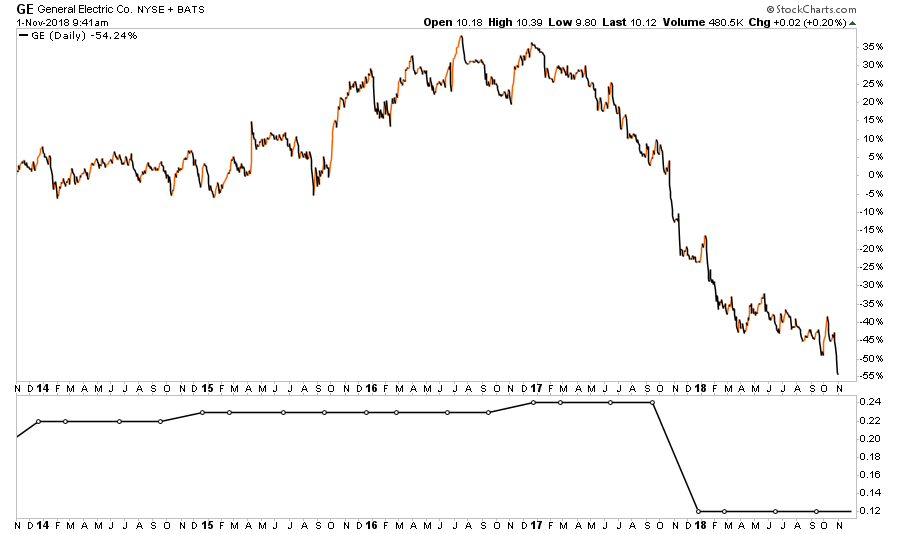

Last week, General Electric (GE) did something that many never thought would happen. They slashed their dividend to just $0.01 per share.

We are talking about GE. A company which has been bringing “good things to life” for well over 100-years.

There is an important lesson to be learned here by investors who have long bought into the myth of:

“I don’t care about the price, I bought it for the yield.”

First of all, let’s clear up something.

Company ABC is priced at $20/share and pays $1/share in a dividend each year. The dividend yield is 5% which is calculated by dividing the $1 cash dividend by the price of the stock.

Here is the important point. You do NOT receive a “yield.”

What you DO receive is the $1/share in cash paid out each year.

Yield is simply a mathematical calculation.

This is an important point which will become much clearer in just a moment.

In a previous article, I discussed the “Fatal Flaws In Your Financial Plan” which, as you can imagine, generated much debate. One of the more interesting rebuttals was the following:

“‘The single biggest mistake made in financial planning is NOT to include variable rates of return in your planning process.’

This statement puzzles me. If a retired person has a portfolio of high-quality dividend growth stocks, the dividends will most likely increase every single year. Even during the stock market crashes of 2002 and 2008, my dividends continued to increase. It is true that the total value of the portfolio will fluctuate every year, but that is irrelevant since the retired person is living off his dividends and never selling any shares of stock.

Dividends are a wonderful thing, Lance. Dividends usually go up even when the stock market goes down.”

Uhm…that isn’t actually true. But it is a comment which drives to the heart of the “buy and hold” mentality and, along with it, many of the most common investing misconceptions.

GE “Bringing Investing Mistakes To Life”

Here is why this distinction between yield and dividend is important. If a company pays a $1.00 dividend/share and is priced at $20/share then the “yield” is 5%. If the price of the stock, and your invested capital, declines by 50% you still ONLY receive $1.00/share but the “yield” increases to 10%.

The problem comes that when a company loses a significant chunk of its value, it is because there are fundamental issues with the company.

Case in point with General Electric.

“I only buy companies that regularly increase their dividends.”

Over the last 5-years GE has struggled with fundamental issues. But despite rising leverage, declining revenue, and falling returns on equity, the company increased their dividends in the previous 4-years. For those that had “bought it for the dividend,” and didn’t pay attention to the fundamental warnings, they have now not only lost 55% of their invested capital but have also watched the dividend all but disappear.

“But GE is just an anomaly. That isn’t the case for most companies.”

While I agree that “most” companies won’t cut their dividends, there will be many that will. GE is likely going to be an early indication of what will eventually be a more widespread issue in the near future.

Let me explain.

Eddy Elfenbein recently wrote about the “Bull Market In Dividends.”

“Over the last eight years, dividends are up 234%, which is pretty close to what the S&P 500 price index has done. Considering how simple it is, the S&P 500 has tracked a 2% dividend yield fairly closely for the last several years.”

It is an interesting point particularly when you consider that there are a lot of dividends which have been “financed” with “cheap debt.” There is also the issue of record debt issuance by companies with marginal balance sheets at best or are walking “zombies” at worst.

