Global 40’ Shipping Container Rate continues to plunge. pic.twitter.com/pooQHMdoRU

— Alastair (@StockBoardAsset) May 29, 2019

equity vol higher and ig credit spreads widening – stress is forming pic.twitter.com/C5I96VKETQ

— Alastair (@StockBoardAsset) May 28, 2019

Morgan Stanley Warns “Volatility Is About To Rise… A Lot”

With every passing day that the US China trade war is not resolved, it appears that Morgan Stanley’s bearish equity strategist, Michael Wilson, will be Wall Street’s most accurate forecaster for the second year in a row, because unlike various quants from JPMorgan who shall remain unnamed, he did not erroneously assume that trade war will be resolved quickly, and instead of slapping a lazy 3,000 S&P year-end price target, Wilson – despite being mocked by the likes of Bloomberg – remained stubborn in the face of the April market melt up, and said that it is only a matter of time before stocks rerate sharply lower.

So just to remind Morgan Stanley clients that unlike most of his peers who are nothing but lagging indicators, their calls flip-flopping every several weeks depending on which way the S&P moves, Wilson has published a report today in which he makes three rather bold calls:

- Trade is not the only risk to growth.

- Adjusting the yield curve for QE and QT shows a persistent inversion for the past ~6 months, suggesting recession risk is higher than normal.

- volatility is about to rise…a lot.

The first of three should be intuitive to anyone who has been following the market in the past month. As Wilson notes, looking at the most recent disappointing macro data including poor durable good, capital spending and Markit PMIs, “recent data points suggest US earnings and economic risk is greater than most investors may think.”

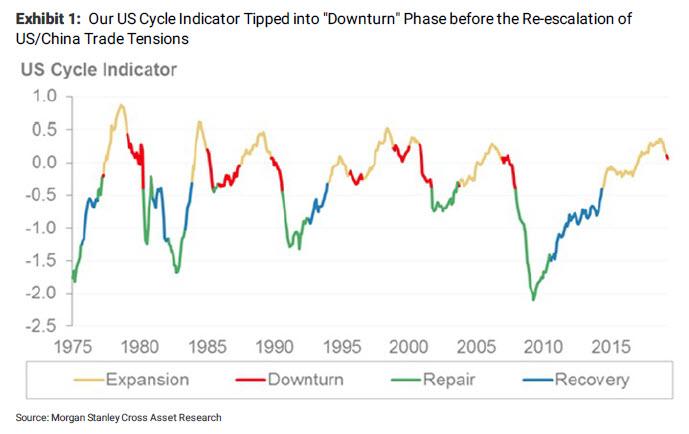

Supporting that claim is the fact that our US Cycle indicator moved into a downturn phase based on the April data which was before the trade talks broke down in early May (Exhibit 1). The OECD leading indicator also fell to its lowest level since the last recession. In addition, we are now hearing from many leading semiconductor (INTC, MCHP) and industrial companies (CAT, DE) that the second half recovery many are counting on is looking less likely. Like the weaker macro data in April, we don’t think these softer outlooks are the result of the uncertainty in the US/China trade negotiations. In the past week, our economists have lowered their 2Q US GDP forecast to 0.6% from 1.0%. We suspect this could deteriorate further if trade negotiations don’t improve soon.

And since all of these reflect April data – which means it weakened before the re-escalation of trade tensions – the latest trade war will only make a dismal economic picture worse. In addition, Wilson claims, “numerous leading companies may be starting to throw in the towel on the second half rebound”, something the Morgan Stanley strategist has repeatedly warned about even though “many investors are not.”

In short, “get ready for more potential growth disappointments even with a trade deal.”