Last week, venture capitalist Chamath Palihapitiya said that central banks have virtually eliminated recessionsthrough their aggressive monetary stimulus programs such as quantitative easing (QE) and record low interest rates –

“I don’t see a world in which we have any form of meaningful contraction nor any form of meaningful expansion. We have completely taken away the toolkit of how normal economies should work when we started with QE. I mean, the odds that there’s a recession anymore in any Western country of the world is almost next to impossible now, save a complete financial externality that we can’t forecast.”

Former Fed Chair Janet Yellen made a similar statement in 2017 –

“Would I say there will never, ever be another financial crisis? You know probably that would be going too far but I do think we’re much safer and I hope that it will not be in our lifetimes and I don’t believe it will be.”

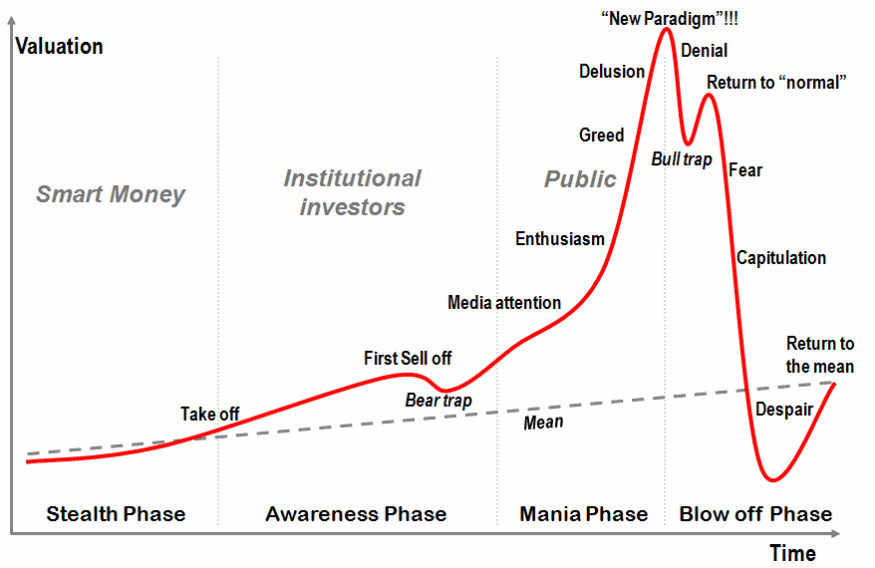

Unfortunately, statements like those above are most commonly made during a bubble or the latter stages of economic cycles. Those kinds of statements are indicative of investor complacency and overconfidence, and should raise contrarian eyebrows. Palihapitiya’s statement sounds very similar to economist Irving Fisher’s infamous 1929 assertion that stocks had reached “what looks like a permanently high plateau” (the stock market crashed just 13 days later).

As the bubble stages chart below shows, market participants become delusional and believe in the myth that the market or economy is experiencing a “new paradigm” in which the old rules no longer apply. Chamath Palihapitiya’s idea that central banks have virtually eliminated recessions is a prime example of this “we are in a new paradigm” thinking. Palihapitiya’s assertion is not new: during the late-1990s dot-com bubble, many economists and technologists believed that the U.S. had a “New Economy” in which technological innovations would keep inflation very low and that recessions had been virtually eliminated. Of course, the “New Economy” believers experienced a rude awakening when the dot-com bubble burst in the early-2000s, the Nasdaq sank 80%, and the U.S. economy experienced recessions in both 2001 and 2007 to 2009.

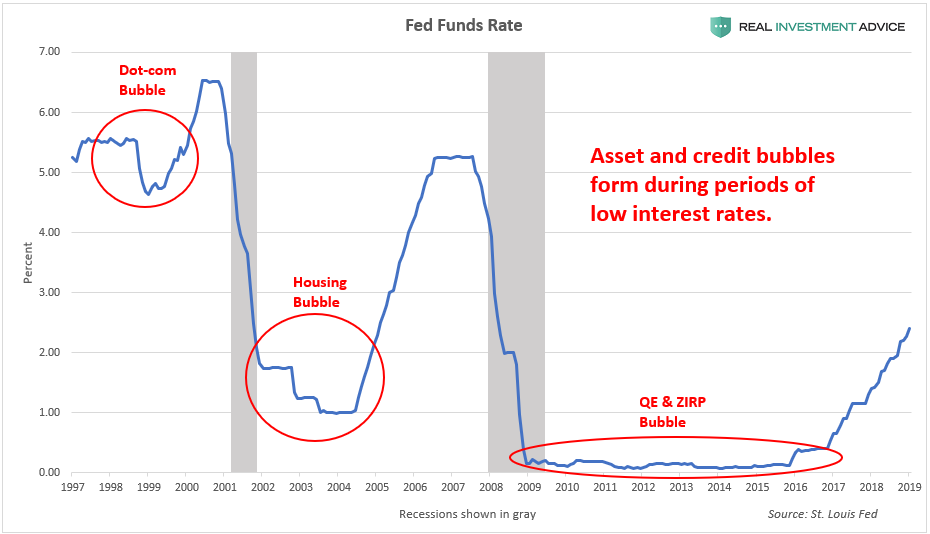

What Chamath Palihapitiya doesn’t realize is that the Fed and other central banks have created economic growth and a so-called economic “recovery” by inflating dangerous new economic bubbles around the world (see my explanation about this). The Fed has not eliminated recessions; the growth-driving bubbles that it has created simply haven’t burst yet. As the chart of the Fed Funds rate below shows, asset and credit bubbles often form when central banks cut interest rates to low levels. The dot-com and U.S. housing bubbles formed during relatively low interest rate periods and the current cycle will prove to be no different, unfortunately.

