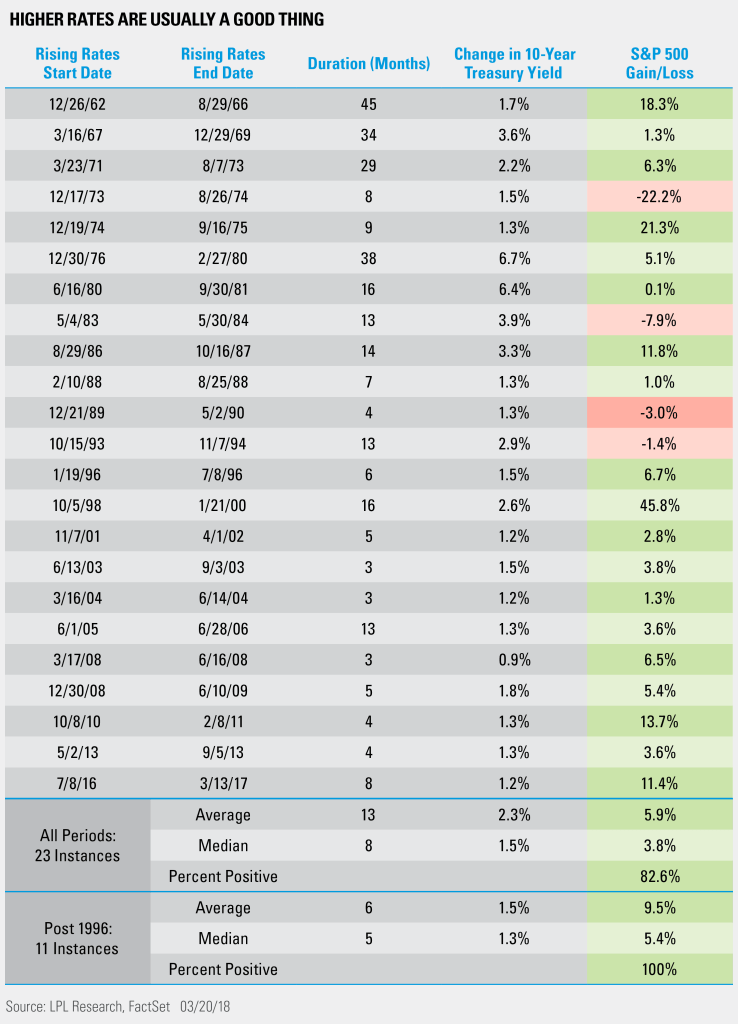

LPL Research recently penned an interesting post entitled “Why Stocks Like Higher Rates.”

“What does it mean for equities if rates and yields do indeed go higher? Fortunately, to the surprise of many, stocks historically do very well when rates increase. Since 1996, stocks gained all 11 times we saw higher rates,”

Here is the conclusion:

“Not to be outdone, the current period of higher rates began in September 2017 and the S&P 500 is up another 11% since then. History suggests higher rates may be a good thing and should the 10-year Treasury yield break about the critical 3% area, this could be further support for the bull market.”

The analysis is actually backwards.

Michael Lebowitz just wrote about this in Fasten Your Seat Belt, Turbulence Ahead. His article is worth reviewing to see what has really happened over entire rate cycles and not hand chosen dates to prove a point.

While the markets, due to momentum, may choose to ignore the effect of “monetary tightening” in the short-term, what about the longer-term? For example, one might think based on the LPL table above that the financial crisis of 2008 was positive for stock investors. The analysis shows that in 8 of the 15 months spanning from March 2008 to June 2009, equity holders had gains. While that is true, equity holders that did not get the memo with specific dates on when to buy and sell lost over 50%.

