The S&P 500 and Nasdaq Composite had their highest closings on record Tuesday, regaining ground lost in last year’s rout. Stocks have flourished under a more accommodative Federal Reserve. In January, the central bank said it would hold interest rates steady, setting in motion the stock market’s strongest first-quarter run in more than two decades, as investors dialed back up their appetite for riskier assets like stocks.

On Tuesday, the stock market hit all-time highs.

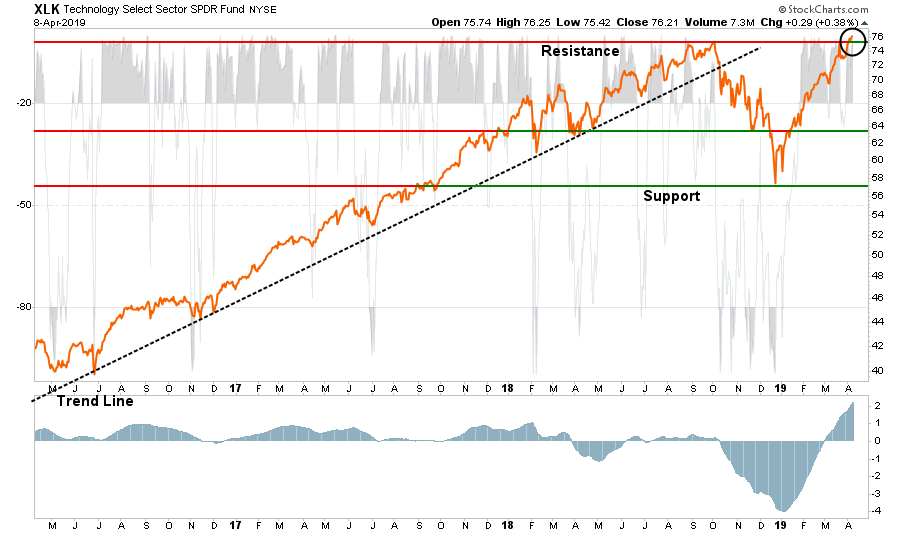

Such should not be surprising given the rally particularly in the very heavily weighted Technology sector (XLK) and something I penned several weeks ago for our RIA PRO subscribers: (Get a 30-day FREE trial)

Currently XLK is on a “Buy” signal (bottom panel) but that signal is “crazy” extended.

However, the good news is that four sectors have broken out to all-time highs and technology is one of them. This is suggesting the overall market will break out to new highs as well.