As noted by John Coumarionos:

“Low interest rates have allowed companies that would have otherwise gone out of business to stay alive, and this has caused a tepid recovery. Chancellor notes the cumulative default rate on junk bonds during the entire recession was 17%, or “around half the level of the two previous downturns.” And while central bankers might view this as a victory, he views it as the cause of economic weakness.

The lessons for investors are to remain vigilant about stock valuations and higher yielding bonds. At some point, the zombies will not be able to sustain themselves any longer.”

To John’s point, corporate leverage is at the highest level on record. This comes at a time where there has been a sharp change in the underlying interest rate environment. Historically, this has not worked out well for investors.

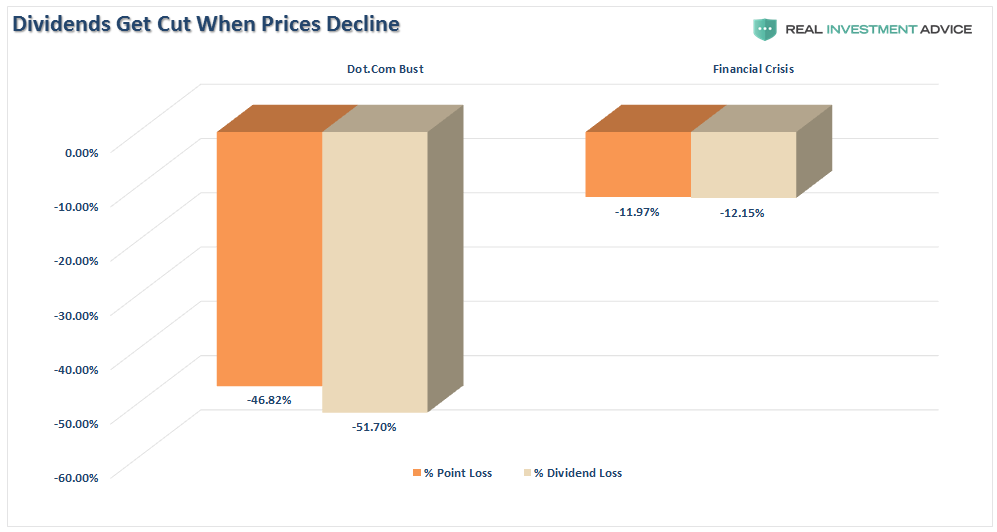

The issue of leverage was the focal point during the 2008 financial crisis. During that crisis, more than 140 companies decreased or eliminated their dividends to shareholders. Yes, many of those companies were major banks, however, leading up to the financial crisis there were many individuals holding large allocations to banks for the income stream their dividends generated. In hindsight, that was not such a good idea.

But it wasn’t just 2008. It also occurred dot.com bust in 2000. In both periods, while investors lost roughly 50% of their capital, dividends were also cut on average of 12%.

Since 2009, due to the Federal Reserve’s suppression of interest rates, investors have piled into dividend yielding equities, regardless of fundamentals, due to the belief “there is no alternative.” The resulting “dividend chase” has pushed the valuations of dividend yielding companies to excessive levels disregarding underlying fundamental weakness.

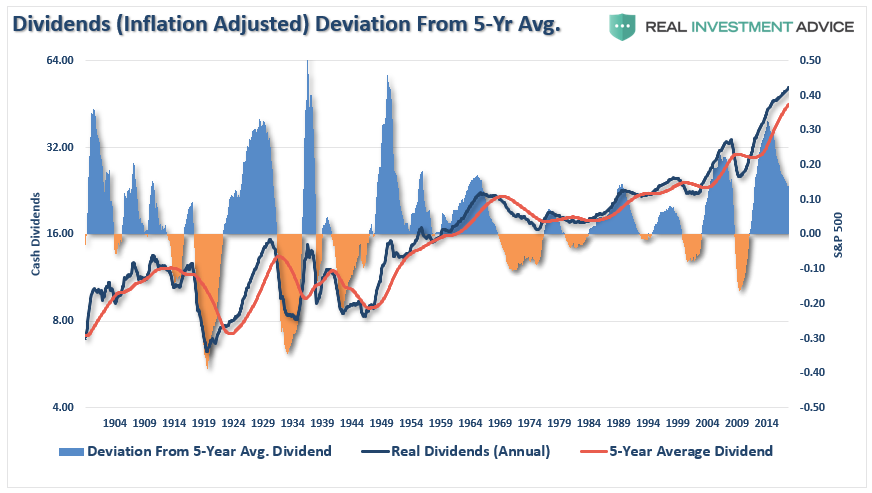

There is a high correlation between declines in asset prices and the actual dividends being paid out throughout history. The chart below shows the history of inflation-adjusted dividends and the S&P 500 going back to 1900. (Data courtesy of Dr. Robert Shiller.)