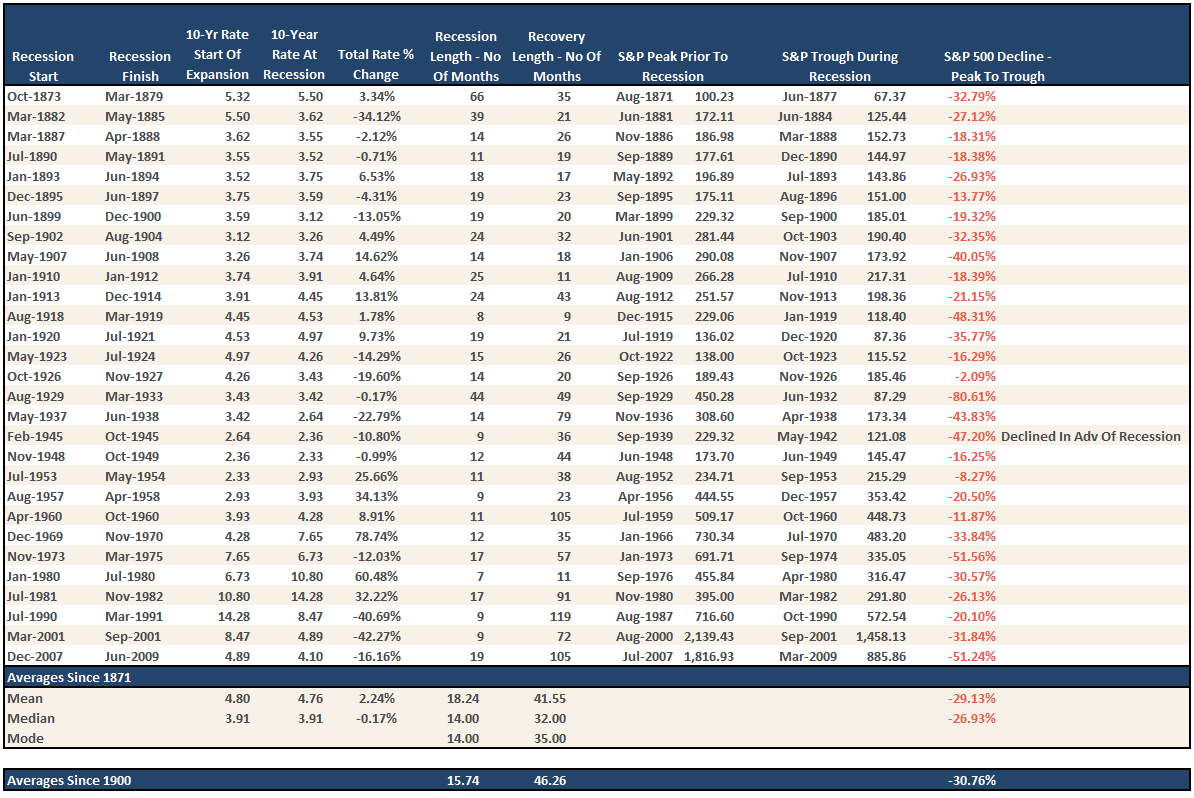

As shown in the table below, the bulk of losses in markets are tied to economic recessions.

However, while it is true the historical average interest rate where a recession was triggered was near 5%, averages are very deceptive.

