Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

A slew of reasons, the China debacle on top.

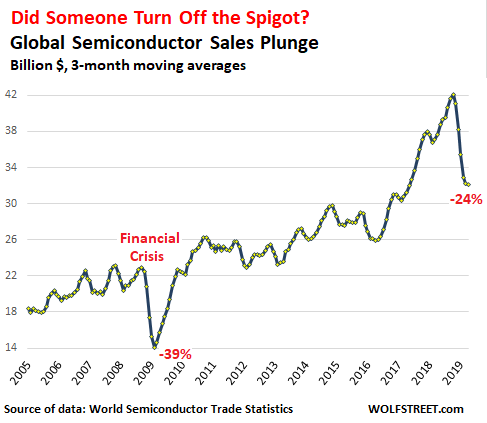

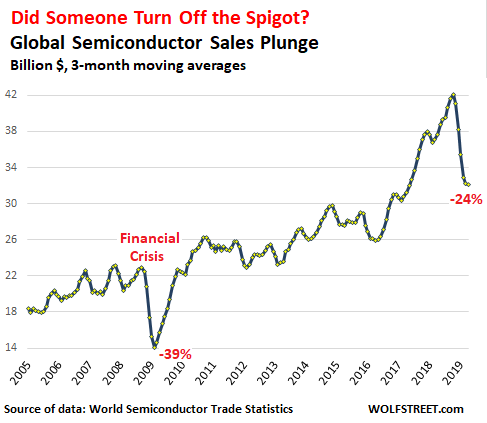

Global semiconductor sales dropped 14.6% in April from April last year, to $32.1 billion, on a three-month moving average basis, the World Semiconductor Trade Statistics (WSTS) organization reported Tuesday afternoon. The three-month moving average in April has plunged 24% from the peak last October, thus continuing the deepest plunge in semiconductor sales since the Financial Crisis:

In dollar terms, semiconductor sales plunged by over $10 billion in April compared to the pace in October 2018, the largest peak-to-trough dollar-drop ever. During the Financial Crisis, chip sales dropped by $9 billion from peak to trough.

But in percentage terms, the current plunge doesn’t quite measure up: 24% versus the 39% collapse during the Financial Crisis and the 45% collapse during the long dotcom bust.

The Semiconductor Industry Association (SIA) said in its press release that sales, based on the data compiled by the WSTS, dropped in all major geographic regions in April (three-month moving averages compared to the same period last year):

- Americas: -29.5%

- Europe: -8.0%

- Japan: -10.9%

- China: -10.9%

- Asia Pacific/All Other: -10.7

And sales may not pick up anytime soon:

The SIA “endorses” the WSTS projections that chip sales for the full year 2019 will fall by 12% from the record levels of 2018, to $412 billion. In terms of regions, the SIA expects semi sales to fall across the board for the full year 2019:

- Americas: -23.6%

- Europe: -3.1%

- Japan: -9.7%

- China and other Asia Pacific: -9.6%

So maybe next year: The SIA expects that sales in 2020 will “bounce back somewhat, posting moderate growth of 5.4%,” from the much lower levels in 2019.

The huge spike and plunge that the semiconductor industry is facing currently is a result of several factors piling on top of each other.

The China debacle.

Potential tariffs and trade tensions between the US and China and potential export controls of tech products, such as semiconductors, to China has caused a stampede in 2018 to front-run these policies.

Just how prescient this stampede was has now been demonstrated by US efforts to clip the wings of Chinese tech and telecom giant Huawei Technologies, whose telecom infrastructure equipment (think 4-G and 5-G) and smartphones, are sold around the globe. They contain US semiconductors. And Huawei has been preparing for these eventualities.

Since the middle of 2018, Huawei has been stockpiling chips and other tech components. Bloomberg reported that according to its sources, it stockpiled enough components to keep its business running for at least three months after it gets cut off from US suppliers. This would give it some time to realign its supply chain.

The Nikkei, citing “multiple sources,” reported in May that Huawei has stockpiled six months’ to a year’s worth of “crucial components,” such as semiconductors, that had a higher risk of falling under export controls, to prepare for a worst-case scenario where its key suppliers would be barred from doing business with it. And it has stockpiles of less crucial components that would last for three months.

Huawei is not the only Chinese tech company that has been preparing for these scenarios. Acquiring these stockpiles means accelerated purchases. This is likely one of the reasons for the long spike in the chart above that peaked in October. And after these companies had acquired the stockpiles, chip sales began to drop.

Decline in global smartphone sales.

Global smartphone sales went from stagnation in 2018 into decline in Q1 2019. According to Gartner Inc., sales in Q1 fell 2.7% compared to the same period last year to 373 million units. Huawei was number two, behind Samsung, and both of them far ahead of Apple. iPhone sales in Q1 plunged 17.6% year-over-year. You see, Apple is now trying to sell services to brush off its dismal iPhone sales. These dynamics put a dent into semiconductor sales.

Decline in global PC and laptop shipments.

Global PC and laptop shipments in Q1 fell 4.6% year-over-year to 58.5 million units, according to Gartner. The Big Three vendors – Lenovo, HP, and Dell – were able to increase their shipments. And their market share rose to 61.5% in Q1, up from 56.9% a year earlier. The smaller kids on the block lost out. Apple’s shipments fell 2.5%. The remaining vendors were confronted with larger drops, ranging from -7.3% for Asus and -13.2% for Acer to -20.9% for all others.

The Crypto-mining collapse.

Demand for special rigs to mine cryptocurrencies collapsed in 2018, and this hit semiconductor makers, such as Nvidia, that make these specialized chips.

Data Center boom slows down. China’s fault again.

Data centers are part of the infrastructure of the “cloud.” This business had been on a relentless boom. And it may still be, but…. Intel caused its shares to swoon with its Q1 earnings report when it disclosed that chip sales of its data-center unit had fallen 6.3% from a year ago, due to weakness in China and large stockpiles among its customers. This came after a warning in January about slowing data center sales in Q4.

CEO Bob Swan said that Intel’s customers in China had “absolutely” stockpiled extra data center chips in 2018 due to the risks of tariffs or export controls. And those stockpiles are still around and need to be consumed.

This spike and plunge in semiconductor sales is a result of a confluence of factors. The global decline in demand for smartphones and PCs – both now mature markets – would have been enough to turn chip sales down. But the China trade issues, the frontrunning of tariffs and export controls, the stockpiling of chips, now topped off by actual tariffs and export controls did much of the rest.

Exports-at-all-costs for economic growth comes home to roost. Read... US Cleanest Dirty Shirt Among Manufacturing Giants: Germany at Crisis Level. China, Japan, South Korea Contract