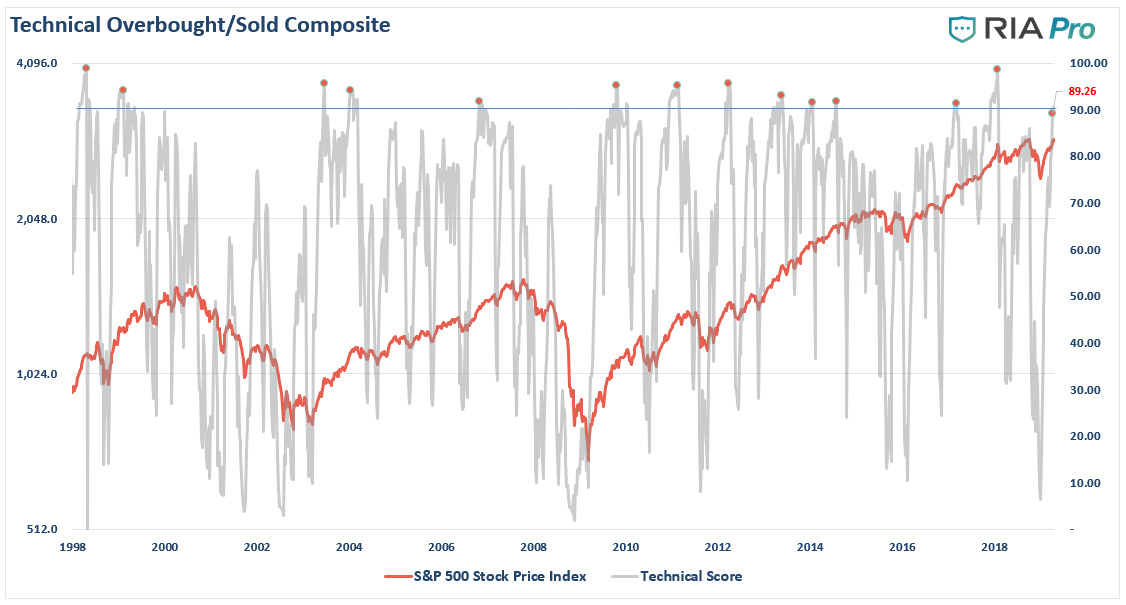

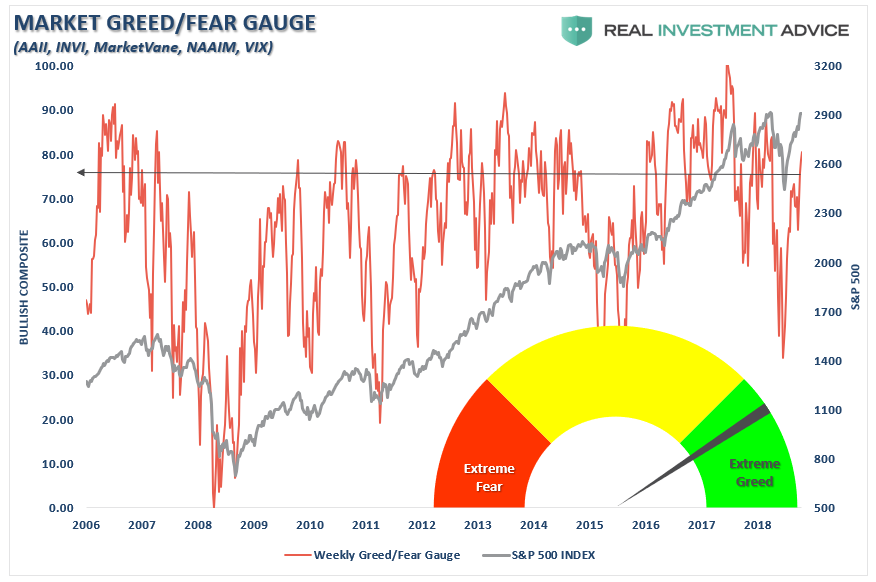

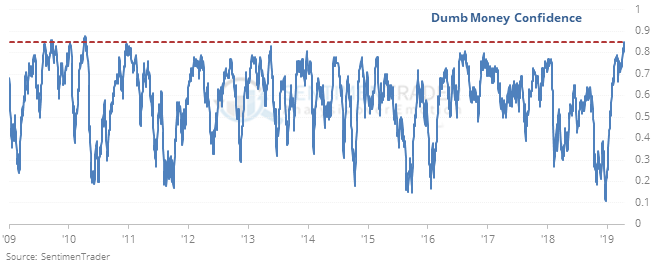

Of course, the rise in the market since the December lows has quickly “replaced” the panic felt then with an unbridled optimism currently. As I showed this past weekend in “F.O.M.O.- The Fear Of Missing Out” and in our RIA PRO Weekly Technical Market Gauge, the bulls are back.

It isn’t just our technical gauge which suggests investors have returned to their bullish ways. The RIA PRO asset allocation composite suggests the same.

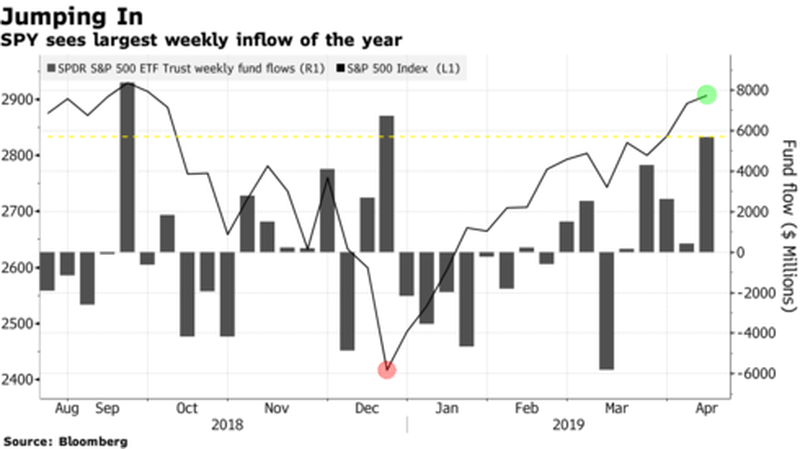

As well as numerous other data points showing investors jumping back into equities with both feet as markets approach all-time highs.

A recent survey from Ally Invest showed much the same:

“The bullish sentiment by investors, which doubled between Q1 and Q2 of this year, appears, in part, supported by the majority of respondents’ belief that interest rates will remain unchanged this year (67%) and the government will sign economic trade agreements that will help drive the markets higher (61%).

