There is a disparity happening in the country.

No, it isn’t political partisanship, but rather “economic confidence.”

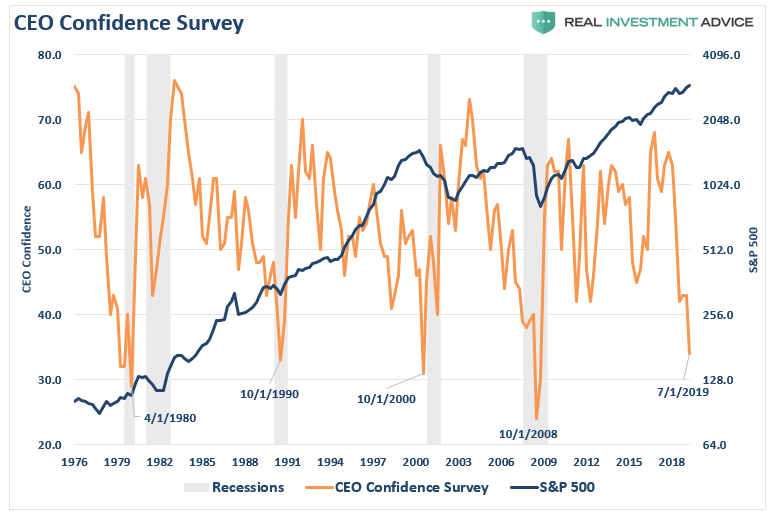

The latest release of the University of Michigan’s consumer sentiment survey rose to a three-month high of 96, beat consensus expectations, and remains near record levels. Conversely, CEO confidence in the economy is near record lows.

It’s an interesting dichotomy.

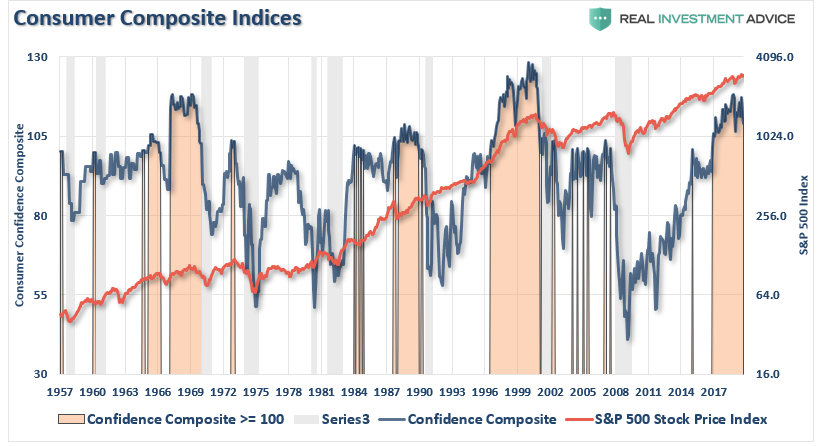

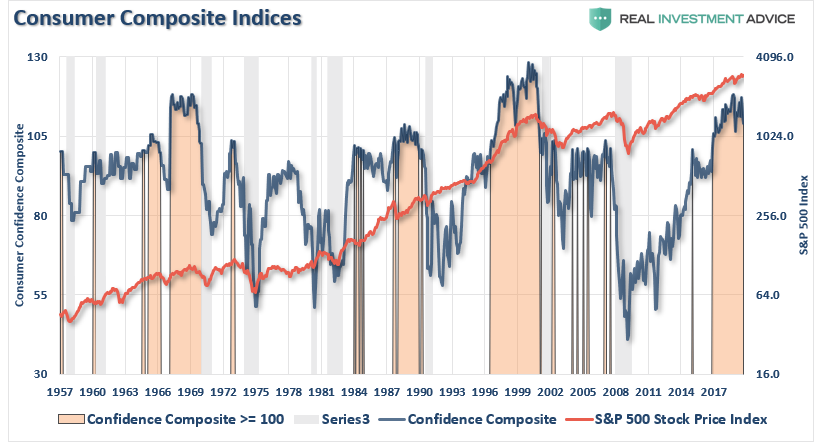

The chart below shows our composite confidence index, which combines both the University of Michigan and Conference Board measures. The chart compares the composite index to the S&P 500 index with the shaded areas representing when the composite index was above a reading of 100.

