Exuberant stock market, disappearing middle class, history repeats itself [ A 32-year-old mother of 7 children called Florence Owens Thompson, Nipomo, California. February 1936.]

One in five American households have ‘zero or negative’ wealth

U.S. homes have regained value since the Great Recession, but many households have not

Millions of Americans are living on the edge.

One in five households has zero or negative wealth, according to a report released this week by the Institute for Policy Studies, a progressive think tank based in Washington, D.C. What’s more, an even greater share of African-American (30%) and Latino (27%) households are “underwater” financially. The combined impact of $1 trillion in credit-card debt, $1.4 trillion in student loan debt, and stagnant wages are taking a toll.

U.S. homes have regained value since the Great Recession, but many households have not. “Millions of American families struggle with zero or negative wealth, meaning they owe more than they own,” the report found. “This means that they have nothing to fall back on if an unexpected expense comes up like a broken down car or illness.” And inequality could get worse through new tax cuts for the wealthy.

Why are Americans drowning in credit card debt?

When used responsibly, credit cards are a useful addition to your wallet. They’re not only safer than cash, they also can build your credit rating. And some cards include rewards programs, helping you save money on future purchases.

But with the accessibility of credit, there also are the risks of overuse and debt. So many people have fallen into the credit card trap, Americans owe a collective $1 trillion in credit card debt, according to the Federal Reserve. And, a recent GOBankingRates survey found respondents have nearly $7,000 in credit card debt, on average.

Among the major reasons people are piling on more credit card debt:

Splurging on a wedding: A fairy-tale wedding can create a memorable day for couples and their guests. But some couples go overboard and end up spending more than they can afford on a wedding. The average cost of a wedding in the U.S. has skyrocketed to a new high of $35,329, according to The Knot 2016 Real Weddings Study.

“Putting most of your wedding expenses on a credit card is a bad idea, and what may not seem like much starts to add up very quickly and soon becomes overwhelming,” said Ogechi Igbokwe, a certified financial educator and founder of OneSavvyDollar, a website that helps students manage their personal finances. “It’s dangerous to start a wedding on credit because it shows you’re not planning adequately as a couple.”

Rather than feel the pressure to throw an impressive wedding, be realistic about what you can afford as a couple, create a budget and then stick with this budget.

“The wedding doesn’t have to be elaborate as long as both parties are present with their loved ones,” Igbokwe said.

Spending more to earn rewards: Credit card rewards programs are attractive and allow you to earn points, miles or cash back on every dollar spent. But the earning potential of a rewards program can also translate into more debt.

“Americans are battling more credit card debt because they are making more purchases with their cards,” said Alayna Pehrson, a digital marketing strategist at Best Company, a review website that ranks thousands of companies, including credit cards. “Many Americans reap rewards from using their credit cards, which encourages them to use the cards more frequently.”

Chart of the Day: Here’s Your Report Card, Janet—America’s Workers Say Good Riddance!

— Alastair (@StockBoardAsset) December 9, 2017

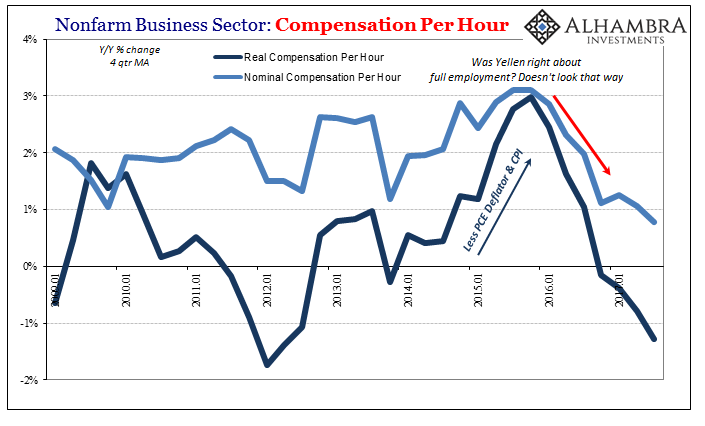

The economy’s biggest mystery — paychecks just aren’t growing

Wage numbers disappoint despite strong job growth from CNBC.

-

Friday’s nonfarm payrolls report showed solid job growth of 228,000 for November but a mediocre 2.5 percent annualized gain in average hourly earnings.