Other major market drivers cited by respondents include positive year-over-year earnings (26%), low unemployment rate (24%), lack of inflation (18%), and tax reform (15%).”

E*Trade also recently released survey data showing:

- Bullish sentiment returns. Bullishness rose 12 percentage points since last quarter to once again represent the majority of investors at 58 percent.

- Investors believe there’s more room for the bull market to run. Two-thirds of investors say they think the bull market has a year or more to go (66%), up seven percentage points from last quarter.

- The majority gave the US economy a passing grade. Investors who gave the economy an “A” or “B” grade rose 9 percentage points this quarter, to 64%.

- Volatility concerns remain. Investors who believe volatility will stay the same was up by 8 percentage points from Q1.

You get the idea. Just 8-weeks after panic selling lows, investors are once again “back in the pool.”

Willful Blindness

Willful blindness, also known as willful ignorance or contrived ignorance, is a term used in law to describe a situation in which a person seeks to avoid civil or criminal liability for a wrongful act by keeping themselves unaware of the facts that would render them liable or implicated.

Although the term was originally used in legal contexts, the phrase “willful blindness” has come to mean any situation in which people intentionally turn their attention away from the facts to avoid the liability of their actions.

In the financial markets, this is most prevalent. Investors regularly dismiss the “facts” which run contrary to their current opinion. As markets are rising, they take on excessive risk with the full knowledge that such actions will have a negative consequence. When that negative consequence eventually occurs, they blame the media, Wall Street, their advisor, and anyone else they can find for their losses.

This currently where we are in the markets today.

Investors know there is a rising risk of loss, but, they are willfully ignoring the facts and and piling into risk because the narrative has simply become “fundamentals don’t matter, the Federal Reserve has got your back.”

After all, CNBC said so.

This is a dangerous assumption given that buoying stock prices are not part of the Federal Reserve’s mandate.Congress set dual goals of stable prices and maximum sustainable employment. The central bank’s preferred inflation gauge registered at 1.8% in January, just below its 2% target and the unemployment rate in March was 3.8%, below the 4.3% the Fed estimates is sustainable. Further, wage pressures are rising which will put pressure on the Federal Reserve to raise rates.

However, as I penned previously, investors currently are under the impression the Federal Reserve will not hike rates further and, more importantly, will quickly initiate QE if the market begins to weaken.

This is likely a misplaced belief.

Cleveland Fed President Loretta Mester:

“Could we be done with policy rate increases this cycle? It is possible, but if the economy performs along the lines I think is the most likely case…the fed-funds rate may need to move a bit higher than current levels.”

Philadelphia Fed President Patrick Harker:

“I continue to be in ‘wait-and-see mode‘ with expectations of at most, one hike for 2019 and one for 2020.”

Those comments don’t align with a Fed eager to sit on the sidelines, reduce rates, or begin to inject further stimulus. Furthermore, Fed officials think the economy is in a good place with low unemployment and benign inflation. If they sense a slowdown, Fed officials would first act by trimming their benchmark interest rate.

Then, there is the question of its effectiveness anyway.

What investors should realize is that markets will be in a deep bear market, and recession, before QE would be restarted. However, that appears to be a point lost on market participants currently.

Furthermore, investors have become “willfully blind” to a few salient points.

- The Fed isn’t hiking rates, but they aren’t reducing them either.

- The Fed isn’t reducing their balance sheet any more after September, but they aren’t increasing it either.

- Economic growth outside of China remains weak

- Employment growth is slowing.

- There is no massive disaster currently to spur a surge in government spending and reconstruction.

- There isn’t another stimulus package like tax cuts to fuel a boost in corporate earnings

- With the deficit already pushing $1 Trillion, there will only be an incremental boost from additional deficit spending this year.

- Unfortunately, it is also just a function of time until a recession occurs.

Of course, the Fed isn’t the only thing behind the market’s recovery.

