Tapered QE-4 Further, Still Hasn’t Bought Junk Bonds or ETFs, Was Just Jawboning.

By Wolf Richter for WOLF STREET.

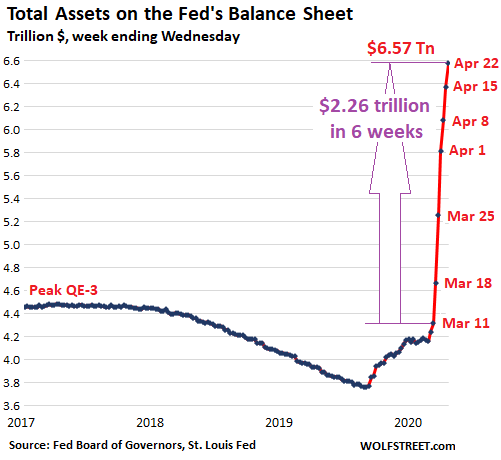

Total assets on the Fed’s balance sheet rose by $205 billion during the week ending April 22, to $6.57 trillion. Since the week ending March 11, when the bailout of the Everything Bubble and its holders began, the Fed has printed $2.26 trillion.

But the $205 billion increase was the smallest increase since the mega-bailout began with its Sunday March 15 announcement. The Fed is tapering its purchases of Treasury securities and mortgage-backed securities (MBS). Repurchase agreements (repos) are falling into disuse. Lending to Special Purposes Vehicles (SPVs) has leveled off. And foreign central bank liquidity swaps, after having spiked initially, only ticked up by a small-ish amount.

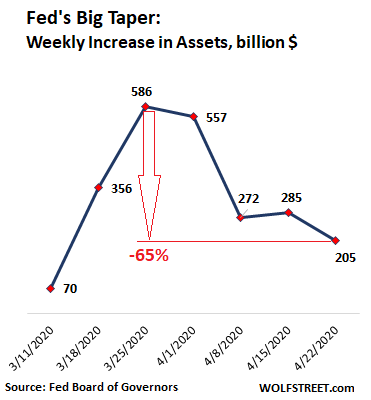

The sharply reduced increases confirm that the Fed is following its various announcements over the past two years that during the next crisis – namely now – it would front-load the bailout QE and after the initial blast would then taper it out of existence, rather than let it drag out for years.

This concept was further confirmed by Fed Chair Jerome Powell in on April 10 when he said that the Fed would pack away its emergency tools when “private markets and institutions are once again able to perform their vital functions of channeling credit and supporting economic growth.”

Overall, the Fed has cut the big QE purchases by 65% since the peak week (week ending April 1, $586 billion), to $205 billion:

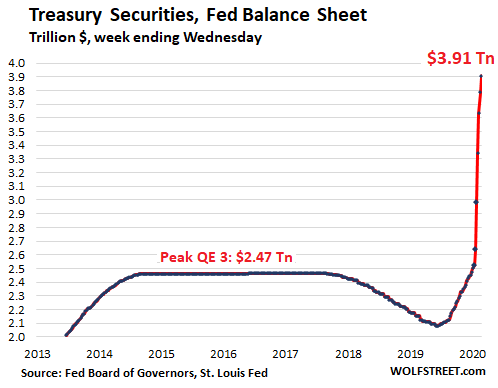

Purchases of Treasury securities get slashed.

The Fed added $120 billion of Treasury securities to its balance sheet, the smallest amount since this began, down 67% from the $362 billion it had added during the peak week:

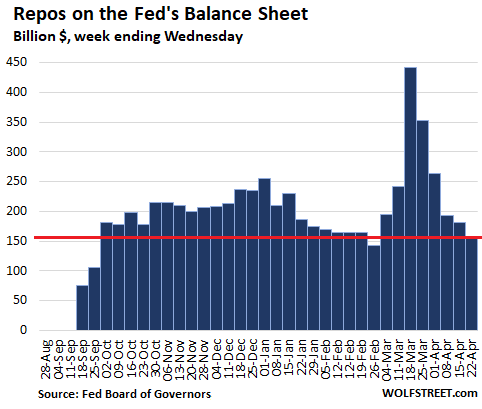

Repos balances continue to decline.

Demand for repos has abated. Recently, there have only been a few nibbles. What is left of the repos stems from prior term repos that will fall off the balance sheet when they mature. Total repo balances fell to $157 million, down 64% from the peak ($442 billion):

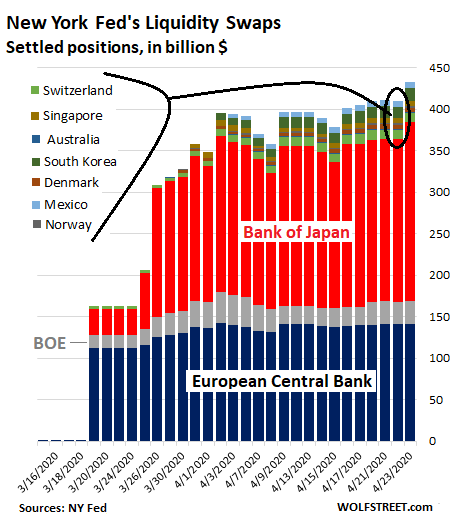

Central Bank Liquidity Swaps.

The Fed has “dollar liquidity swap lines” with the Bank of Japan, the ECB, and the central banks of England, Canada, Australia, New Zealand, Sweden, Denmark, Norway, Switzerland, Singapore, South Korea, Brazil, and Mexico. The combined amount of those swaps increased by $31 billion from the prior week to $410 billion. Some highlights:

- The Bank of Japan is the largest counterparty with $195 billion in liquidity swaps, or 48% of the total.

- The ECB, with $142 billion in swaps, accounts for 32% of the total.

