Financialization was never sustainable, and neither was the destructive globalization it enabled.

All the happy-story analogies to past pandemics being mere bumps in the road miss the mark. A popular claim is that the 1918-1919 flu pandemic killed millions but no biggie, the Roaring 20s started the following year. It’s onward and upward, baby, once we toss the masks.

Wrong. Completely, totally, dead wrong. The drivers of the past 75 years of growth– globalization and financialization–are dead, and so is everything that depended on them for “growth”. (Growth is in quotes because once external costs and currency arbitrage are factored in, most of what’s been glorified as “growth” is nothing but losses covered by accounting trickery.)

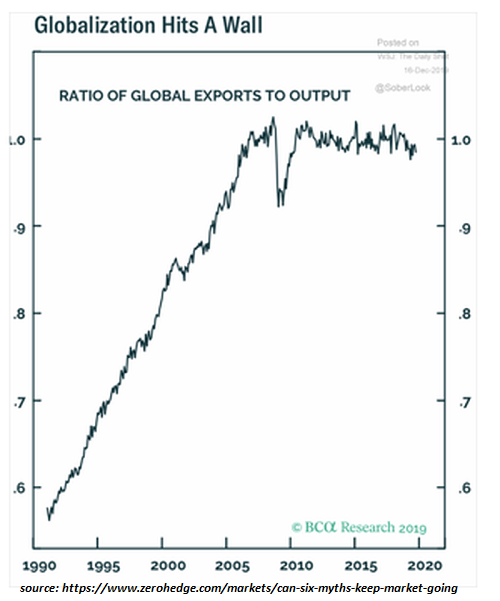

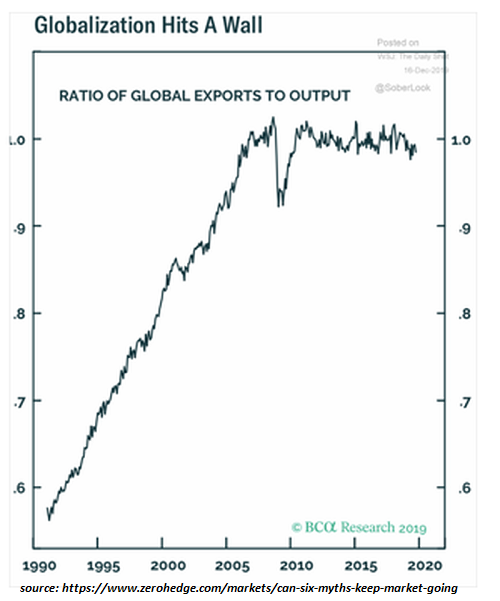

Here’s what’s poorly understood: globalization and financialization die when they stop expanding. Just as a shark dies if it stops swimming forward, globalization and financialization die once they stop expanding, because their viability depends on expansion.

Globalization and financialization have been losing momentum for years. Under the guise of “opening markets,” globalization has stripmined every economy that can’t print a reserve currency and hollowed out economies globally as only globally competitive sectors survive globalization. The net result is that once vibrant, diversified economies have been reduced to fragile monocultures completely dependent on global flows of capital and spending for their survival.

Tourism is a prime example: every region that has seen its local economy crushed by global arbitrage and corporate hegemonies, leaving global tourism as its sole surviving sector, has been devastated by the drop in tourism, which was always contingent on disposable income and credit expanding forever.

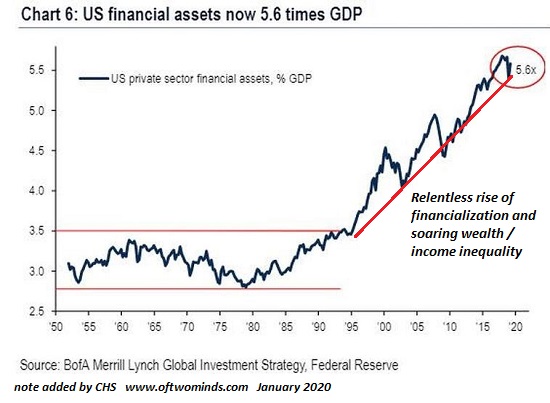

But credit can’t expand forever, as it eventually runs out of income to service additional debt. Financialization is not just the expansion of credit and leverage to marginal borrowers; it’s also legalized looting as the true risks of soaring debt and leverage are hidden in obscure financial instruments and bogus claims of “safety” and “hedging.”