-

Economists believed heading into 2017 that the low unemployment rate would push wages higher, but they still haven’t broken out.

-

White House economic advisor Gary Cohn told CNBC that the administration is optimistic that wages will move considerably higher in the year ahead.

Despite a mostly solid run of job growth, 2017 ends pretty much where it began — with a two-speed economy where wage growth is funneling to one end while the other lags behind.

Friday’s nonfarm payrolls report brought with it news all too familiar to the post-crisis economy. The 228,000 jobs created formed a solid foundation, but the pedestrian 2.5 percent average hourly earnings growth left many scratching their heads wondering how a 4.1 percent unemployment rate, the lowest in 17 years, still wasn’t producing fatter paychecks.

“The lack of wage growth at the aggregate level despite the declines in the unemployment rate and strong job gains remains a mystery,” Joseph Song, U.S. economist at Bank of America Merrill Lynch, said in a note to clients.

“Splurging on a wedding: A fairy-tale wedding can create

a memorable day for couples and their guests. But some couples go

overboard and end up spending more than they can afford on a wedding.”

You should never get married, esp. in the west, if you’re a man; but if a woman wants something like this (and she’s not rich and paying for it herself), she’s not wifey material.

AND STILL NO civil WAR or revolution, WHY NOT?

easy answer is CONTROL total control, since and some before 911 the USA is RUN by ZIONIST JEWS the exact same ones that DID 911 for G.Bush, we LET them GO!

They run the USA TOP DOWN and will NEVER GO peacefully.

David A. Steinberg just bought Disqus!!!! WATCH who is the moderator NOW!!! https://uploads.disquscdn.com/images/921ead0c68f8fb046cc464c7c03f462d2ba3736439b1d12b091486fc2d4068f1.jpg

“Housing values going up” Bullshit – the zionist scum who STOLE over 15 million homes since 2008 in the last engineered “collapse” have transfered over 7 miilion homes to the scumbag zionist fed. The elevation is prices is a real as the fraudulent zionist run stock market. Only a revolution will fix the probelm, this time: permanently.

Just so long as ISRAEL gets American TAXES that is all that counts —-

Now -I- want to see Trump’s tax returns ….. After bragging he was too rich to be bribed and funding his own campaign ….. he is “INDEBTED” to filthy Sheldon Adelson?!!!!

I have lost all respect and have no use for P.O.S. Trump he is a retard who got through life by bullying everyone …. Not only that, Mister “Art of the Deal” who claims every other treaty we have is a “rotten deal” …. What did Mr. Negotiator GET for groveling to his Owners? Will Adelson order all the Jewish politicians that have been blocking the Wall and forcing Invaders onto Us to STOP?!? Will America finally cut off the $5+BILLION WELFARE CHECKS ? Israel has been collecting WELFARE from America for SEVEN DECADES, did Drumpf stop that !?

I believe Trump will spin on a dime and betray every promise about Guns and immigration ……

Trump betrayed America AND Christ in Jerusalem, and is betraying the Middle Class with FAKE tax cuts … https://www.bloomberg.com/news/articles/2017-12-07/trump-s-middle-class-tax-pledges-go-unfulfilled-in-senate-bill How long before Trump betrays America for the Jewish Kalgeri Plan https://www.youtube.com/watch?v=0NE2rCKKtOc https://www.youtube.com/watch?v=8rBr62XQUSA and flings open Our borders.

http://www.redressonline.com/2017/08/no-time-for-shallow-diplomacy-christians-in-the-religious-war-on-churches-in-the-holy-land/

Where are the HOLOMODOR memorials ??!! http://www.rense.com/general85/holodo.htm

We probably should have moved Washington D.C. to Jerusalem as this is where our foreign policy will come from in the Hebrew dominated nation that Amerika has become. http://www.corbettreport.com/ anyone who does not see it now is mindbogglingly stupid (i.e. Zion-Evangelists) or a Crypto-Jews like Trump. https://www.strategic-culture.org/news/2017/12/04/mueller-names-trump-foreign-colluding-power-israel.html

America needs another Independence Day – independence from Israel.

Trump is too busy making ISRAEL FIRST to build that wall …..

FAKE —- Trump is a FAKE president —– Trump’s Biggest Owner/Donor Sheldon Adelson Pushed For Jerusalem Embassy Move https://www.globalresearch.ca/trumps-biggest-donor-pushed-for-jerusalem-embassy-move/5621657 ahhhhhhhh what happened to Trump “Too rich to be bribed and funding HIS OWN campaign”?????? Bought and PAID FOR …………..