One of the dangerous, economic growth-driving bubbles that have been forming as a result of the Fed’s loose monetary policy is the tech startup bubble. Over the past several years, tens of thousands of tech startups have been formed as entrepreneurs try to start the next Google or Facebook. The explosion of venture capital activity over the past several years can be seen in the chart of the monthly count of global VC deals that raised $100 million or more.

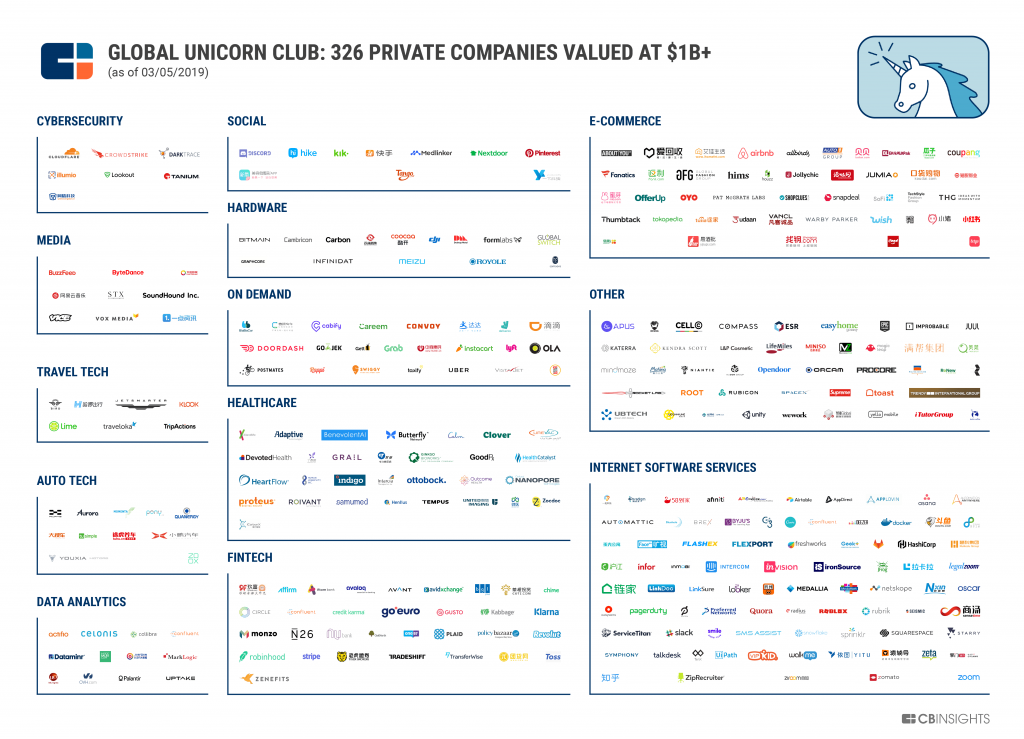

Over the past several years, hundreds of new tech “unicorn” companies that have valuations of $1 billion or more have come out of practically nowhere and most don’t even turn a profit. Make no mistake: the tech unicorn phenomenon is a direct byproduct of stimulative central bank policies. Today’s tech unicorns are the equivalent of dot-coms in the late-1990s and will experience the exact same fate. Though many people in the startup world believe that the boom is the result of new technologies, the reality is that the startup boom is likely only 20% due to new technologies and 80% due to the trillions of dollars worth of liquidity that central banks have pumped into the global economy over the past decade. As a prominent tech VC, Chamath Palihapitiya is so deep into the tech startup culture that he’s missing the forest for the trees and doesn’t see the obvious bubble (and, therefore, the risk of another economic crisis when this bubble and many others like it eventually burst).

A very high percentage of today’s startups are actually malinvestments that only exist due to the false signal created when the Fed and other central banks distorted the financial markets and economy with their aggressive monetary stimulus programs after the global financial crisis. See this definition of malinvestment from the Mises Wiki:

Malinvestment is a mistaken investment in wrong lines of production, which inevitably lead to wasted capital and economic losses, subsequently requiring the reallocation of resources to more productive uses. “Wrong” in this sense means incorrect or mistaken from the point of view of the real long-term needs and demands of the economy, if those needs and demands were expressed with the correct price signals in the free market. Random, isolated entrepreneurial miscalculations and mistaken investments occur in any market (resulting in standard bankruptcies and business failures) but systematic, simultaneous and widespread investment mistakes can only occur through systematically distorted price signals, and these result in depressions or recessions. Austrians believe systemic malinvestments occur because of unnecessary and counterproductive intervention in the free market, distorting price signals and misleading investors and entrepreneurs. For Austrians, prices are an essential information channel through which market participants communicate their demands and cause resources to be allocated to satisfy those demands appropriately. If the government or banks distort, confuse or mislead investors and market participants by not permitting the price mechanism to work appropriately, unsustainable malinvestment will be the inevitable result.

To summarize, belief that “this time is different!” and “we are in a new paradigm!” is one of the classic hallmarks of economic bubbles. Though the Fed and other central banks have created an unusually long economic cycle by keeping their monetary policies so loose for so long, there is no escaping the eventual correction of the tremendous excesses and malinvestments that have built up in the past decade. To believe that the Fed has finally tamed the business cycle and can create sustainable economic growth without busts is extremely naive and will be disproven in the not-too-distant future.