by Tom Allen

As a business owner, how can you maximize your tax deductions and improve employee loyalty simultaneously?

“Everything should be made as simple as possible, but no simpler.” – Albert Einstein

In a world of increasing automation, the role of a true consultant is to respect the individual and not “place them in a box.” The 401(k) industry is quite notorious for this as they constantly look to simplify the client’s life.

Respect the Individual Client

But simplicity does not necessarily mean automated or “turnkey.” A LOT of value gets left on the table by oversimplifying a client’s situation.

In today’s case study, I present a typical scenario that gets placed in the “simple box.” I recently worked with a husband and wife that own their own realty company. The company is having a blockbuster year coming out of the pandemic. As such, their CPA recommended that they start to diversify their assets outside of their business and establish a 401(k) plan.

Fantastic!

Now what often convolutes offering benefits within a company are the employees. The IRS allows tax benefits to employers. However, there are “strings attached” as they cannot “discriminate” against non-owner employees. This couple happens to have one full-time employee and will hire another within the next 12 months.

The Discovery Process

Our process begins with understanding the end goal we are trying to solve. In this specific case, we will try to maximize tax deductions to the owners. Also, the goal is to keep expenses low, accommodate the non-owner employee, and plan for another hire within the year.

Situations like these rely heavily on efficient plan design to maximize tax deductions to the business owners and service provider selection to keep costs reasonable and service that is commensurable to their needs. For example, the service requirements for a small business with three total employees look a lot different than a Fortune 500 company with 1,000 employees across multiple office locations. You don’t want to end up overpaying or underpaying for services that don’t fit your specific scenario.

Within a 401(k) plan, there are essentially 3-buckets of money:

- Employee Deferrals – these can be Pre-Tax or Roth up to $19,500 per year or $26,000 for those age 50 or older

- Employer Matching Contributions – these are very common in most 401(k) plans as an incentive for employees to save

- Employer Non-Elective Contributions – these are contributions made to employees’ accounts without employees having to do anything. They are additional contributions from the employer

Profit-Sharing Benefits

Outside of employee deferrals and employer matching contributions, most employers utilize profit-sharing contributions for their non-elective contributions. The IRS allows third party administrators (i.e., the party responsible for compliance with the plan) four different ways to allocate profit-sharing contributions:

- Pro-Rata – everybody gets the same percentage of compensation

- Integrated – takes into account payroll taxes paid by the employer when determining benefits

- Age-Weighted – gives larger allocations to those individuals who are older

- New Comparability – considers the ages and compensation of all employees to determine “beneficial accrual rates” for each employee. If those accrual rates are within certain limits, the plan passes testing. To give the “cliff notes,” if an owner is relatively older and makes more money than most of their employees, the higher their profit-sharing allocation can be relative to their employees.

Efficient Plan Design

Going back to our couple, here are the specifics that we took into consideration when designing their plan:

- Both husband and wife want to max out their contributions (i.e., $58,000 per year each)

- Both are about the same age as their one non-owner employee

- The majority of contributions are coming from the owners

- Utilize Quickbooks as their payroll provider

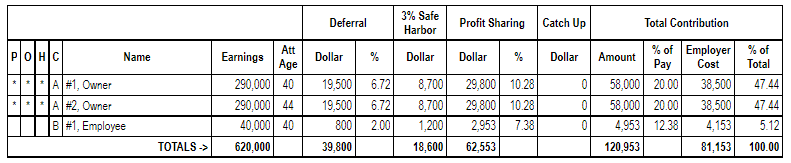

We decided to go with a Safe Harbor 401(k) Plan that utilizes an integrated profit-sharing allocation formula from a plan design standpoint. Here is how it is stacked out:

The key columns to pay attention to are the Profit-Sharing columns. The vast majority of employer non-elective contributions went to the owners (i.e., $29,800 each) and a higher percentage of total compensation (i.e., 10.28% vs. 7.38%). Why does this matter?

If I were to simply put these clients in the “simple box” and did Pro Rata (very typical in small business plans), the employer would have ended up paying an additional 2.90% of their one employee’s compensation simply because somebody didn’t take the time. That’s an additional $1,160 per year of unnecessary contributions. The result is an efficient plan design that gives the two owners 95% of total employer contributions.

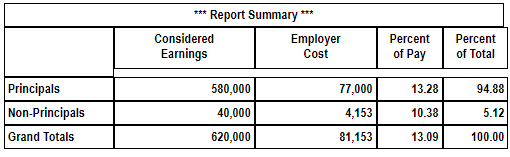

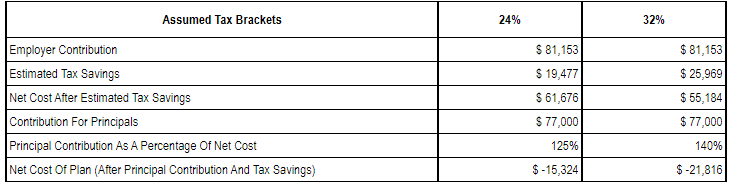

In terms of tax savings to the two owners, we created a net benefit of ~$21,816 per year, assuming a 32% effective tax rate.

In other words, after we take into account the after-tax contributions the employer has to make to the plan (i.e., $55,184), there is a net benefit to the owners since they are taking home $77,000.

Don’t Overspend

From a service provider standpoint, I wanted to find a bundled provider that was flat fee, had a dedicated relationship manager attached to it, and could integrate with Quickbooks payroll. “Bundled” means that the same service provider does the Third-Party Administration and Recordkeeping. Alongside an integrated payroll solution, it saves employers time as owners typically wear many hats in a 3-person company. Such is where we can make their life simple.

For expenses, here is what it came out to:

- One-Time Start-Up Fee: $1,000

- Annual Service Fee: $2,560

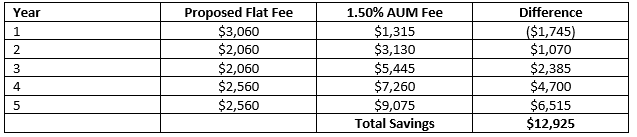

Once we account for the Retirement Plan Start-Up Cost Tax Credit of $500 per year for the first 3-years of the plan’s existence afforded to them by the IRS, the total first-year cost of the plan is $3,060.

Here is where service provider selection becomes crucial. Based on the plan design illustration above, the plan expects about $121,000 in contributions per year. 96% of those contributions are coming from the two owners. What if we went with a service provider that charged by assets under management of 1.50%?

Here is what expenses would look like for the first 5-years, not considering return on the investments in the plan or advisor expenses.

As you can see, the savings add up over time. Again, the flat fee approach works incredibly well for small businesses because most contributions are coming from the owners. In terms of service provider economics, most of their work gets driven by headcount, not contributions. So if a small business is not looking to grow outside of adding an employee once every couple of years, don’t overpay your service provider by using the AUM model.

Conclusion

Simplification can have its place, but it should not be the “end all, be all” when it comes to plan design. You could be leaving A LOT of value on the table with improper plan designs and service provider selection.

If you are interested in a no-obligation assessment of your company’s 401(k) plan and how RIA Advisors can help you level up, feel free to contact me directly.