On the surface, this is bullish for investors. High levels of consumer confidence (above 100) have correlated with positive returns from the S&P 500.

However, high readings are also a warning sign as they then to occur just prior to the onset of a recession. As noted, apparently, consumers did not “get the memo” from CEO’s.

So, who’s right?

Is it the consumer cranking out work hours, raising a family, and trying to make ends meet? Or the CEO of a company who is watching sales, prices, managing inventory, dealing with collections, paying bills, and managing changes to the economic landscape on a daily basis?

Michael Arone, chief market strategist at State Street Global Advisors, recently told MarketWatch:

“I’m not sure if we’ve seen this disparity between positive consumer sentiment and negative business confidence at this level. From my perspective, something has to give. Either businesses have to be more confident, or you’re likely to see more rollover on the consumer data.”

Actually, a quick look at history shows this level of disparity is not unusual. It happens every time prior to the onset of a recession.

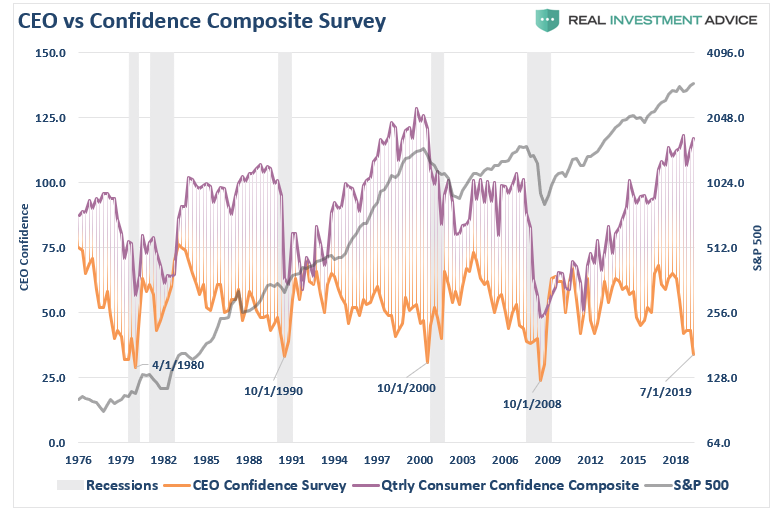

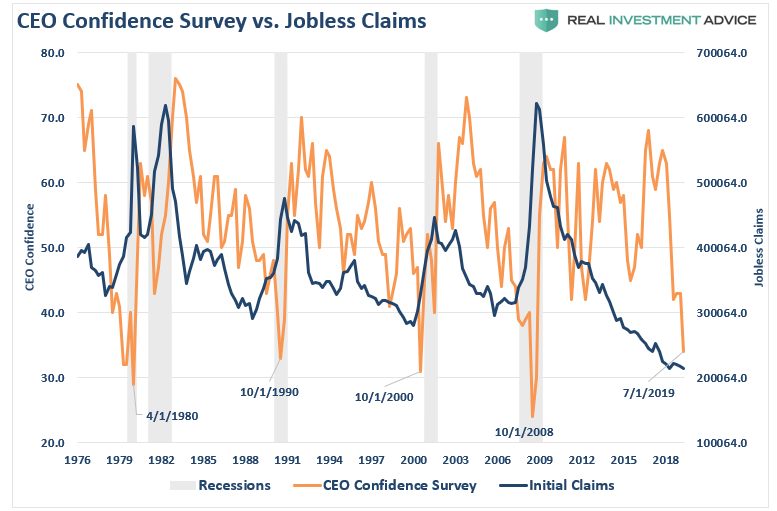

Take a closer look at the chart above.

Notice that CEO confidence leads consumer confidence by a wide margin. This lures bullish investors, and the media, into believing that CEO’s really don’t know what they are doing. Unfortunately, consumer confidence tends to crash as it catches up with what CEO’s were already telling them.

What were CEO’s telling consumers that crushed their confidence?