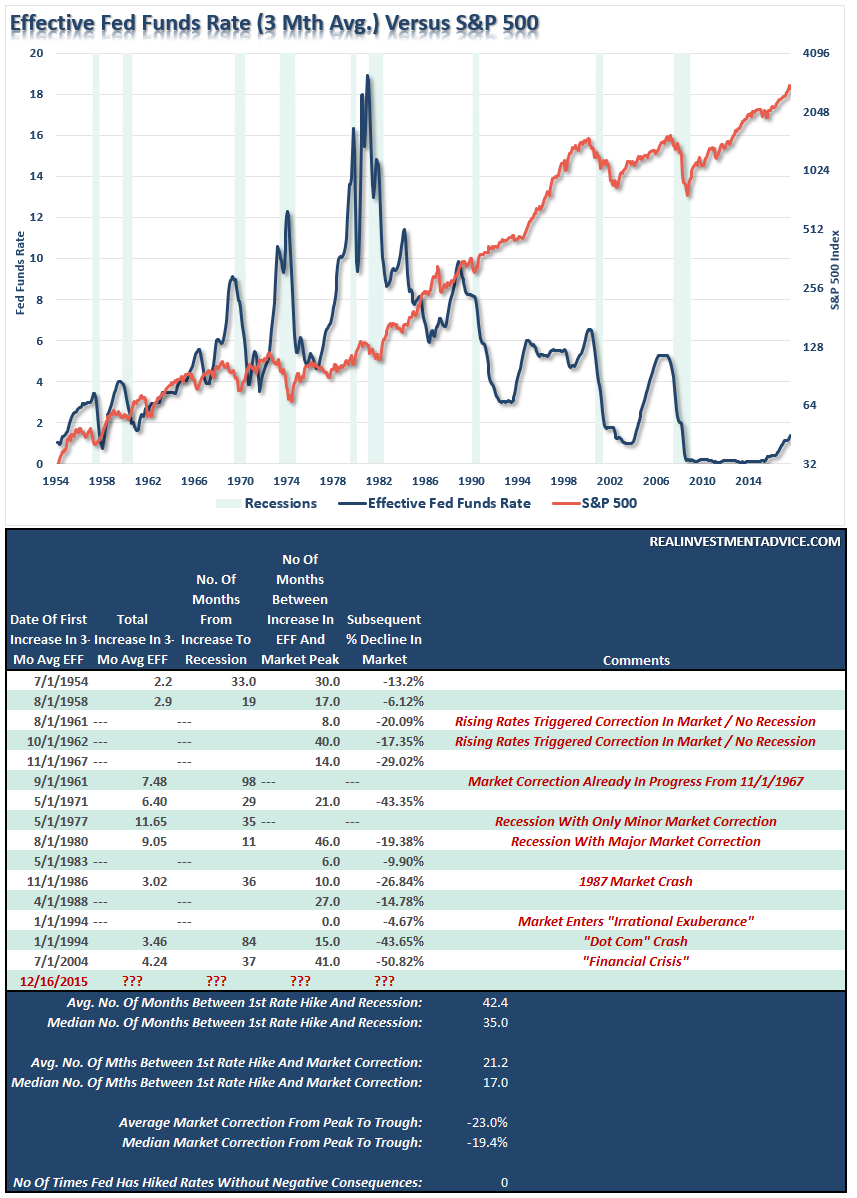

Of more importance than the nominal level, are the actions of the Federal Reserve which are typically reflected by the 10-year Treasury rate. The graph below shows the confluence of Fed Fund increases and recessions. The table below the graph shows the date of the first Fed rate hike, the number of months until the next event which was either a recession, a market correction or both, and the percentage decline in the stock market.

The point is that in the short-term the economy and the markets (due to the current momentum) can DEFY the laws of financial gravity as interest rates begin to rise. However, as rates continue to rise they ultimately act as a “brake” on economic activity. Think about the all of the economic areas that are NEGATIVELY impacted by rising interest rates:

1) Rising interest rates raise the debt servicing requirements which reduces future productive investment.

2) Rising interest rates will immediately slow the housing market taking that small contribution to the economy away. People buy payments, not houses, and rising rates mean higher payments.

3) An increase in interest rates means higher borrowing costs which leads to lower profit margins for corporations. This will negatively impact corporate earnings and ultimately the financial markets.

4) One of the main arguments of stock bulls over the last 5-years has been the “stocks are cheap based on low interest rates.” When rates rise, the market becomes overvalued very quickly.

5) The massive derivatives and credit markets will be negatively impacted.

6) As rates increase so does the variable rate interest payments on credit cards and home equity lines of credit. With the consumer being impacted by stagnant wages and increased taxes, higher credit payments will lead to a contraction in disposable income and rising defaults.

7) Rising defaults on debt service will negatively impact banks which are still not as well capitalized as most believe, due to the suspension of FASB Rule 157, and are still burdened by large levels of debt.

8) Many corporate share buyback plans and dividend payments have been done through the use of cheap debt, which has led to increased corporate balance sheet leverage. This will end.

9) Corporate capital expenditures are dependent on lower borrowing costs. Higher borrowing costs leads to lower capex.

