Authored by Lance Roberts via RealInvestmentAdvice.com,

With roughly 98% of the S&P 500 having reported earnings, as of mid-June, we can take a closer look at the results through the 1st quarter of the year. During the most recent reported period, 12-month operating earnings per share rose from $33.85 per share in Q4-2017 to $36.43 which translates into a quarterly increase of 7.62%. While operating earnings are widely discussed by analysts and the general media; there are many problems with the way in which these earnings are derived due to one-time charges, inclusion/exclusion of material events, and outright manipulation to “beat earnings.”

Therefore, from a historical valuation perspective, reported earnings are much more relevant in determining market over/undervaluation levels. It is from this perspective the news improved markedly as 12-month reported earnings per share rose from $26.96 in Q4-2017 to $32.81, or a whopping 21.7% in Q1. This jump, of course, is directly related to the reduction in corporate tax rates following the passage of the “tax reform” bill in December of 2017.

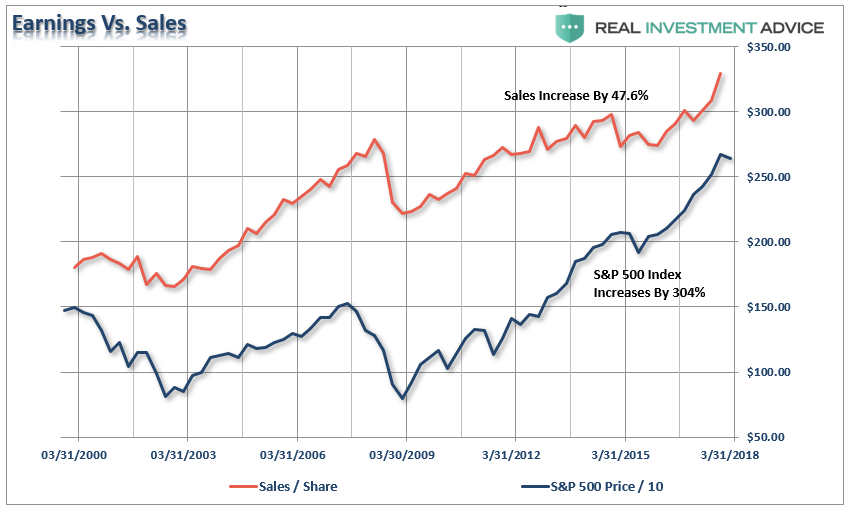

However, as shown below, top-line revenue growth (sales) has also improved since the market bottom in early 2016. The issue is that while sales are indeed rising, the price investors are paying for each dollar of sales has grown exponentially since 2009. In other words, it is already well “priced in.”

Since the media focus on earnings per share (EPS), we see the same issue. Since the end of 2014, investors are paying twice the rate of earnings growth.

No matter how you look at the data, the point remains the same. Investors are currently overpaying today for a stream of future sales and/or earnings which may, or may not, occur in the future. The risk, as always, is disappointment.

Always Optimistic

But optimism is certainly one commodity that Wall Street always has in abundance. When it comes to earnings expectations, estimates are always higher regardless of the trends of economic data. The problem is that the difference between expectations and reality have been quite dramatic.