“I’m sorry, we think you are really great, but I have to let you go.”

It is hard for consumers to remain “confident,” and continue spending, when they have lost their source of income. This is why consumer confidence doesn’t “go gently into night,” but rather “screaming into the abyss.”

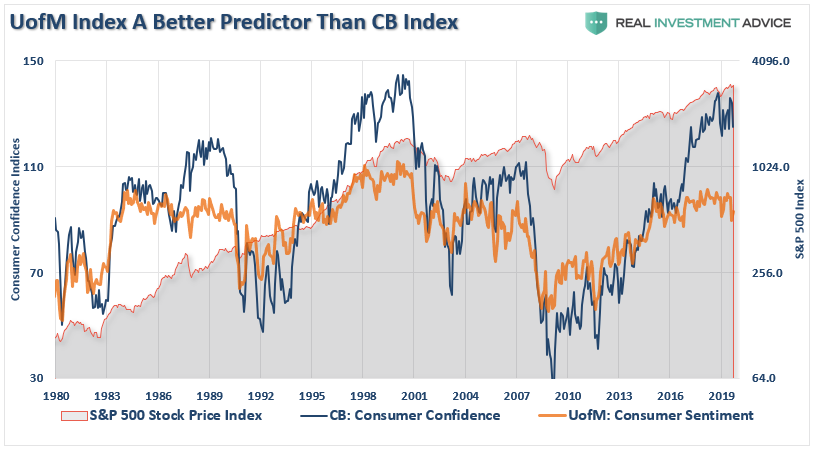

UofM A Better Predictor

As noted above, our composite indicator is the average of both the University of Michigan and Conference Board measures. Of the two measures, the UofM index is the better index to pay attention to.

As shown above, while the Conference Board is near all-time highs suggesting the consumer is “strong”, the UofM measure is sending quite a different message. Not only has it turned lower, confirming the recent weakness in retail sales, but also has topped at a lower high than then previous two bull market peaks.

As shown above, while the Conference Board is near all-time highs suggesting the consumer is “strong”, the UofM measure is sending quite a different message. Not only has it turned lower, confirming the recent weakness in retail sales, but also has topped at a lower high than then previous two bull market peaks.

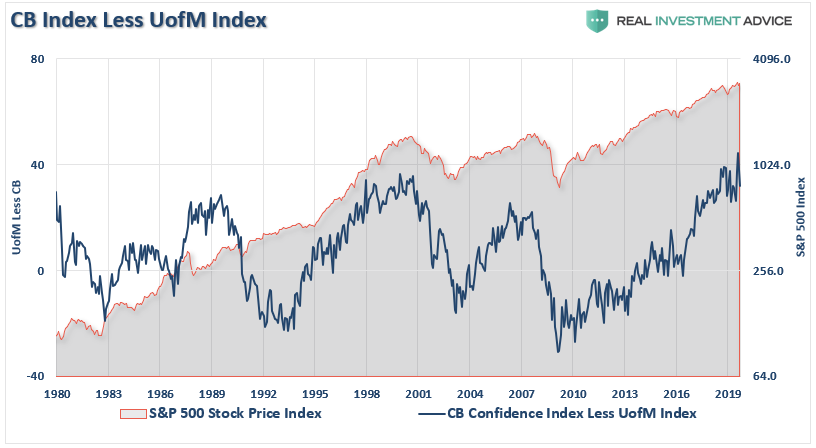

The chart below subtracts the UofM measure from the Conference Board index to show the historical divergence of the two measures. Importantly, the Conference Board measure is always overly optimistic heading into a recession and bear market, then “catches down” to the UofM measure.