10) The deficit/GDP ratio will soar as borrowing costs rise sharply. The many forecasts for lower future deficits will crumble as new forecasts begin to propel higher.

I could go on, but you get the idea.

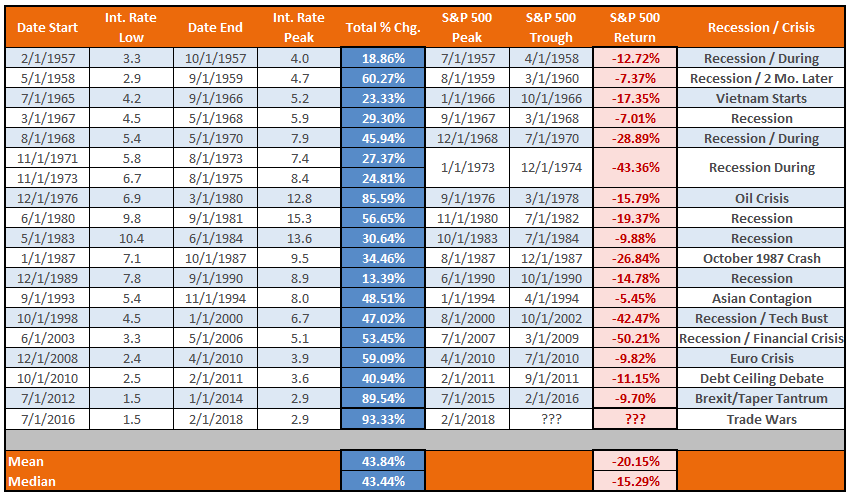

But LPL was addressing the 10-year rate specifically. As I stated, the Fed can push rates in the short-term, but the lifting of rates on the short-end tends to lead to an inverted yield curve. The claim that higher rates lead to higher stock prices falls into the category of “timing is everything.”

In every case, increases in interest rates negatively impact equity prices.

It is just the function of “time” until “something breaks.”

While the analysis from LPL is certainly well intentioned to support the “bullish case,” what it fails to address is the “full-cycle” effect from rate hikes.

LPL is correct that historically interest rate increases have led to higher stock prices. Since troughs in interest rates are typically associated with market bottoms (as money flows from “risk” to “safety,”) the time to BUY equities is when rates begin to rise, not near the end of a rate/economic cycle. The same premise holds true for valuations.

While the mainstream analysis is not to fear rising interest rates in the short-run, as longer-term investors it is crucially important to the preservation of investment capital to understand the dynamics of increasing interest rates and heed the warning being offered by rising rates.

Summary

Here are the things that you need to know:

1) There have been ZERO times when interest rates have risen that did not eventually lead to negative economic and financial market consequences.

2) The median number of months following the initial rate hike has been 17 months. However, given the confluence of central bank interventions, that time frame could extend to the 35-month median or late-2018.

3) The average and median increases in the 10-year rate before negative consequences have occurred has historically been 43%. We are currently at double that level.

4) Importantly, there have been only two times in recent history that the Federal Reserve has increased interest rates from such a low level of annualized economic growth. Both periods ended in recessions.

5) The ENTIRETY of the“bullish” analysis is based on a sustained 34-year period of falling interest rates, inflation and annualized rates of economic growth. With all of these variables near historic lows, we can only really guess at how asset prices, and economic growth, will fair going forward.

6) Rising rates, and valuations, are indeed bullish for stocks when they START rising. Investing at the end of rising cycle has negative outcomes.

What is clear from the analysis is that bad things have tended to follow sustained interest rate increases. While the markets, and economy, may seem to perform okay during the initial phase of the rate hiking campaign, the eventual negative impact leads to losses in investment capital.

Emotional mistakes are 50% of the cause as to why investors consistently underperform the markets over a 20-year cycle. (The other 50% is lack of capital)

For all the reasons currently prognosticated that rising rates won’t affect the “bull market,” such is the equivalent of suggesting “this time is different.”

It isn’t.

Importantly, “This Cycle Will End,” and investors who have failed to learn the lessons of history will once again pay the price for hubris.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter and Linked-In