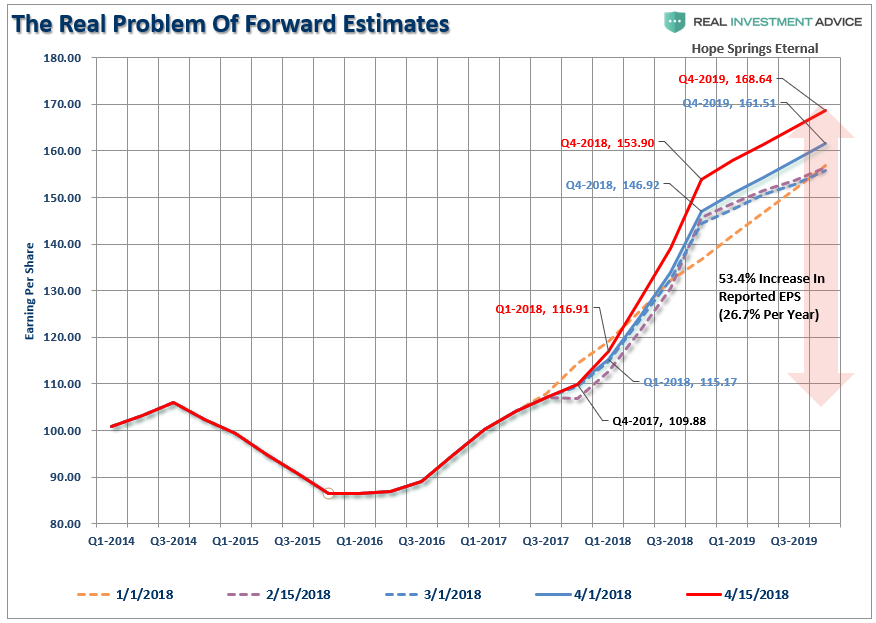

“Despite a recent surge in market volatility, combined with the drop in equity prices, analysts have ‘sharpened their pencils’ and ratcheted UP their estimates for the end of 2018 and 2019. Earnings are NOW expected to grow at 26.7% annually over the next two years.”

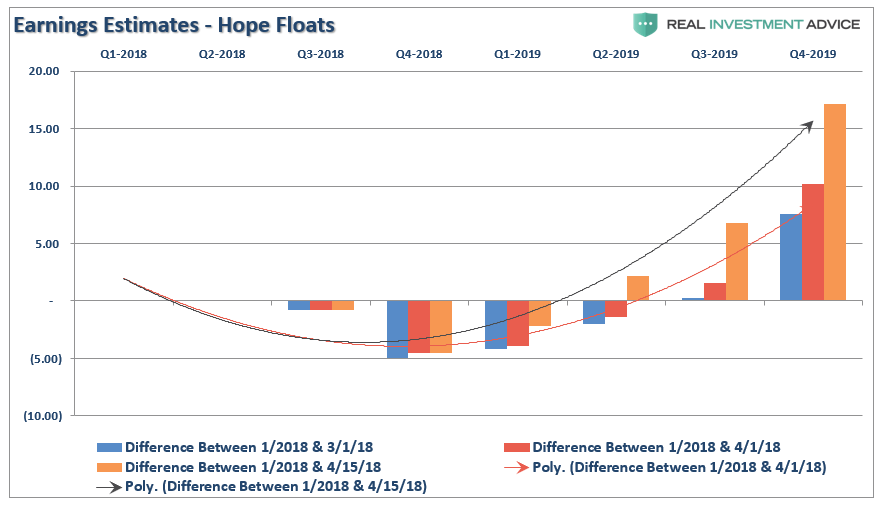

“The chart below shows the changes a bit more clearly. It compares where estimates were on January 1st versus March and April. ‘Optimism’ is, well, ‘exceedingly optimistic’ for the end of 2019.”

That was so a month-and-a-half ago.

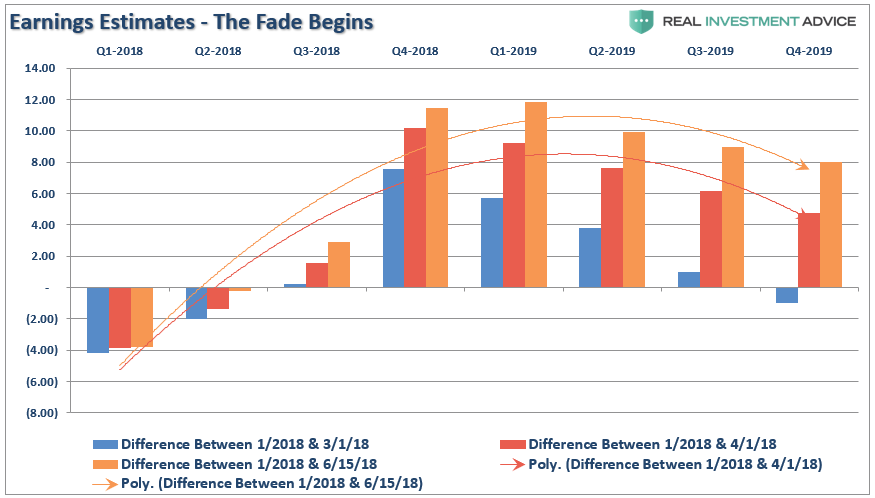

Since then, analysts have gotten a bit of religion about the impact of higher rates, tighter monetary accommodation, and trade wars. As I wrote yesterday, the estimated reported earnings for the S&P 500 have already started to be revised lower (so we can play the “beat the estimate game”). For the end of 2019, forward reported estimates have declined by roughly $6.00 per share.