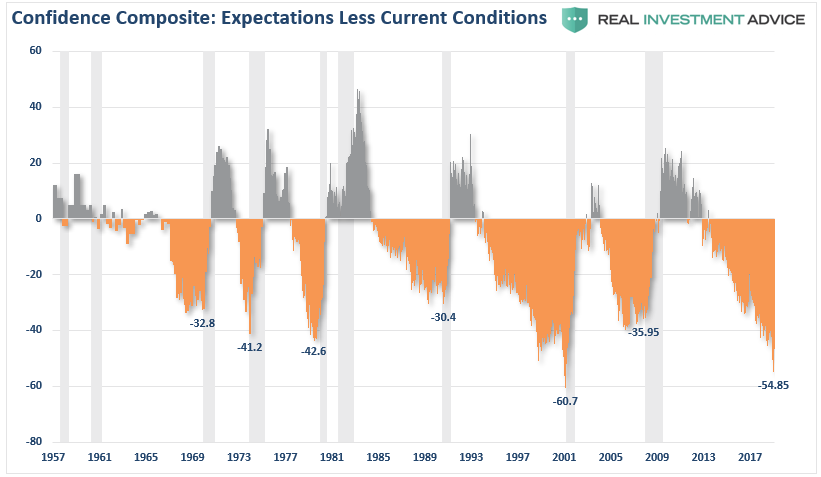

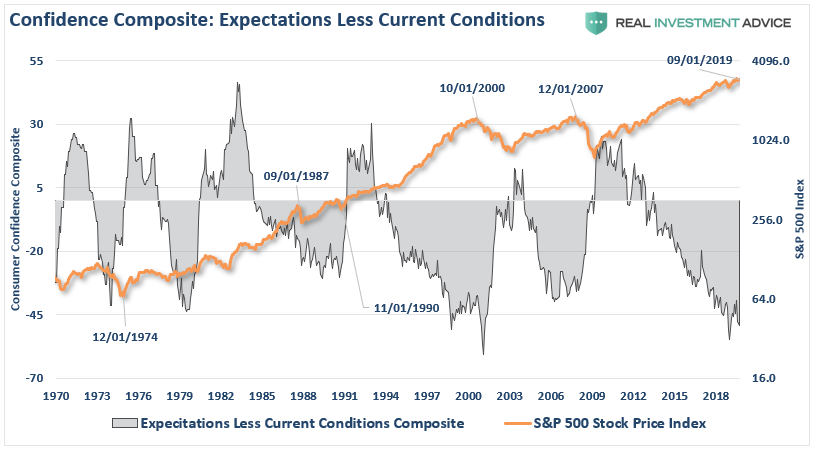

Another way to analyze confidence data is to look at the consumer expectations index minus the current situation index in the consumer confidence report.

This measure also is signaling a recession is coming. The differential between expectations and the current situation, as you can see below, is worse than the last cycle, and only slightly higher than prior to the “dot.com” crash. Recessions start after this indicator bottoms, which has already started happening.

Given that GDP is roughly 70% consumption, deterioration in economic confidence is a hugely important factor. The most significant factors weighing on that consumption, as noted above, are job losses which crushes spending decisions by consumers.

This starts a virtual spiral in the economy as reductions in spending put further pressures on corporate profitability. Lower profits lead to more unemployment, and lower asset prices, until the cycle is complete. Note, bear markets end when the negative deviation reverses back to positive.

Currently, the bottoming process, and potential turn higher, which signals a recession and bear market, appears to be in process.

None of this should be surprising as we head into 2020. With near record low levels of unemployment and jobless claims, combined with record high levels of sentiment, job openings, and near record asset prices, it seems to be just about as “good as it can get.”

However, that is also a point to consider, as I wrote previously:

“’Record levels” of anything are “records for a reason.”

As Ben Graham stated back in 1959:

“‘The more it changes, the more it’s the same thing.’ I have always thought this motto applied to the stock market better than anywhere else. Now the really important part of the proverb is the phrase, ‘the more it changes.’

The economic world has changed radically and will change even more. Most people think now that the essential nature of the stock market has been undergoing a corresponding change. But if my cliché is sound, then the stock market will continue to be essentially what it always was in the past, a place where a big bull market is inevitably followed by a big bear market.

In other words, a place where today’s free lunches are paid for doubly tomorrow. In the light of recent experience, I think the present level of the stock market is an extremely dangerous one.”

He is right, of course, things are little different now than they were then.

For every “bull market” there MUST be a “bear market.”

This time will not be “different.”

If the last two bear markets haven’t taught you this by now, I am not sure what will.

Maybe the third time will be the “charm.”