- The Bank of England is in third place, with $27 billion.

- No swaps with the central banks of Canada, Brazil, New Zealand, and Sweden.

The balance sheet is for the week ended Wednesday April 22. The chart, which depicts the most current daily balances released by the New York Fed, also includes Thursday (right column):

With a swap, the Fed lends newly created dollars to a central bank, which posts newly created domestic currency at the Fed as collateral. The exchange rate is the market rate at the time of the contract. The swaps come with two types of maturities: 7 days or 84 days. When the swaps mature, the Fed collects its dollars, and the other central bank collects its own currency. The Fed books these swaps on its balance sheet in dollars, at the exchange rate in the agreement.

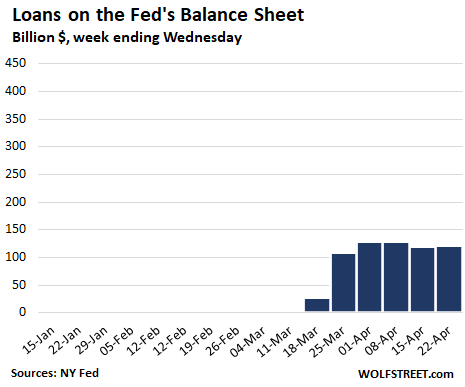

“Loans” to SPVs & Primary Dealers level off.

The line item on the balance sheet labeled “Loans” represents the Fed’s loans to Special Purpose Vehicles (SPVs) it set up, and to its Primary Dealers (the big broker-dealers and banks the Fed does business with). By using SPVs, the Fed can buy whatever it chooses to, because legally, it just lends to the SPV, a separate legal entity that then can use this money to buy whatever the Fed wants it to buy, or to re-lend the money against whatever collateral the Fed deems acceptable. Congress, which could stop these schemes, applauds them.

When the Fed first announced its alphabet soup of bailout programs, the “loans” ballooned. But over the past four weeks since then, they have remained essentially unchanged, currently at $122 billion:

The Fed splits these loans into category:

- Primary credit: $34 billion, down from $43 billion two weeks ago. Expanded to include “fallen angel” junk bonds. But since the expansion, the balance has dropped and the Fed hasn’t bought any fallen angel bonds.

- Secondary credit: $0. Designed to purchase corporate bonds, bond ETFs, and even junk-bond ETFs. None were purchased, but the Fed’s jawboning about it was enough to trigger a massive rally in junk bonds and junk bond ETFs.

- Seasonal credit: $0

- Primary Dealer Credit Facility: $32 billion, down from $36 billion last week. Amounts the Fed lent to primary dealers to buy stuff with. After the initial burst, nothing.

- Money Market Mutual Fund Liquidity Facility: $49 billion down from $53 billion two weeks ago. This is the money-market fund bailout where the Fed’s SPVs bought corporate paper and other short-term assets that money-market funds normally buy. After the initial burst, nothing.

- Paycheck Protection Program Liquidity Facility: $8 billion. Showing up for the first time. This is where the Fed lends to the SPV to buy from the banks the loans they have issued to “small businesses” under the PPP program.

So over the past four weeks, the Fed has not done any of the things with these SPVs and Primary Dealers that the markets were raving about it would do. It didn’t buy junk bonds, it didn’t buy ETFs, it didn’t buy stocks, it didn’t buy old bicycles. But Wall Street sure loved raving about it.

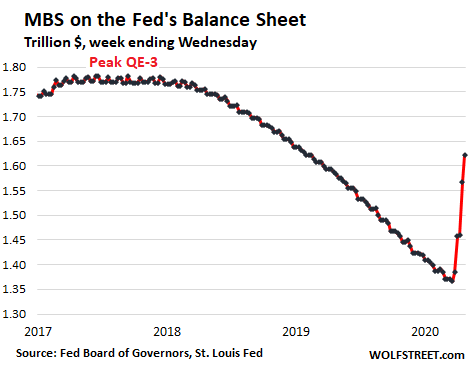

MBS purchases get tapered.

The Fed has slashed its purchases of MBS over the past three weeks, as reported by the New York Fed transaction summary (for the weeks ended):

- $157 billion (Mar 25)

- $145 billion (Apr 1)

- $109 billion (Apr 8)

- $58 billion (Apr 15)

- $56 billion (Apr 22)

MBS trades take a long time to settle. For example, all of the $56 billion in MBS the Fed bought this week will settle in May. The MBS the Fed bought last week will settle variously in April, May, and June. But the Fed books the trades only after they settle. So the Fed’s balance sheet lags by some time the actual trades.

Something else is different with MBS. Holders of MBS, including the Fed, receive pass-through principal payments as the underlying mortgages are paid down or are paid off. Due to the current boom in mortgage refinancing – 75% of all mortgage applications are now refis – these pass-through principal payments have become a torrent. Just to keep its balance of MBS level, the Fed would need to buy a significant amount of MBS.

On the Fed’s balance sheet, MBS increased by $54 billion to $1.62 trillion, down from an increase of $108 billion last week. This $54 billion increase is a mix of MBS trades that the Fed did in prior weeks and that just now settled, minus the torrent of pass-through principal payments:

The Fed has stated last year a number of times that it would like to get rid of the MBS on its balance sheet because they’re cumbersome to deal with for monetary policy purposes. And it was getting rid of them until the MBS market started blowing up in early March. That’s when the Fed held its nose and started buying them again.

If…

The Fed has printed $2.26 trillion since March 11 to inflate asset prices and bail out asset holders and Wall Street. If the Fed had spread that $2.26 trillion equally over the 130 million households in the US, each would have received $17,380. But this was helicopter money for Wall Street and the wealthy that were losing part their wealth in the sell-off. Those are the folks that matter to the Fed.