However, the onset of a “trade war” could reduce earnings growth by 11% which would effectively wipe out all of the benefits from the recent tax reform legislation.

As you can see, the erosion of forward estimates is quite clear and has gained momentum in the last month.

There is no arguing corporate profitability improved in the last quarter as oil prices recovered. The recovery in oil prices specifically helped sectors tied to the commodity such as Energy, Basic Materials, and Industrials. However, such a recovery may be fleeting. There are signs currently that global economic growth is showing signs of weakening. As noted by Adem Tumerkan:

“Taking the contrarian route – it’s not hard to see the market isn’t pricing in any potential global earnings issues. And this is troublesome because the risks keep adding up. The historically accurate South Korean Export Growth Indicator (SKEG) is signaling a looming global earnings recession.”

“[And] for the first time since the 2008 Great Recession, corporate bond yields have inverted.”

“…this inversion signals trouble ahead for the stock market. It means that ‘the cost of capital for corporates is now higher than the return on capital.’ Corporate Bond investors are clearly expecting a recession and deflation ahead – which will cause the prime rate to plunge…this will spill into the stock market and negatively send prices tumbling.”

Accounting Magic

Looking back it is interesting to see that much of the rise in “profitability” since the recessionary lows have come from a variety of cost-cutting measures and accounting gimmicks rather than actual increases in top line revenue. As shown in the chart below, there has been a stunning surge in corporate profitability despite a lack of revenue growth. Since 2009, the reported earnings per share of corporations has increased by a total of 336%. This is the sharpest post-recession rise in reported EPS in history. However, that sharp increase in earnings did not come from revenue which has only increased by a marginal 49% during the same period.

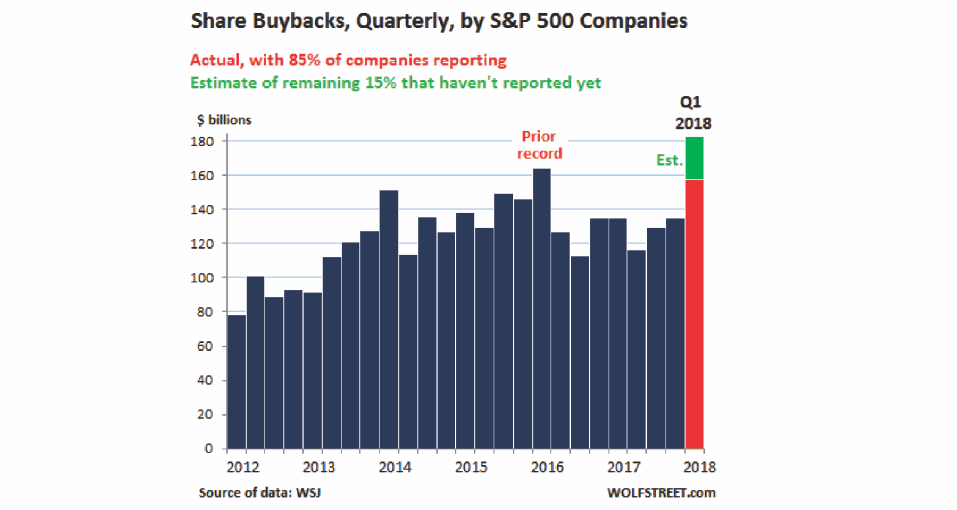

Of course, stock buybacks have been the “go to” method for boosting earnings. According to Greg Haendel from Wealth Management:

“The largest beneficiary of repatriation spending has been the stockholder with the most utilized tool being corporate stock buybacks. Share buybacks increased during Q12018 to a record $178 billion, up from $135 billion a year ago. Further, the 24 U.S. companies with the largest foreign cash holdings accounted for two-thirds of the increase in share buybacks. There has already been $324 billion of buyback announcements year-to-date with an expected total buyback amount of $800 billion for the year. ”

Furthermore, while the majority of buybacks have been done with “repatriated” cash, it just goes to show how much cash has been used to boost earnings rather than expanding production, making productive acquisitions or returning cash to shareholders.