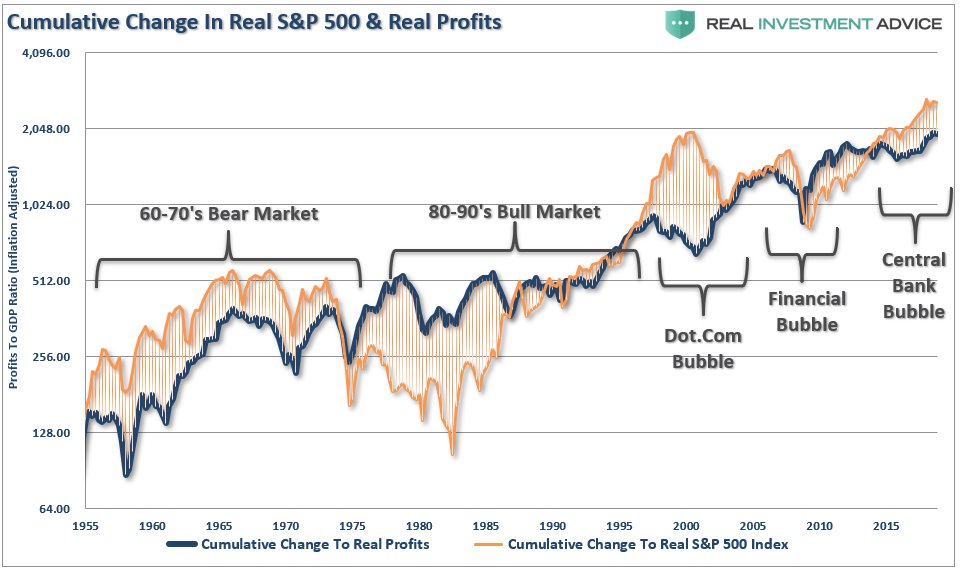

About Those Soaring Profits

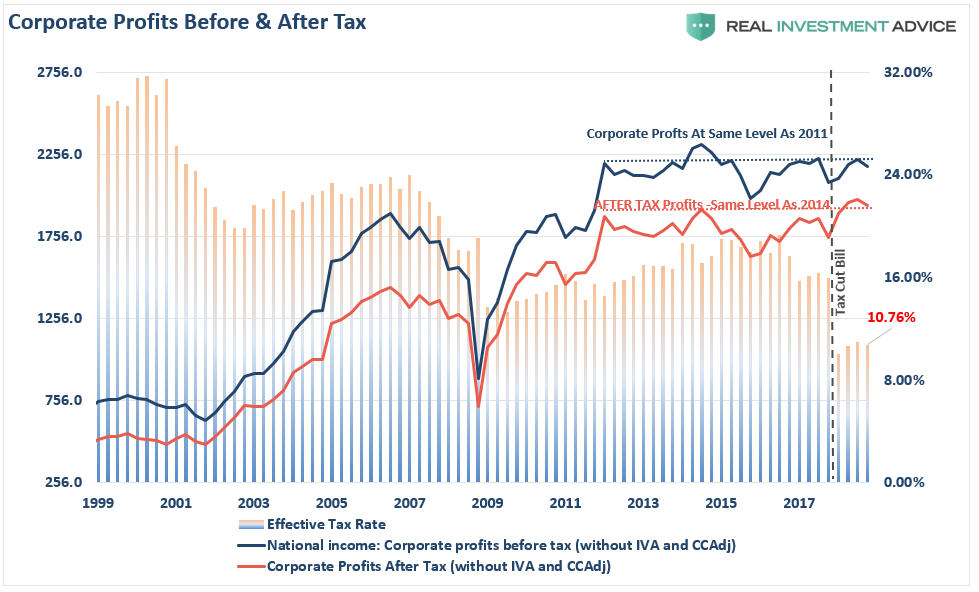

As noted by the WSJ recently noted, U.S. corporate profits have surged which have been the support for surging asset prices.

The important thing about looking at corporate profits, rather than earnings, is that this is what is reported to the Internal Revenue Service for taxation purposes. It also strips out all of the accounting gimmickry found in operating earnings, excessive share buybacks, and other obscuring factors.

While stock prices have surged to all-time highs, corporate profits remain at the same level as they were in 2011 on a pre-tax basis, and 2014 on a post tax basis.

