by Anthony B Sanders

It is quite a start to the New Year! Goldman Sachs issues a warning over extreme levels of risk appetite while, at the same time, cash flows are slowing.

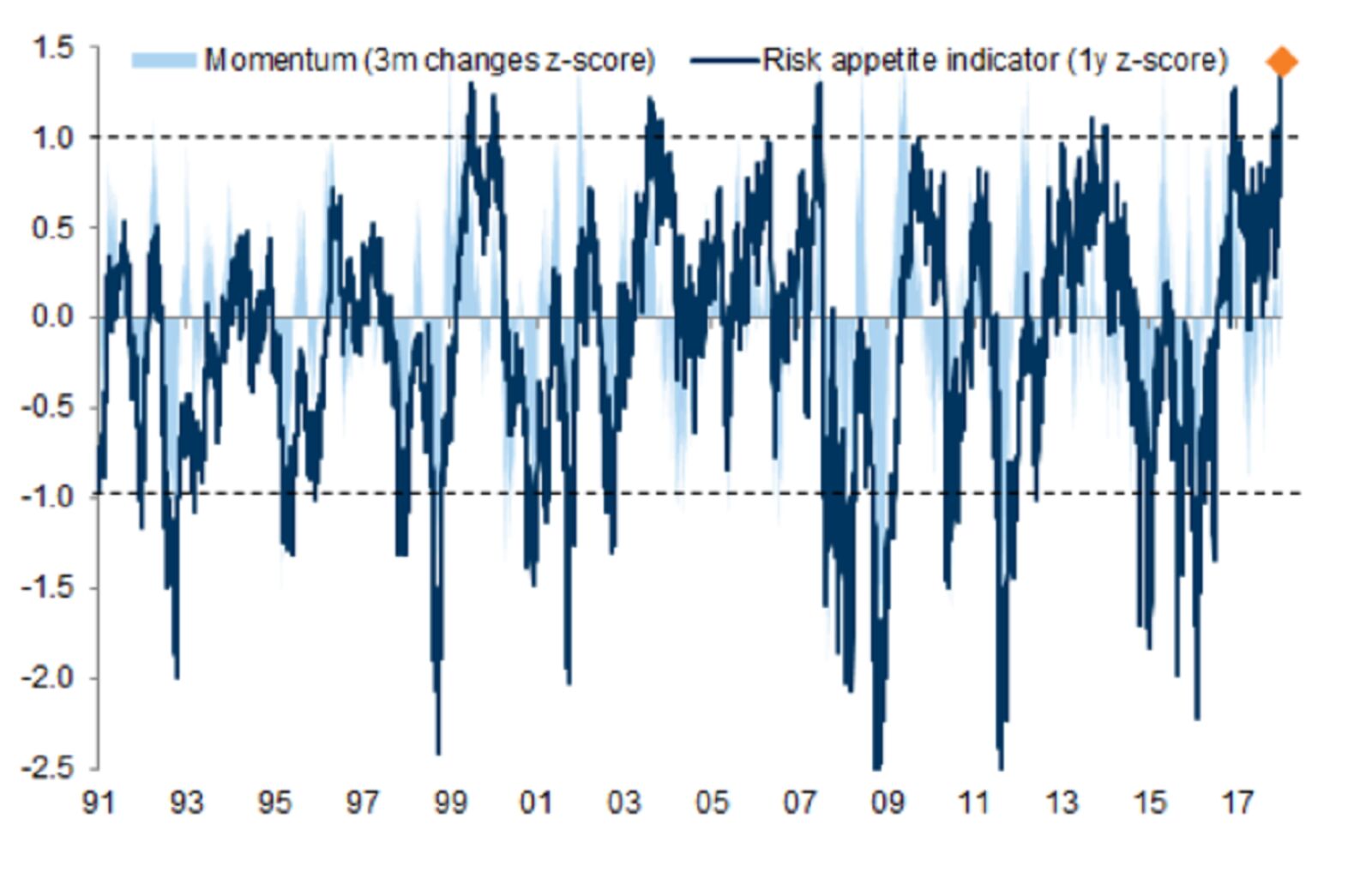

(Bloomberg) Global stocks and U.S. Treasuries are in the throes of their most “extreme” start to the year ever as bullish sentiment engulfs markets, according to Goldman Sachs Group Inc.

The bank’s cross-asset measure of risk appetite around the world is the highest since it started the gauge in 1991. Euphoria is turbo-charging global equities while 10-year U.S. government bonds are suffering their worst performance in risk-adjusted terms, according to Goldman.

“Risk appetite is now at its highest level on record, which leads to the question of what future returns can be,” strategists including Ian Wright wrote in a Monday note.

