it looks to expand further into the booming installment loan market.

Jack Dorsey’s payments company announced the $29 billion, all-stock deal on Sunday evening. The price tag marks a roughly 30% premium to Afterpay’s last closing price.

“Square and Afterpay have a shared purpose,” said Square’s CEO Dorsey in a statement. “We built our business to make the financial system more fair, accessible, and inclusive, and Afterpay has built a trusted brand aligned with those principles.”

Shares of Afterpay in Australia soared more than 23% Monday morning on the back of the news.

Square pointed to consumers eschewing traditional credit, especially younger buyers. The San Francisco-based payments company already offers installment loans, which said it has been a “powerful growth tool” for Square’s core seller business. It plans to integrate Afterpay into both its seller and Cash App ecosystems.

Afterpay lets customers pay in four interest-free installments and pay a fee if they miss an automated payment. Its 16 million customers will eventually be able to manage installment payments directly through Cash App. The deal is expected to close in the first quarter of 2022.

So-called installment loans have been around for decades, and were historically used for big-ticket purchases such as furniture. Online payment players and fintechs have been competing to launch their own version of “pay later” products for online items in the low hundreds of dollars.

Affirm is one of the better-known public companies offering the option to finance items in smaller, monthly payments. PayPal, Klarna, Mastercard and Fiserv, American Express, Citi and J.P. Morgan Chase are all offering similar loan products. Apple is planning to launch installment lending in a partnership with Goldman Sachs, Bloomberg reported last month.

Hmmm… Wonder how these financial innovators make their money. Could it be from those fees charged when customers miss an automated payment? Sort of like how the credit card companies make most of their profits from late fees.

And who accounts for most late fees? Why, the young, the poor, and the unsophisticated, of course. The serfs, in other words, who are desperate for the things they see on TV and easily conned into taking on loans they can’t afford, then milked ever after by their friends at Visa and Mastercard – and now, apparently, their new friends at Square, PayPal, and Apple.

The only consolation here is the prospect of a wave of buy-now-pay-later defaults crushing the consumer finance industry.