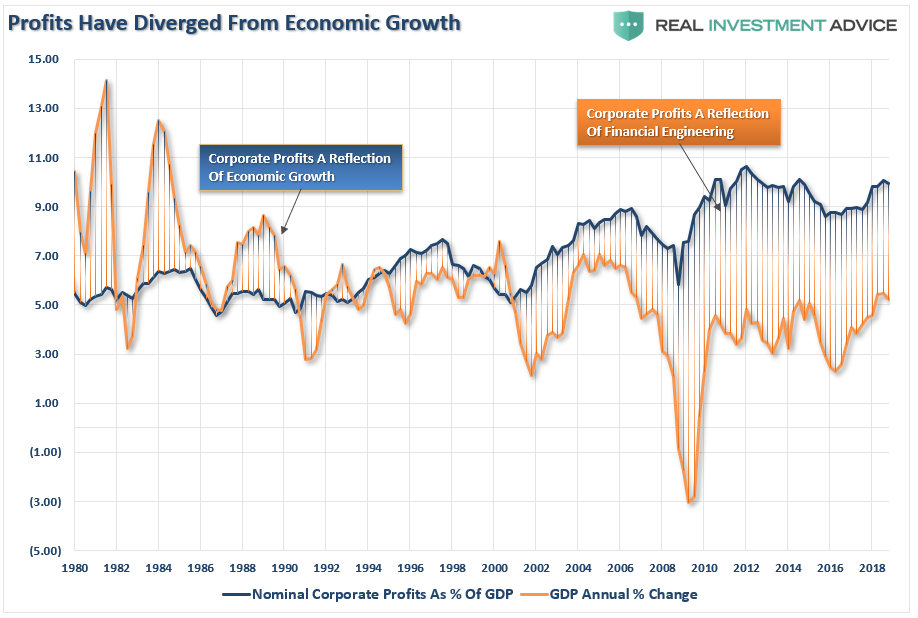

While the WSJ is correct that corporate profits now 10% of GDP, up from 6-8% prior to the turn of the century, there are two factors worth noting.

- Corporate profits are very diverged from economic growth which is contributing to the wealth inequality issue.

- The profit/GDP ratio is still lower than it was in 2010-2011 despite the massive boost from tax cuts, $1 trillion in deficit spending, and a booming stock market.

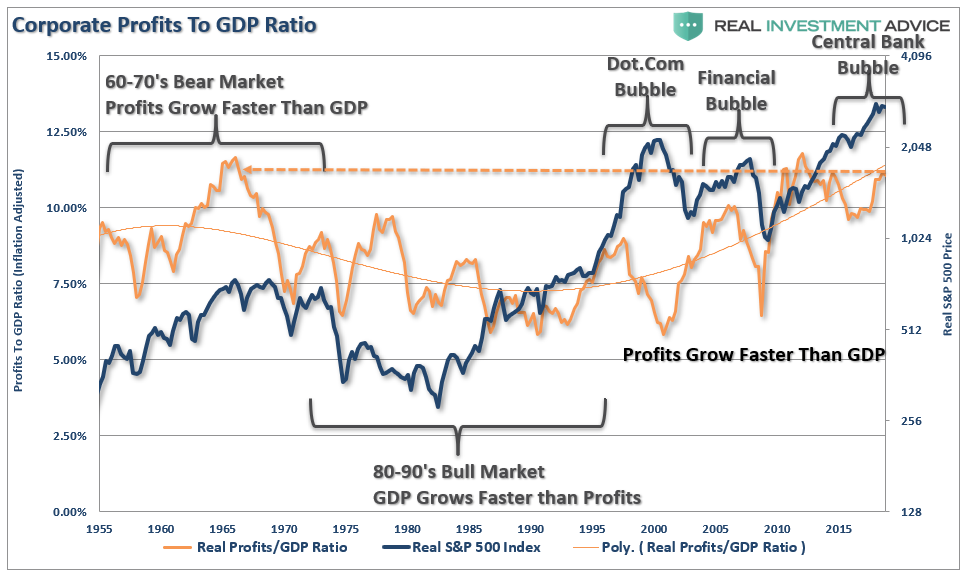

Looking at this a little differently, we can better understand what is occurring. In the 60-70’s, leading up to the “Black Bear Market of 1974,” corporate profits were growing faster than GDP. This is ultimately an unsustainable trend as profits are a function of economic growth and not the reverse. The 80-90’s bull market was a period of economic growth outstripping profit growth as interest rates and inflation fell. Beginning at the turn of the century, and now three asset bubbles later, profits are again growing faster than the economy.

The same can be seen in the cumulative change in asset prices versus profits. When price inflation exceeds profit growth, that deviation has not historically lasted very long.

Economic Hopes To Be Disappointed

“But…the global slowdown is temporary.”

The expectation of an economic recovery to support the continuation of the bull market is likely misplaced for several reasons.

- The Fed rate hikes that were done in 2018 are still working their way through the economy, Higher rates are impacting economically sensitive sectors like autos, housing, and manufacturing.

- Economic growth globally remains weak and is impacting growth in the U.S.

- Interest rates, and the yield curve, despite stocks hitting “all-time” highs are suggesting that economic weakness is likely more pervasive than currently believed.

