Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

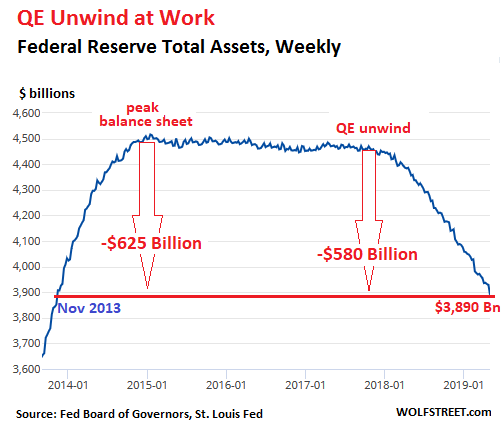

Fed sheds $46 Billion, Total QE Unwind Reaches $580 Billion. Assets drop to lowest level since Nov 2013.

In April, total assets on the Fed’s balance sheet fell by $46 billion, as of the balance sheet for the week ended May 1, released Thursday afternoon. This drop reduced the assets to $3,890 billion, the lowest since November 2013. Since the beginning of the “balance sheet normalization” process, the Fed has shed $580 billion. Since peak-QE in January 2015, the Fed has shed $625 billion:

According to the Fed’s old “balance sheet normalization” plan, which was still on autopilot in April, the QE-unwind would shed “up to” $30 billion in Treasuries and “up to” $20 billion in mortgage-backed securities (MBS) a month for a total of “up to” $50 billion a month, depending on the amounts of bonds that mature that month.

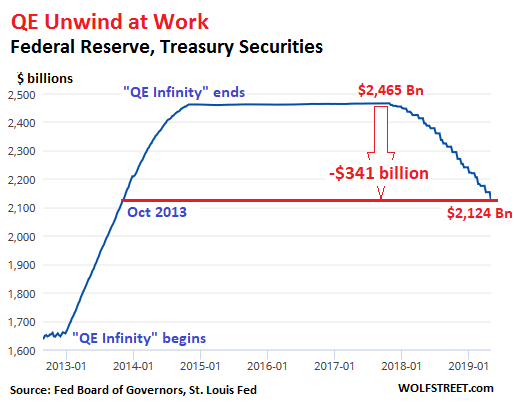

Treasury Securities

The Fed doesn’t actually sell its Treasury securities but allows them to “roll off” without replacement when they mature at mid-month or at the end of the month.

On April 15, $10 million in Treasury Inflation-Protected Securities (TIPS) and $169 million in Treasury securities in the Fed’s portfolio matured. On April 30, two issues of Treasuries matured, totaling $28 billion. Since all of it combined was below the $30-billion “cap,” all of it rolled off without replacement. This brought the Fed’s Treasury holdings down to $2,124 billion, the lowest since October 2013:

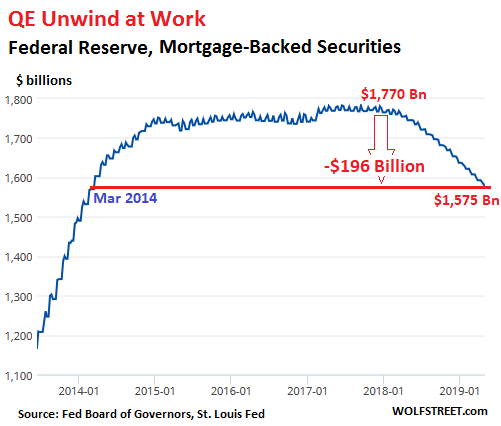

Mortgage-Backed Securities (MBS)

The residential MBS that the Fed still holds were issued and guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae. All holders of MBS, including the Fed, receive pass-through principal payments as the underlying mortgages are paid down on a monthly basis with each mortgage payment, or are paid off when the house is sold or the mortgage is refinanced. The remaining principal is paid off at maturity.

These pass-through principal payments are unpredictable and can cause the MBS balance in the Fed’s portfolio to decline erratically. To keep the balance steady after QE had ended, the New York Fed’s Open Market Operations continued purchasing MBS in the market, but the settlement lag of two to three months (the Fed books these trades at settlement) caused the zigzag moves in the MBS balance in the chart below.

In April, the balance of MBS fell by $17 billion to $1,575 billion, the lowest since March 2014. Since the QE unwind began, the Fed has shed $196 billion in MBS. But the runoff is nearly all due to pass-through principal payments because 95% ($1,503 billion) of the MBS on the Fed’s balance sheet mature in over 10 years:

The Fed has now outlined its new plan for its balance sheet. April was the last month on the old plan where the asset runoff proceeded on “autopilot.” In May, the transition begins with tapering the runoff of Treasury securities while maintaining the autopilot for MBS.

In October, a new regime kicks in that is intended to keep the balance sheet level, but replace MBS with shorter-dated Treasury securities with the goal of getting rid of those pesky MBS entirely by even selling them outright if the runoff is too slow.

In addition, according to Fed Chair Jerome Powell during the FOMC meeting press conference, the Fed is going to decide later in the year on the details of a huge component in this new plan: How to address the maturity-sinkhole that the Fed has been slipping into.

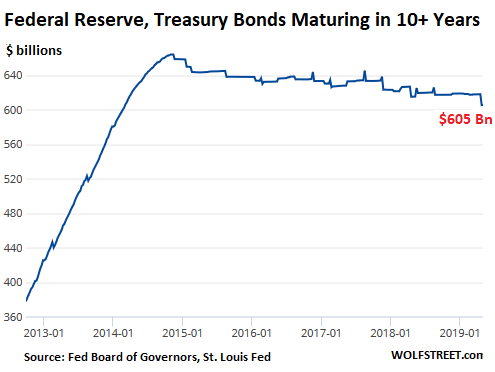

Of those $2,124 billion in Treasury securities, $605 billion are bonds maturing in over 10 years! This amount has not moved much since the QE unwind started:

The Fed has already announced that it wants to bring down the average maturity of its Treasury holdings to the average maturity of total outstanding marketable Treasury securities. This will require that the Fed take on short-term bills, of which it has none at the moment, and get rid of a portion of its long-dated Treasury notes and bonds. The Fed’s stepping away from those long-dated maturities is likely to put upward pressure on the 10-year Treasury yield which would steepen the yield curve a wee bit. Sit tight for details, Powell said.