Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

And now the biggest boom of all.

The Nasdaq has dropped 8% from its intraday high on October 1, and now the real estate industry in the San Francisco Bay Area has its collective eyes fixed on it because there is an uncanny dependency on tech stocks.

The cause-and-effect relationship between tech-stock prices and real estate in San Francisco is not perfectly agreed-upon. One thing is sure: when the Nasdaq surges for an extended period of time, office rents shoot sky-high, and when the Nasdaq plunges, office rents plunge along with it. But when it comes to home prices, it’s complicated, as they say.

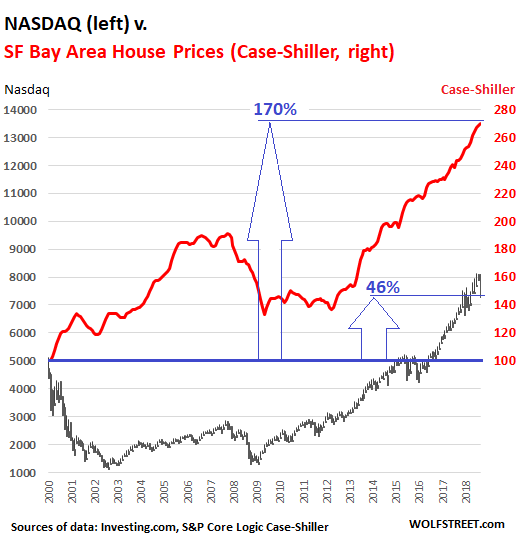

We’ll start with the relationship between the Nasdaq and home prices as measured by the S&P CoreLogic Case-Shiller Home Price Index for “San Francisco.” The Case-Shiller covers house prices (not condo prices) in the five Bay Area counties of San Francisco, San Mateo (northern part of Silicon Valley), Alameda and Contra Costa (both in the East Bay) and Marin (North Bay). This area is home to a lot of tech companies and near a lot of other tech companies in the South Bay.

The Nasdaq, now at 7,449, is up 46% from the crazy dotcom-bubble peak of March 2000 (5,132). Over the same period, house prices in the five-county Bay Area have surged 170%.

As a reminder for those who’ve graciously forgotten: The Nasdaq plunged 76% from that bubble peak to 1,192 by July 2002, and as measured from that low, has since soared 524%, but remains far behind the home-price increases.

This chart shows the monthly Nasdaq ranges (black) and the Case-Shiller index for “San Francisco.” The horizontal fat blue line depicts the starting point for both:

In the year 2000 and in early 2001, the Case-Shiller index soared 34%, still boosted by the Nasdaq gains of pre-March 2000 and the hope that the tech-stock collapse was just a regular sell-off. Also, the Case-Shiller, by the way it is designed, lags several months behind actual home price changes.

But by mid-2001, both headed south together, with the Case Shiller dropping 12% over the next 12 months.

By the end of 2002, the Greenspan Fed’s low interest rates started to inflate the San Francisco housing market with a vengeance. Tech stocks followed six months later.

From mid-2003 until October 2007, both surged: The Nasdaq 126%; the Case-Shiller 58%, but off a much larger base, and thus continued to run away from the Nasdaq.

At the end of 2007, both headed south together: the Nasdaq plunged 53%. The Case-Shiller plunged 30% from super-lofty highs.

The Nasdaq bottomed out in March 2009 and began to skyrocket, gaining 440% since then. The Case-Shiller began to skyrocket at the beginning of 2012, gaining over 100%, but from a much higher base.

There are other standouts from the chart:

- This – the Nasdaq being up 46% in 18 years – is in part what you get when you measure a volatile stock market from its bubble-peak: It just doesn’t do that well on that basis, and that’s why it is rarely measured that way.

- The housing market in the SF Bay Area has been totally crazy over the past 18 years: up 170%. Over the same period, inflation as measured by CPI rose 47%.

- The Nasdaq would have to surpass 13,700 to catch up with the Case-Shiller home price index for San Francisco.

- The Case-Shiller index only goes back to the year 2000. Hence the limits of this chart.

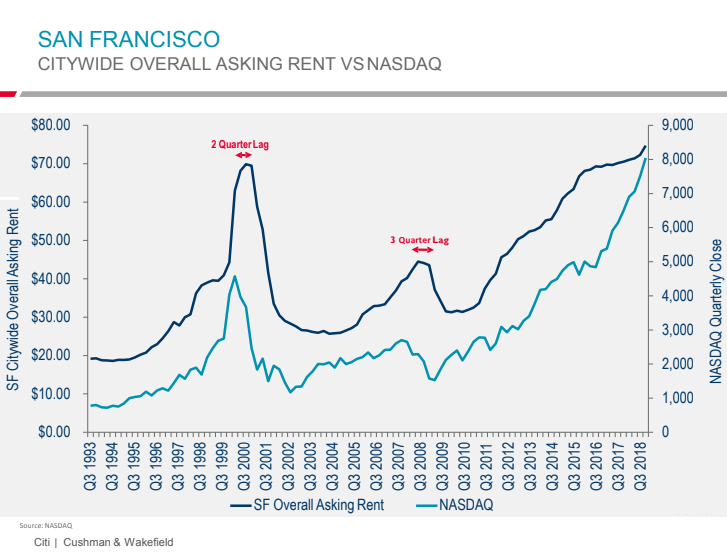

In terms of the Nasdaq and office rents in San Francisco, the picture is a lot clearer. Reza Musavi at the San Francisco office of Cushman & Wakefieldprovided this chart showing the quarterly close of the Nasdaq and quarterly office asking rents per square foot per year in the City of San Francisco (not including the surrounding counties; click to enlarge):

The chart depicts overall asking rents for the city of San Francisco, from the super-high-dollar rents downtown to the somewhat less breathtakingly high rents in other areas of the city, across all classes of buildings. Turns out, San Francisco office asking-rents move in-near lockstep with the Nasdaq, but lag two or three quarters behind.

Since the chart goes back to 1993, it covers the mega-bubble leading up to 2000, the smaller office-rent bubble leading up to 2007, and the greatest-of-all bubbles currently underway. And real estate pros who’ve been through this know where this is going. Boom and bust, always in San Francisco.