The first thing to note is the extreme deviation of real annual dividends above their long-term linear growth trend. Such extensions have ALWAYS mean reverted throughout history. (In other words, the best time to BUY dividend yielding companies is when the dividend has deviated well below the long-term growth trend.)

Here is another way to look at the same data. The chart below shows the percentage deviation above and below the 5-year average annual cash dividend. There are two things you should take note of.

- When deviations have exceeded a 20% deviation it has denoted very overvalued markets.

- Reversions below the 5-year average have been coincident with secular bear markets.

Notice that the current deviation from the 5-year average has already started to decline which is coincident with the Federal Reserve rate hike campaign. Given that much of the dividend issuance was done through cheap debt over the last decade, it is not surprising that with rising rates, the rate of dividend issuance has begun to slow which is likely indicative of a more troubling trend for investors.

While I completely agree that investors should own companies that pay dividends (as it is a significant portion of long-term total returns), it is also crucial to understand that companies can, and will, cut dividends during periods of financial stress. During the next major market reversion, we will see much of the same happen again.

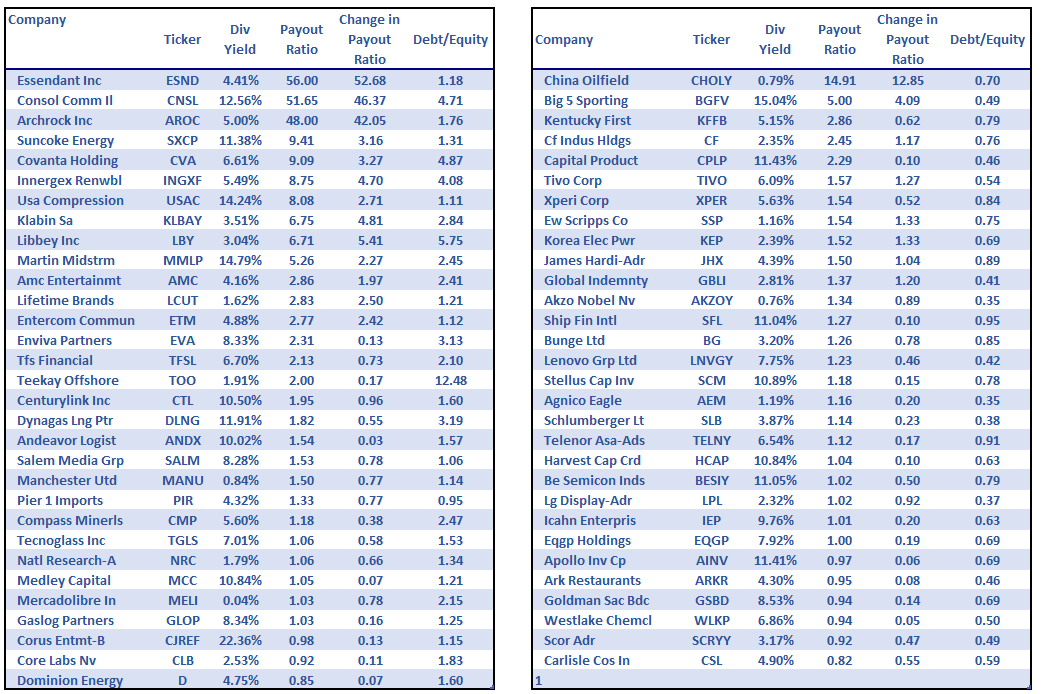

The table below shows 60-companies that are at risk during the next downturn (I reduced the list from more than 150 companies for the purposes of this article.) The screen looked for companies with a payout ratio above 80% and an increasing change in the payout ratio over the last 3-quarters. The list below does not contain REIT’s and MLP’s as their dividend payout policies are largely mandated by securities law and therefore hard to compare to other corporations.

Important Note: I am NOT suggesting that every company that fits these parameters will slash or eliminate their dividend. I AM suggesting there are a substantial number of companies at financial risk during the next economic downturn.

(Click here for the Top-10 Dividend Yielding Value Stocks hitting our screens now.)

There are two important lessons to be learned from General Electric (as well as numerous other companies which litter the “I bought it for the dividend” landscape of history):

- During a recession, when revenues fall, companies will cut their dividend to protect their creditors. This is especially important at a time when corporate leverage is at historical levels.

- The sharp decline in the stock price will precede the eventual cut to the dividend.

The reality is that every investor has a point, when prices fall far enough, that they will capitulate and sell their position. This point generally comes when dividends have been cut and capital destruction has been maximized.

While I certainly encourage investing in companies that pay a dividend, just remember that fundamentals are always THE single most important variable of long-term returns.

General Electric is just the latest lesson to be learned, and quite possibly the first, in a long line of dominoes.