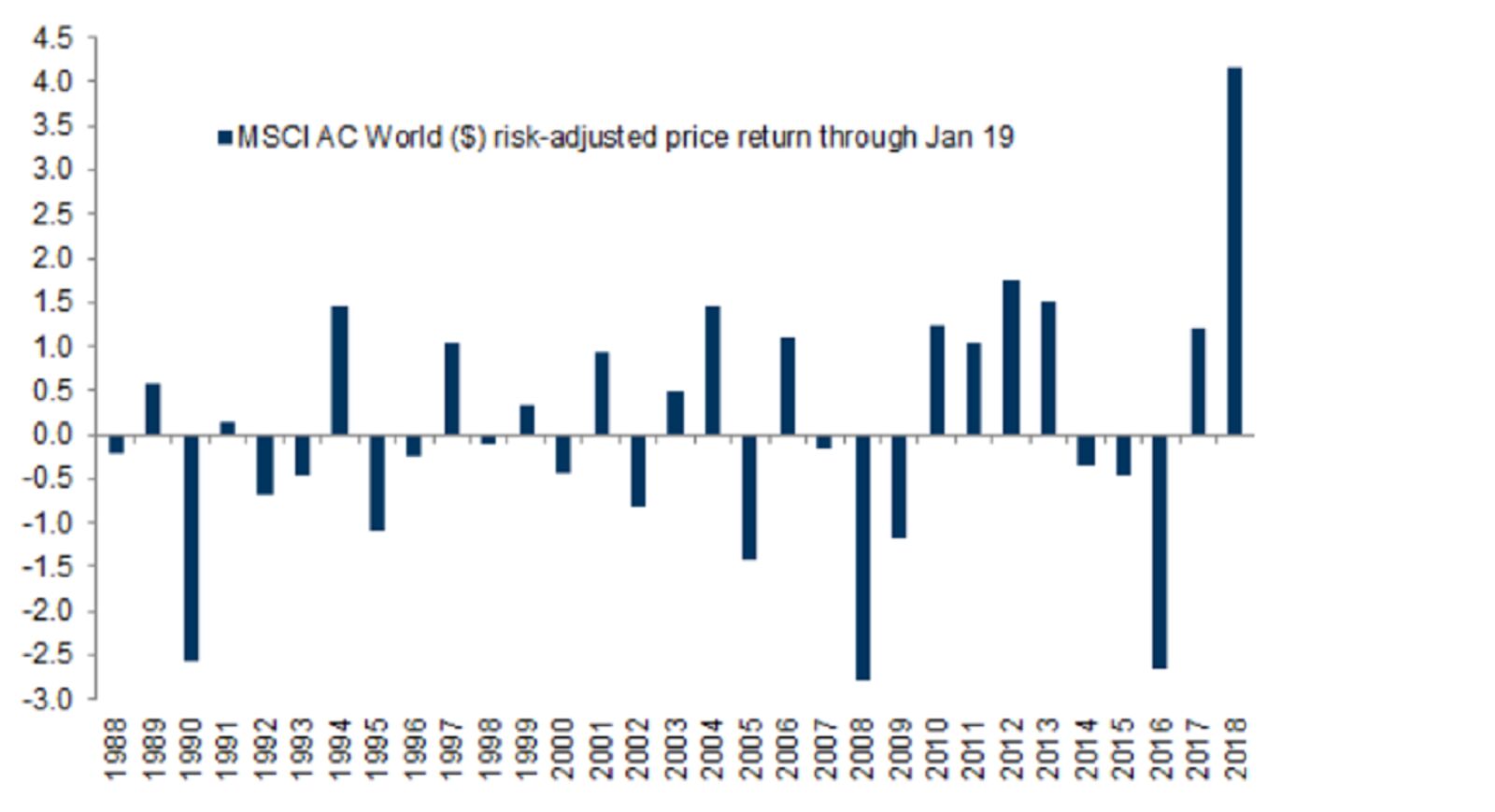

Investors are enjoying the fastest global expansion since the start of the decade, strong corporate earnings growth and stable economic data. Equities around the world have added over $4 trillion this year, even as major gauges flash overbought signals, while premiums on U.S. corporate bonds are back to 2007 lows.

Goldman remains overweight stocks and underweight government bonds over a three- to 12-month horizon, citing strong global expansion and a hawkish monetary trajectory.

The economic outlook this year and next is better than previously anticipated but loose financial conditions and rich asset valuations suggest investors should guard against complacency, the International Monetary Fund said at the Davos gathering this week.

“While high risk appetite increases risk of disappointment, we find historically that the signal from macro data tends to trump the signal from risk appetite,” Goldman said.

(Bloomberg) Amidst the euphoria over fresh record highs in U.S. stocks, Societe Generale SA is among a few investment firms now highlighting warning signs for investors.

Concerns over a flattening U.S. Treasury yield curve — a sign to some of a coming economic slowdown — have quieted down for the moment, thanks to the recent pick-up in longer-dated yields. But the potential slowdown message has an echo in diminishing corporate cash flows, SocGen strategists including Andrew Lapthorne have highlighted.

The slowdown for the broader group of companies is noteworthy because it’s coincided with both a slump in the dollar and a decline in the yield curve, said the strategists. An inverted yield curve, which will occur if the trend continues, has historically come before economic slumps like the one that started about 10 years ago. And a falling dollar could reflect relatively more positive investor sentiment about economies outside the U.S.

“If the cash-flow growth signal is correct, and that reinforces the yield-curve view” of the U.S. outlook, “then equity markets could be in for a nasty surprise,” according to SocGen.

One caused of this dysfunctional parable? Global Central Bank balance sheets are staggering in size (over $14 trillion).

Yes, it is time for Ozzy Osbourne’s “Crazy Train” again.

And the Federal Reserve is changing engineers on their crazy train. From Yellen to Powell.