As Dire Straits almost sang, “Money For (Almost) Nothing” but you have to pay fees.

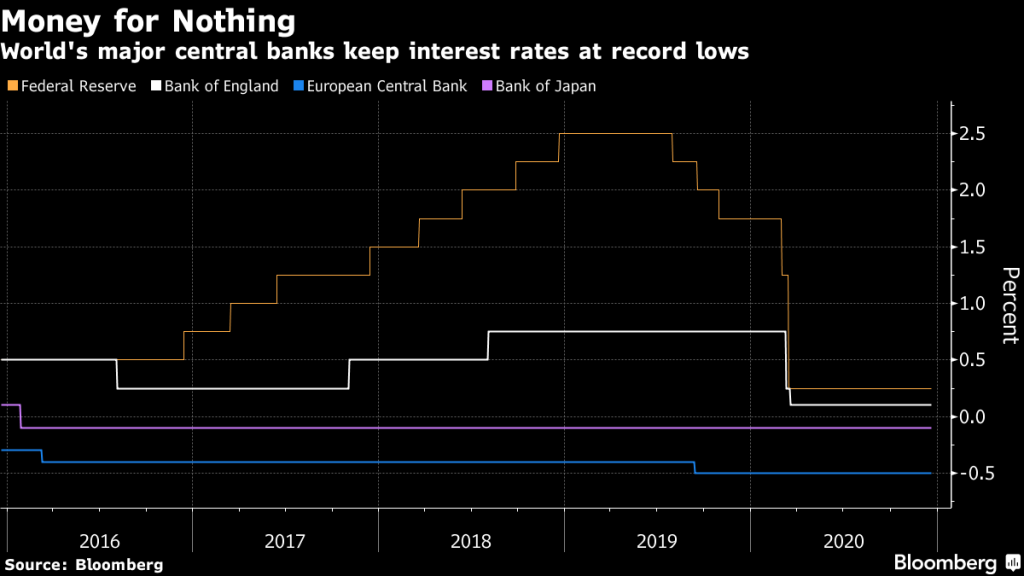

With Central Banks keeping interest rates near or below zero, …

European bank deposit rates are still above zero, although close to zero which harm savers. A negative deposit rate is intended to encourage lenders to do something more useful with their money than park it with the ECB. But European banks are adding fees to already beleaguered savers.

(Bloomberg) In normal times, bankers who oversee assets exceeding $1 trillion wouldn’t be groping for loose change under the sofa.

But in the banking equivalent of hunting for pennies, European financial giants like Banco Santander SA and ING Groep NV are looking to squeeze more revenue from depositors. Wealth For YouHelp us deliver more relevant content for you by telling us about yourself. Answer 3 questions to tailor your experience.

Introducing charges and increasing fees show how a future of sub-zero interest rates is forcing euro-area banks to transfer more costs to clients. While the tactics could backfire by accelerating a shift of depositors into low-cost neobanks, they may help traditional lenders sell more lucrative products.

For a banker, “if you only have a current account with me, I lose money,” said Angel Corcostegui, former Santander CEO and founder of private equity firm Magnum Capital Industrial Partners. “Banks need to be a clearer about the costs that they assume.”

The move toward more fees will most likely have more impact on those who don’t have a steady paycheck or the means to buy financial products, said Patricia Suarez, president of financial consumer watchdog Asufin. “They’re separating more profitable clients from the less profitable ones,” she says.

In Spain, Santander will introduce a monthly charge in the new year of as much as 20 euros on current accounts for customers who don’t meet certain criteria, which include paying in salary and buying at least one other financial product. Banco Bilbao Vizcaya Argentaria SA is starting to charge customers over 29 years old who don’t pay in their salaries and use the account to pay bills. It will also begin charging 2 euros for using cashier services and 0.4% on transfers.

ING, which for many years advertised the appeal of no-fee current accounts in Spain, sent out an email to its customers there telling them it would begin charging 10 euros a month on holdings over 30,000 euros ($37,000) if the customer doesn’t use ING for their salary deposits or receive at least 700 euros a month in income.

A statement from ING cited “the unusual economic moment in which interest rates (which set the price of money) have been going down endlessly.” A Santander statement emphasized that “loyal” customers will avoid new fees.

At the other end of the spectrum, euro-area banks have also imposed new costs. Deutsche Bank AG and Commerzbank AG last year lowered the threshold to 100,000 euros for charging new retail depositors.

While Asian and American banks cans still count on positive rates, Europe’s half-a-decade experiment with negative interest rates has put pressure on lending revenue and burdened banks with billions of euros in penalties for parking cash with the central bank. In Denmark, where benchmark rates have been negative since 2012, most banks now charge clients on deposits exceeding a set amount.

Michael Soffe, a British expat who owns wedding and catering companies in Malaga, Spain, says he’s noticed a steady increase in fees on credit cards, debit cards and transfers. As an owner of a business account at Banco Unicaja SA, he was able to get some of those removed, although the charges he does pay have risen about fourfold in recent years. He’s also noticed a push to sell other products, such as house insurance.

“Bank charges have risen quite substantially,” Soffe said. “And they all want you to have insurance with the banks.”

The increase in fees and charges may represent an opportunity for digital-only banks such as Monzo Bank Ltd., Revolut Ltd. and N26 Bank GmbH, which thanks to lower cost structures may be able to lure new customers with the promise of no charges on services. Starling Bank Ltd., which also recently began lending, could prove an appealing alternative for consumers fleeing charges.

“Whenever there is a negative customer experience in a traditional bank, it opens the door for someone to come along and do it better,” said Joe Fielding, head of banking and payment practice for the Americas at Bain & Co. in New York. “’Better in today’s terms is inevitably digital.”

But with interest rates at record lows, a move to charging for those services makes sense, said Magnum Capital’s Corcostegui.

“What we’re going to see now is an unbundling of costs per service. We’ll move toward a pay-per-use system,” Corcostegui said in an interview. “Having a current account is a service that needs to be paid for, just like when you pay to catch a bus.”

So, European banks are now The Sultans Of Fees?

A German saver getting almost no interest on deposits but having to pay fees.