via mises:

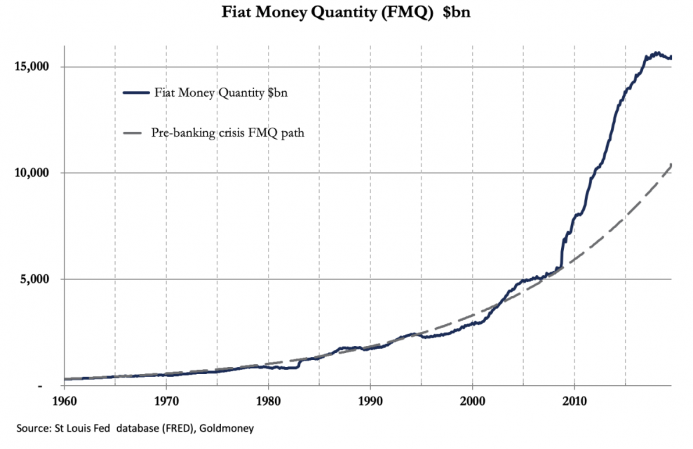

Listening to recent commentaries about the repo failures in New York leads one to suppose there is insufficient money in the system. This is not the real issue, as the chart below of the fiat money quantity for the dollar clearly shows.

The fiat money quantity is the amount of fiat money (in this case US dollars) both in circulation and held in reserve on the central bank’s balance sheet. Before the Lehman crisis, it grew at a fairly constant compound growth rate of 5.86%. Since the Lehman crisis, it has grown at an average of 9.45%, even after the slowdown in its rate of growth that started in January 2017. FMQ is still $5 trillion above where it would have been today if the massive monetary expansion in the wake of the Lehman crisis had not happened. If there is a shortage of money, it is because the process of debt creation to fund current expenditure is spiralling out of control.

It is not just the US. If we take similar (but less detailed) figures for FMQ in other major nations by adding together broad money M3 and central bank balance sheets, we find that it has increased at varying rates for the most important economies. In China, the compound annual growth rate has been 12% — although the growth in Japan at 5.2%, and in the Eurozone at 4.9%, has been more subdued, reflecting stagnant levels of bank credit. When, for the lack of any other measure, statisticians use a GDP money total as a substitute for defining economic progress, we should not be surprised to see that the economies with the greatest rate of monetary growth are reckoned to be the best performing.

Just as GDP tells us nothing about human progress and its benefits to society, other uses of money as a control mechanism for economic management are equally misleading. Much of the monetary expansion has been to fund unproductive government spending. Most of the balance after the government’s cut has fuelled speculation in the financial sector and has funded consumer credit for those whose savings have been tapped out. Not revealed by the acceleration of money supply growth is the wealth transfer effect which impoverishes every productive individual for the benefit of governments, the banking system, and the bank’s favoured customers. These latter groups are, in the main, large corporates and — directly or indirectly — the hedge funds.

The Real Reason It Looks Like There’s a Money Shortage

Decades of impoverishment by monetary inflation, which has quickened since Lehman, is a very serious matter and is behind the fragility of economic systems dominated by government spending deficits. The reason there appears to be not enough money is because the acceleration of government liabilities in nominal currency terms is catching up with them. Laurence Kotlikoff’s famous 2012 estimate of the US Government’s future commitments of a net present value of over $222 trillion is very much alive on arrival.

It would be more accurate to say the figure for the US is trending towards infinity. It is already infinity in Japan and the Eurozone, where negative interest rates and bond yields offer the basis for the net present value calculation. As in most things financial, the public is blissfully unaware of the true implications of low and negative interest rates and ultra-low bond yields. They take the view that very low interest rates permit their government to borrow as much as it likes to provide the public with new hospitals, schools and the like. It is a case of fools of politicians and central bankers having turned everyone else into fools, and the few who realise it have no idea how to reverse the process. What they do not see is the government cannot now fund public healthcare and pensions, which make up the bulk of future obligations in a welfare state, without accelerating monetary debasement even more.

No one can know what the true figure is for future government liabilities, of which welfare is an increasing component. Politicians, who claim that a week in politics is the long term, fail to see any problem. The few governments which have raised retirement ages have done so to deal with escalating current welfare liabilities, not addressing those of the future that will lead ultimately to the destruction of what as Westerners we generally agree is civilised democratic society. That is their successors’ problem.

If history and reasoned economic theory is any guide, the demands for credit by the state will terminate in the destruction of government currencies. For the truth of the matter is inflation of money, and credit has created the illusion we can all live beyond our income, our income being what we produce.

Nothing, with the sole exceptions of a central bank and its commercial charges can make money without having to advertise for it: the seigniorage is simply taken without public consent. Without questioning how it arises, the extra money allows us to indulge in all our flights of fancy until at some time reality strikes. Rather like Monty Python’s glutton, Mr Creosote, can we force in a little more inflation before we all explode?

Excerpted from Monetary Failure is Becoming Inevitable