Ultimately, the problem with cost-cutting, wage suppression, labor hoarding and stock buybacks, along with a myriad of accounting gimmicks, is that there is a finite limit to their effectiveness. Eventually, you simply run out of people to fire, costs to cut and the ability to reduce labor costs.

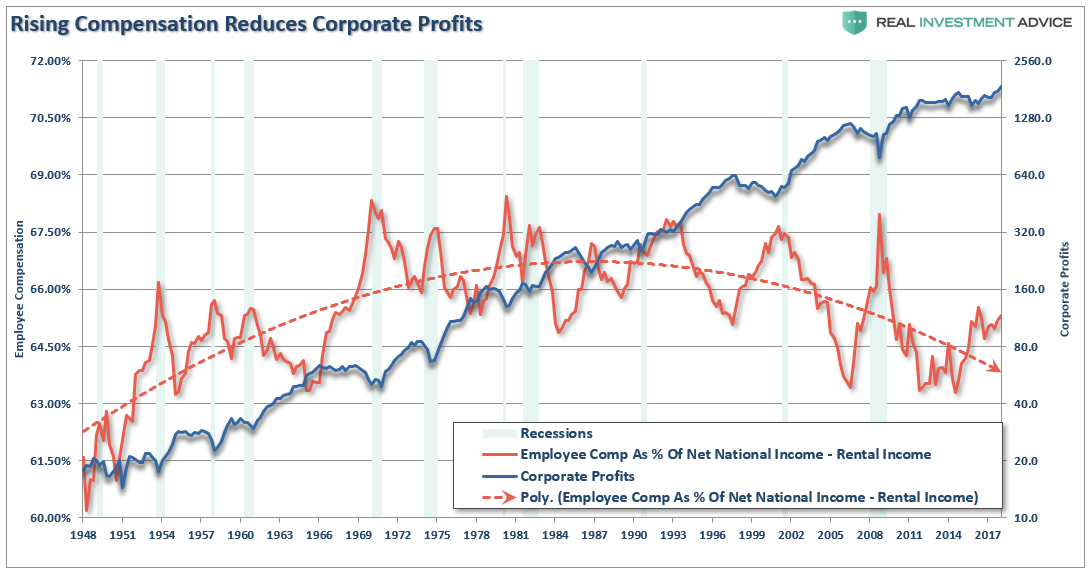

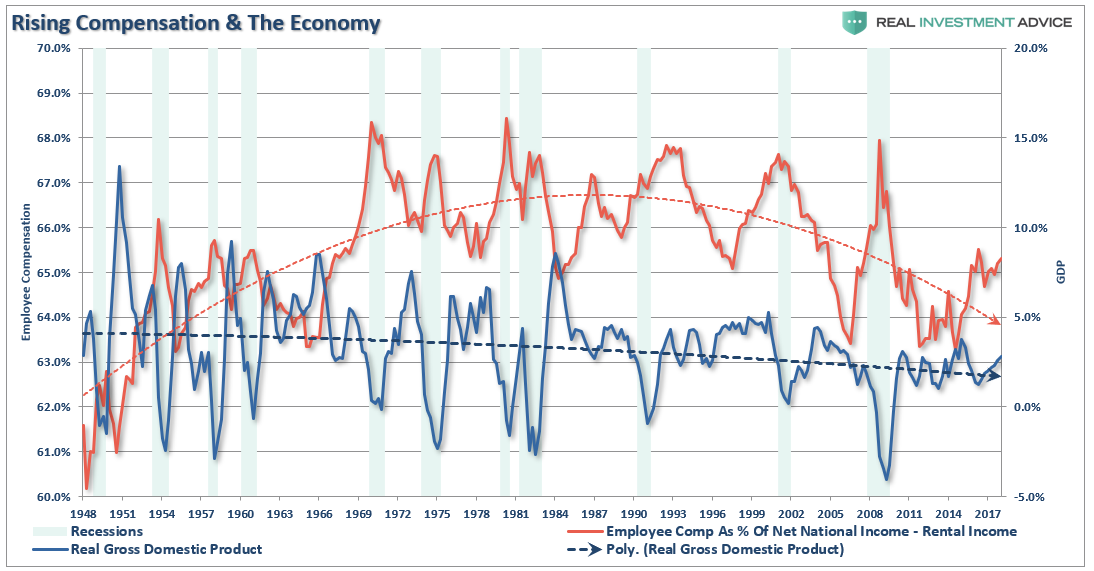

Recently, compensation costs have been rising as the labor market has indeed grown tighter. Of course, this is what is normally seen at the end of economic cycle as rising compensation triggers a profit contraction.

While it would seem that sharply rising employee compensation would be a “good thing,” you will notice that sharply rising employee compensation, which impacts earnings growth, has historically coincided with weaker economic outcomes as higher costs erode profitability.

“It is worth noting that in both charts above, despite hopes of continued economic expansion, both employee compensation, and economic growth have continued to trend to lower since the 1980’s. This declining growth trend has been compensated for by soaring levels of debt to sustain the current standard of living.”

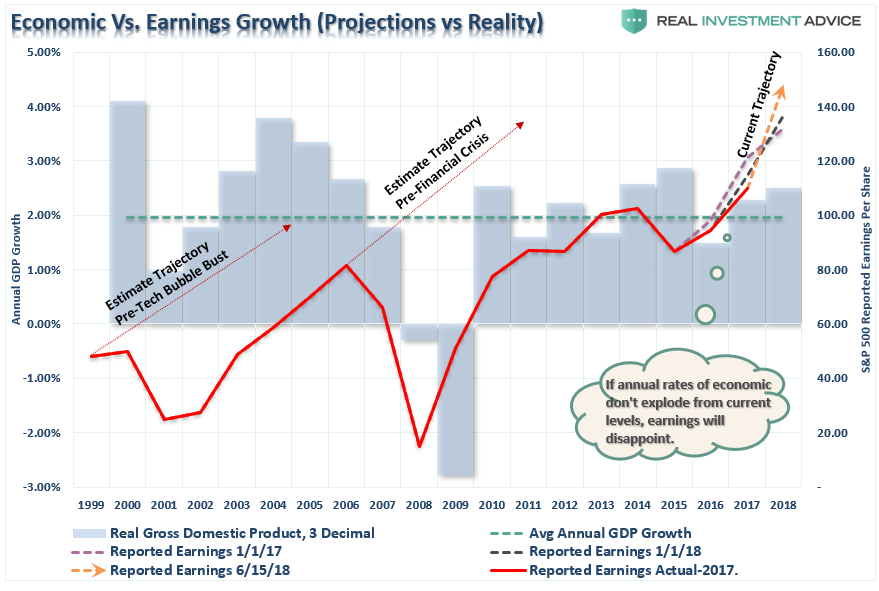

Economics Matter

The last chart below compares economic growth to earnings growth. Wall Street has always extrapolated earnings growth indefinitely into the future without taking into account the effects of the normal economic and business cycles. This was the same in 2000 and in 2007. Unfortunately, the economy neither forgets nor forgives.

With analysts once again hoping for a continued surge in earnings in the months ahead, it is worth noting this has always been the case. Currently, there are few, if any, Wall Street analysts expecting a recession at any point in the future. Unfortunately, it is just a function of time until the recession occurs and earnings fall in tandem.

The deterioration in earnings is something worth watching closely. While earnings have improved in the recent quarter, due to the benefit of tax cuts, it is likely transient given the late stage of the current economic cycle, continued strength in the dollar and potentially weaker commodity prices in the future.

Wall Street is notorious for missing the major turning of the markets and leaving investors scrambling for the exits.

This time will likely be no different.

It is important to remember the bump in earnings growth will only last for one year at which point the analysis will return to more normalized year-over-year comparisons. While anything is certainly possible, the risk of disappointment is extremely high.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter and Linked-In