- The rising trend of the U.S. dollar will impact exports which makes up between 40-50% corporate profits.

- Imports continue to suggest the U.S. consumer, 70% of the economy, is weaker than headlines suggest.

- Rising oil prices, and gasoline prices, are a tax on consumers and will further impair economic growth.

- Deflation is a rising concern.

- There is no massive slate of natural disasters to pull forward consumption or boost manufacturing, construction or commodity demand.

- While deficit spending is certainly supportive of growth, with the deficit already at $1.2 trillion, the rate of change in deficit spending will not be supportive of stronger economic growth.

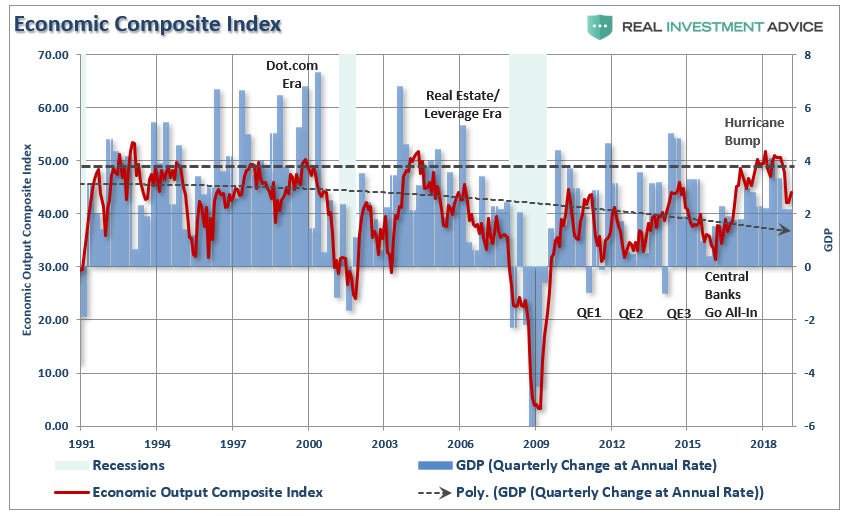

The RIA economic composite index (a broad composite of hard, soft, and leading indicators and surveys) has turned lower. Historically, turns from high levels (dashed black line) tend to revert to the lower bound suggesting more economic weakness is likely in the quarters ahead.

That reversion would also align with the recent CFO survey which generated responses from more than 1,500 chief financial officers, including 469 from North America, and showed:

- 67% of those surveyed predicted the U.S. economy would be in recession by the third quarter of 2020,

- 84% believe a recession will have begun by the first quarter of 2021.

- 38% of respondents predicted a recession by the first quarter of next year.

While CFOs are not as pessimistic as they were three months ago, it is unusual in the history of the survey for such a large share of respondents to predict a recession just 16 months from now.

The Problem Of Eternal Bullishness

With the current economic cycle already long by historical standards, economic data continuing to remain weak, and profit margins on the decline, there is an increasing possibility that “risk” may well outweigh “reward” at this juncture.

Such doesn’t mean that stocks can’t go higher in the near term, and despite some wiggles along the way, it is quite likely they will simply because of momentum and lot’s of “bullish bias.”

However, the problem of “eternal bullishness” is that it leads to the “willful blindness” of risks, rather than having a healthy respect for, and recognition of, those risks. This leads to the unfortunate problem of being “all-in” on every hand which has a devastating consequence when a mean reverting event occurs.

John Hussman once penned an excellent piece on the full-market cycle:

“Regardless of very short-term market direction, it is urgent for investors to understand where the equity markets are positioned in the context of the full market cycle. While the most extreme overvalued, overbought, overbullish, rising-yield syndrome we define has generally appeared only at the most wicked market peaks in history, and investors have ignored those conditions over the past year. We can’t be certain when the deferred consequences will emerge. But a century of market history provides strong reason to believe that any intervening gains will be wiped out in spades.

It’s instructive that the 2000-2002 decline wiped out the entire total return of the S&P 500 – in excess of Treasury bills – all the way back to May 1996, while the 2007-2009 decline wiped out the entire excess return of the S&P 500 all the way back to June 1995. Overconfidence and overvaluation always extract a terrible payback.”

In the end, it does not matter IF you are “bullish” or “bearish.” The reality is that both “bulls” and “bears” are owned by the “broken clock” syndrome during the full-market cycle. However, what is grossly important in achieving long-term investment success is not necessarily being “right” during the first half of the cycle, but by not being “wrong”during the second half.