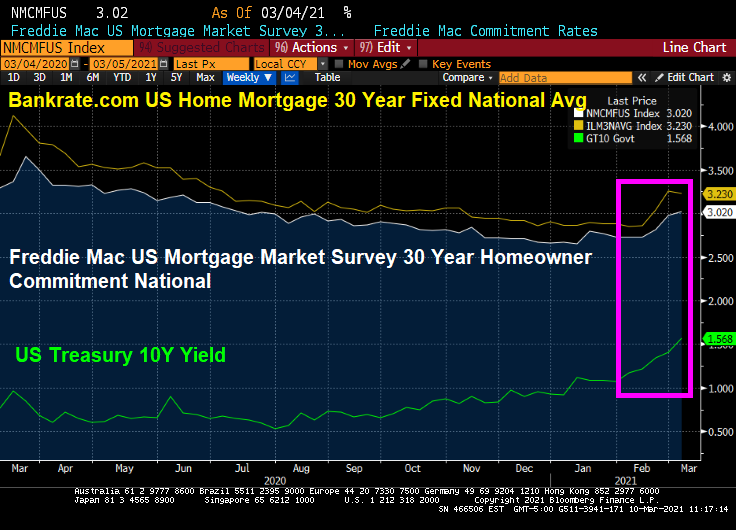

Last week, the average rate for a 30-year fixed mortgage climbed above 3% for the first time since July, according to Freddie Mac. That’s up from the record low of 2.65%, reached in early January.

Even small changes in interest rates can have a big impact for buyers. In a report this week, Redfin Corp. calculated that an increase in mortgage rates to 3.25% from 2.75% would mean that a borrower on a $2,500-a-month housing budget would lose $23,250 in purchasing power.

The rise in mortgage rates is not as disruptive as the lack of available inventory.

Rising mortgage rates and limited available housing inventory is the proverbial “double whammy.”

0 views