Get some FACTS straight …. the DOW, NASDAQ, & S&P are hitting all time highs. Unemployment is supposed to be at all time LOWS. We are supposedly having a glorious upsurge in the economy, If we do not pay off the debt NOW when will we? All this glorious economic news and we still have DEFICITS?! Why do you have to “cut taxes for the already rich” so they will supposedly be inspired to create more jobs …… when everybody is supposedly employed???!! And the true job creation is proven to be by Small Business and financed by Middle Class spending, NOT by millionaires.

We should be raising taxes. If these Billionaires had to pay a proportionate amount equal to the benefit they derive from Us protecting Their money, property, LIVES …….. they would take an interest in getting a GOOD government not just one that serves their immediate interests …. They would insist on ending corruption and waste and balancing the books. People whine there is no such thing as “fair” taxes ,,,,, but there is . The Workers pay with blood & money for ONE house with a mortgage to the BANKSTERS ….. counting all they pay for state, local, sales, federal taxes 1/3 of their gross. The Billionaires whine they need tax cuts “to create jobs” and NEVER SERVE in uniform so they never get PTSD, amputations, maimed or die.

TAKE 60% of their gross because they own multiple homes with NO mortgages.

It is past time these Billionaires & mega-corporations PAY for the wars from which they profit and which protect them. Either PAY for the wars, or we put your Boards of Directors in the Front Lines to BLEED with us working stiffs. You want to move your corporation, OUR JOBS, to another country to dodge taxes here? So WE have to pay for your wars? Over YOUR DEAD BODIES. The U.S. has intervened militarily and covertly in so many nations it is impossible to recount them all but in every case the American military is protecting some investments of value to American corporations, or a strategic position or both.

Those who benefit the most should contribute a proportionate share.

Amazing that all these leftwing tech billionaires do not want to share THEIR wealth. They always talk left wing “communalism” but they clutch their money like it is life itself ….Even when they “give” charity it is through THEIR trusts &foundations that THEY control and reapTAX BENEFITS FROM. Even though They are always eager to spread YOUR money around……

Time for the 1% to contribute PROPORTIONALLY to the War Efforts. Much is expected from those to whom much is given.

Some of our Troops give ALL, or are maimed for life,and the 1% balks at giving MONEY when they have so much?!

Cut taxes for the “Rich” so they will invest their money in creating more jobs? By that logic giving ALL your money to the Rich would make Everyone rich. Humanity already tried that. It was called FEUDALISM, a primitive form of COMMUNISM.

LISTEN to what these neocon PSEUDO-capitalists are saying:

“TAKE from the POOR and GIVE to the RICH”

“FROM each according to their ABILITY, TO each according to their NEED. The POOR have the ABILITY to be squeezed for more taxes …….. and the Rich NEED more money …… to create jobs”???????.

This is INSANITY, this is C-O-M-M-U-N-I-S-M by a different name.

MAKE ZUCKerberg and these other Billionaires want to flood the labor pool and drive down YOUR wages with cheap illegals & invaders ….. . As it is, YOU pay to bring in and train YOUR replacements.

The rich “Nobles” paid NO taxes and they created LOTS of jobs for the SERFS and PEASANTS………building CASTLES and making life better for the RICH-NOBILITY. Work and Taxes was all the Serfs knew. Where do the heroic figures of Robin Hood and William Tell spring from if not resistance to this inane idea? Seing this extremist idea dragged out of the muck of history proves to me that our Nation has truly been DUMBED DOWN and Public Schools need to be upgraded and intensified.

Quit living in Never-Never Land where Wars are not paid for. The Founding Fathers of America didn’t. The Founding Fathers were rich, but they knew it was their CIVIC DUTY to contribute. It was called LEADERSHIP. They personally “raised” entire companies of men for the war. That means THEY PAID FOR THEM. Not like today when the YELLOW-BELLIED-DRAFT-DODGING Neocan WAR PROFITEERS beat the drums for endless war, and insist that YOU pay for it, while they reap profit off Defense Stocks. It is REALITY CHECK time America. Make those who pound the War Drums, GO TO THE WAR.

This really should not come has a surprise, it’s not like Americans haven’t been warned countless upon countless of time in the past 10 years