via wallstreetonparade:

Spasms in big Wall Street bank stocks have been happening on a serial basis over the past three years. (See here and here.) Yesterday offered another one of those bank warning signs to a Congress intent on further deregulation of an already dangerously deregulated market.

As the stock market grappled yesterday with fears of sinking emerging market currencies leading to loan defaults at European banks that are derivative counterparties to the biggest banks on Wall Street, the Wall Street banking sector was a sea of red. Two banks in particular sold off more than others.

Deutsche Bank is the big German lender that trades on the New York Stock Exchange. It closed with a loss of 2.61 percent versus a much milder decline of 0.76 percent in the Standard and Poor’s 500 Index. Posting a final trade of $11.19, Deutsche Bank closed at just 83 cents above its all time closing low of $10.36 which came in late June. This leaves Deutsche Bank with a scant $23.1 billion in equity market value to support a notional (face amount) derivatives book of 48 trillion euros or roughly 54.6 trillion U.S. dollars. Deutsche Bank has lost 75 percent of its market value over the past five years while it has continued to remain heavily engaged as a counterparty to global bank derivative trades.

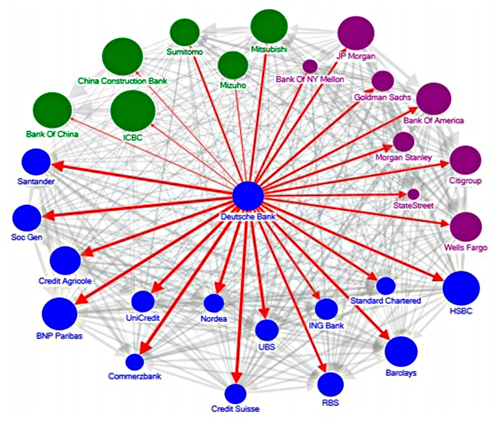

In 2016 the International Monetary Fund (IMF) issued a report that set off alarm bells about the potential for systemic banking contagion to emanate from Deutsche Bank as a result of its counterparty exposures. The report provided a graphic (see below) that demonstrated that problems at Deutsche could spill over onto such big Wall Street banks as Morgan Stanley, JPMorgan Chase, Citigroup, Bank of America and Goldman Sachs. Those five banks just happen to be where derivatives are deeply concentrated in the U.S.

Deutsche Bank’s 2017 Annual Report contains additional cause for alarm. It shows that 28 percent of Deutsche Bank’s €48 trillion derivatives book is not being centrally cleared but is simply bilateral contracts between it and another party. (That represents approximately 15.28 trillion U.S. dollars for a bank with $23.1 billion in equity capital.) That means that Deutsche Bank and whomever is on the other side of those derivatives trades are on the hook to each other for any losses, as opposed to a central clearing party (CCP) backing the trade. The lack of central clearing parties for derivative trades is why the big life insurer AIG required a $185 billion backstop from the U.S. taxpayer to prevent it from defaulting on its massive credit default derivative trades with Wall Street and global banks during the 2008-2009 financial crisis. It is also why Lehman Brothers imploded in short order in the 2008 Wall Street crash.

A rational person might expect that the U.S. Senate Banking Committee, the House Financial Services Committee and the Senate’s Permanent Subcommittee on Investigations would be all over this situation, hauling in executives, subpoenaing documents and taking testimony under oath. Nothing of the sort has happened.

Deutsche Bank is effectively living in the fantasy world that regulators allowed Citigroup to inhabit in the leadup to the 2008 crash. As former FDIC Chair Sheila Bair wrote in her book, Bull by the Horns:

“By November [of 2008], the supposedly solvent Citi was back on the ropes, in need of another government handout. The market didn’t buy the OCC’s and NY Fed’s strategy of making it look as though Citi was as healthy as the other commercial banks. Citi had not had a profitable quarter since the second quarter of 2007. Its losses were not attributable to uncontrollable ‘market conditions’; they were attributable to weak management, high levels of leverage, and excessive risk taking. It had major losses driven by their exposures to a virtual hit list of high-risk lending; subprime mortgages, ‘Alt-A’ mortgages, ‘designer’ credit cards, leveraged loans, and poorly underwritten commercial real estate. It had loaded up on exotic CDOs and auction-rate securities. It was taking losses on credit default swaps entered into with weak counterparties, and it had relied on unstable volatile funding – a lot of short-term loans and foreign deposits. If you wanted to make a definitive list of all the bad practices that had led to the crisis, all you had to do was look at Citi’s financial strategies…What’s more, virtually no meaningful supervisory measures had been taken against the bank by either the OCC or the NY Fed…Instead, the OCC and the NY Fed stood by as that sick bank continued to pay major dividends and pretended that it was healthy.”

This year marks the tenth anniversary of that epic crash on Wall Street that wiped out the jobs and life savings of millions of Americans, and yet, the regulators and Congress are repeating the same negligent behavior they exhibited in the leadup to the crash. They are ignoring the buildup of risks and allowing the gutting of the Office of Financial Research, the very agency created to warn about those risks. (See here and here.)

It is noteworthy that Citigroup did not trade well yesterday either, losing 1.94 percent to close at $68.65. That nice sum looks a lot better than it really is. Without the dodgy 1-for-10 reverse stock split that Citigroup did in 2011 (leaving shareholders with 1 share for each previous 10 shares), it would have closed yesterday at $6.87. Citigroup is, in reality, trading 88 percent below where it was trading in early 2008.

According to a report from the Office of the Comptroller of the Currency (OCC), as of March 31, 2018 Citigroup’s holding company had a notional book of $56.6 trillion in derivatives, second only to Goldman Sachs’ holding company which had $59.2 trillion notional. The OCC also noted that only 51 percent of Citigroup’s derivatives are centrally cleared versus 49 percent that are not.

Nothing more clearly demonstrates that Congress is marching to the beat of Wall Street’s demands than this.

Systemic Risk Among Deutsche Bank and Global Systemically Important Banks (Source: IMF 2016 — “The blue, purple and green nodes denote European, US and Asian banks, respectively. The thickness of the arrows capture total linkages (both inward and outward), and the arrow captures the direction of net spillover. The size of the nodes reflects asset size.”)