via Luke Kawa

The biggest use of cash among S&P 500 companies is making their public footprints smaller — a strategy that’s paid dividends in 2018.

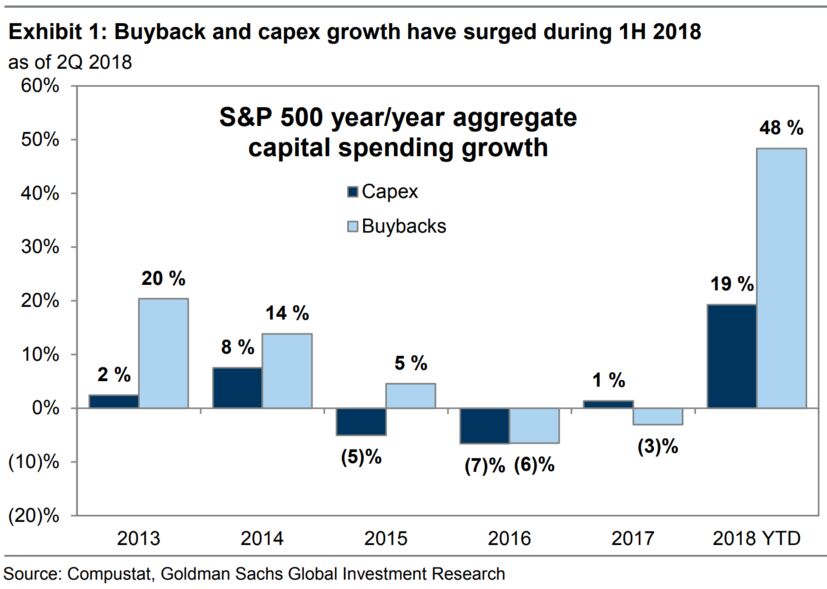

According to Goldman Sachs, aggregate share repurchases (or buybacks) rose by nearly 50 percent to $384 billion in the first half of 2018. That tops the $341 billion spent on capital expenditures, which are rising at the fastest pace in at least a quarter century.

“For the first time in 10 years, buybacks are garnering the largest share of cash spending by S&P 500 firms,” writes chief U.S. equity strategist David Kostin. “Capital spending has typically represented the largest single use of cash by corporations, a position it has held for 19 of the past 20 years.”

However, limits on companies’ ability to conduct discretionary buybacks ahead of their earnings announcements constitutes “a near-term risk” for U.S. stocks as this removes one potential buyer of any dips, which could exacerbate moves to the downside.

“Since 2000, S&P 500 returns have been comparable in blackout and non-blackout periods, but realized volatility has been nearly 1 point higher in blackout periods than when a majority of firms are free to repurchase stock,” the strategist writes.

The 2018 increase in share shrinkage is fairly narrow, with Apple alone accounting for roughly one quarter of the rise in buybacks. Goldman’s buyback desk expects repurchase authorizations to top $1 trillion in 2018.

Critics contend that buybacks are a product of self-interested, short-term thinking among executives that exacerbate wealth inequality and come at the expense of activities that would boost economic activity and a firm’s longer-term prospects. But the near 20 percent rise in business investment during the first half among S&P 500 companies highlighted by Goldman suggests that genuine growth opportunities aren’t being starved of capital.

Growth stocks should continue to fare better than their less expensive counterparts as the speed of the U.S. economic expansion wanes, Kostin expects. He recommends growth-oriented investors focus on a basket of firms with the highest ratio of R&D and capital spending (net of depreciation) as a share of their cash flow from operations, a group that’s going almost as well as buyback-biased firms in 2018.