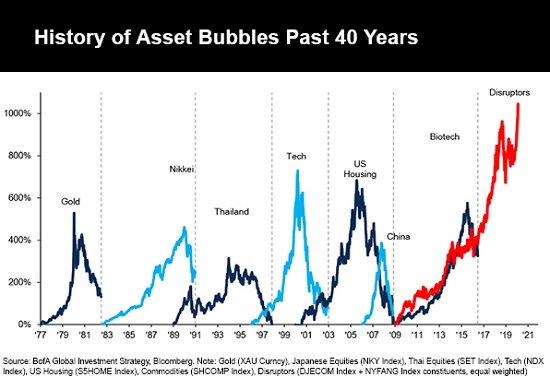

Excesses of debt and leverage funneled into risky speculations inevitably end in default. Financialization manifests as asset bubbles and hyper-consumption as people who never had credit spend up to the credit limits and beyond. Both asset and consumption bubbles pop, pushing the financial sector that feasted off the unsustainable expansion of credit into insolvency.

In other words, neoliberal globalization and financialization–essentially one dynamic– are inherently destabilizing, as all the incentives are perverse and exploitive. Just as asset and consumption bubbles are inevitable, so too is the bursting of those bubbles and the devastation of everything that had become dependent on the expansion of those bubbles.

The common good, long derided by those feasting on the excesses of globalization and financialization as nationalism, is now understood as the resilience and security that’s been sacrificed at the altar of globalization and financialization. Food security, to take a basic example, is impossible once globalization has destroyed local agricultural production, and financialization has rewarded factory-farming since Big Ag can borrow capital at scales that only make sense in a world of globalized monoculture agriculture.

Everyone touting 1919 as the model for 2020 is deeply ignorant of history and the destructive ontologies of globalization and financialization. There is virtually no overlap between the world of 1919 and the world of 2020 in terms of financial structures and excesses.

That globalization and financialization are dead is revealed by what Federal Reserve bailouts and fiscal free-for-alls cannot do:

1. They cannot create creditworthy borrowers out of thin air like the Fed creates dollars out of thin air.

2. They cannot force lenders facing mass defaults to loan more money to uncreditworthy borrowers

3. They cannot force creditworthy borrowers to borrow money.

4. They cannot reflate asset and consumption bubbles that have popped.

5. They cannot restore confidence in long, fragile supply chains.

6. They cannot magically turn unprofitable enterprises into profitable enterprises.

7. They cannot create income streams–revenues, profits, wages, etc.–with bailouts that continue the perverse incentives of moral hazard or “free money” designed to give debt-serfs enough cash to continue making their loan payments.

8. They cannot forgive debt payments without destroying the wealth held as debt: mortgages, student loans, auto loans, credit card debt, corporate junk bonds, etc. are assets that lose their value once borrowers default.

9. The Fed can buy impaired debt, but that doesn’t change their abject powerlessness (points 1 through 7 above).

Financialization was never sustainable, and neither was the destructive globalization it enabled. Any system that depended on the ever-expanding exploitation of new resources, debtors and markets could never be anything but fragile. The ferociousness of its rapacity masked its inherent weakness, a weakness that is now exposed as fatal.

I explain these dynamics, and the way they undermine democracy, in my short book Why Our Status Quo Failed and Is Beyond Reform.

New podcast: AxisOfEasy Salon #4: What comes after the failure of Neo-Liberalism? (57:51) (Mark, Jesse and I dig into the pathways opened by the collapse of neoliberal globalism)