Going to all cash in your portfolio to avoid a crash can be just as costly as the crash itself. A recent CNBC article quoted a $200 billion money manager suggesting “every stock market investor should be ready to go to cash.”

The comment was from Ashbel Williams, who retired from the Florida State Board of Administration.

“You never want to be a forced seller of risk assets at reduced prices because of market turmoil that locks in permanent capital impairment. There always has to be liquidity when equity markets go down. The No. 1 way to protect capital is to follow investment policy and rebalance back into equities while at depressed prices.”

Regular readers of our columns are already well aware we agree with Ashbel on raising cash to avoid drawdown risk. However, there is an essential distinction between “going to all cash” and “raising cash” to manage risk.

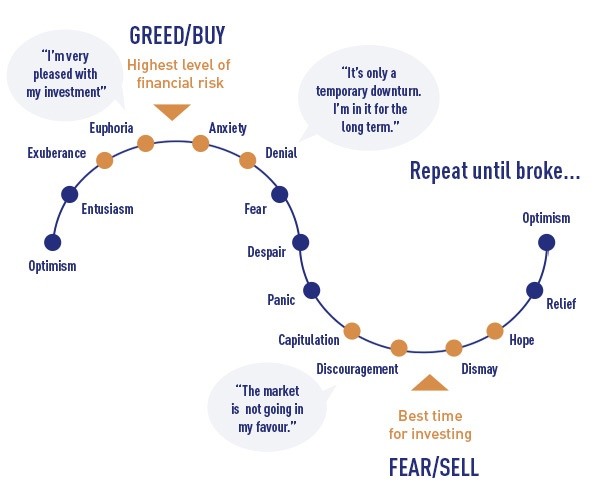

The Psychology Trap

The biggest battle for all investors is their own “psychology.”

From “herding” to “anchoring” to “confirmation bias,” individuals exhibit the same set pattern of responses through the entire investing cycle. Such was a point we discussed recently in “Is Past Performance A Guarantee?”

“During a bull market, people tend to forget about bear markets. As far as human recent memory is concerned, the market should keep going up since it has been going up recently. Investors therefore keep buying stocks, feeling good about their prospects. Investors thereby increase risk taking and may not think about diversification or portfolio management prudence. Then a bear market hits, and rather than be prepared for it with shock absorbers in their portfolios, investors instead suffer a massive drop in their net worths and may sell out of stocks when the market is low. Selling low is, of course, not a good long-term investing strategy.” – Morning Star

When it comes to “going completely to cash” in portfolios, such action triggers numerous emotional behaviors that negatively impact portfolio outcomes.

Over the past decade, I have met with numerous individuals who “went to cash” in 2008 before the crash. They felt confident in their actions at the time. However, that “confidence” gave way to “confirmation bias” after the market bottomed in 2009. Nevertheless, they remained convinced the “bear market” was not yet over and continued to seek out confirming information.

As a consequence, they remained in cash.

The Fear Of Being Wrong

The cost of “sitting out” on a market advance is evident.

As the market turned from “bearish” to “bullish,” many individuals remained in cash, worrying they had missed the opportunity to get in. Even when there were decent pullbacks, the “fear of being wrong” outweighed the necessity of getting capital invested.

The problem with being completely in cash is that it becomes increasingly difficult to break those “psychological” barriers to getting capital invested as the market advances.

- The market has already run up too much.

- What if I buy in now and the market crashes?

- I’ve already missed so much, I will just wait for the next crash.

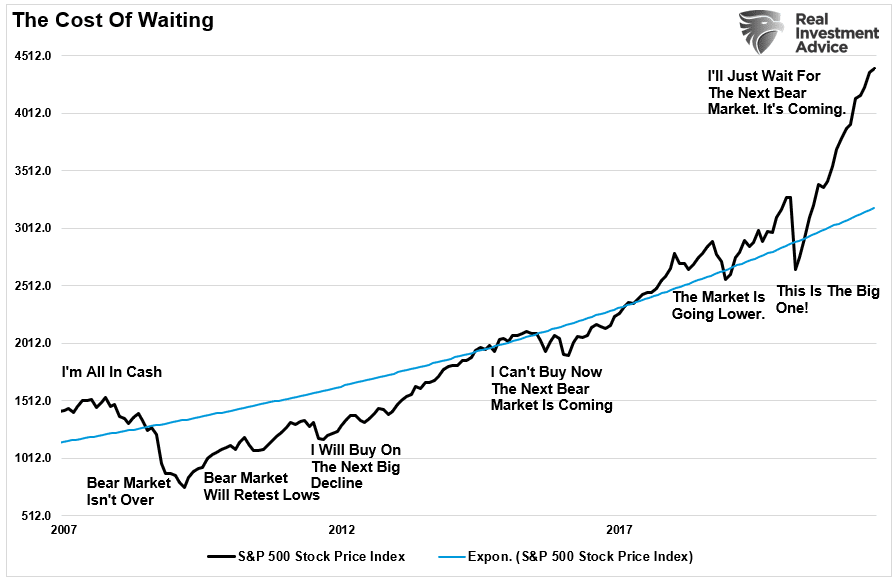

The Cost Of Waiting

While being entirely in cash certainly has psychological freedom, it also has negative financial consequences. The chart below shows the impact more clearly.

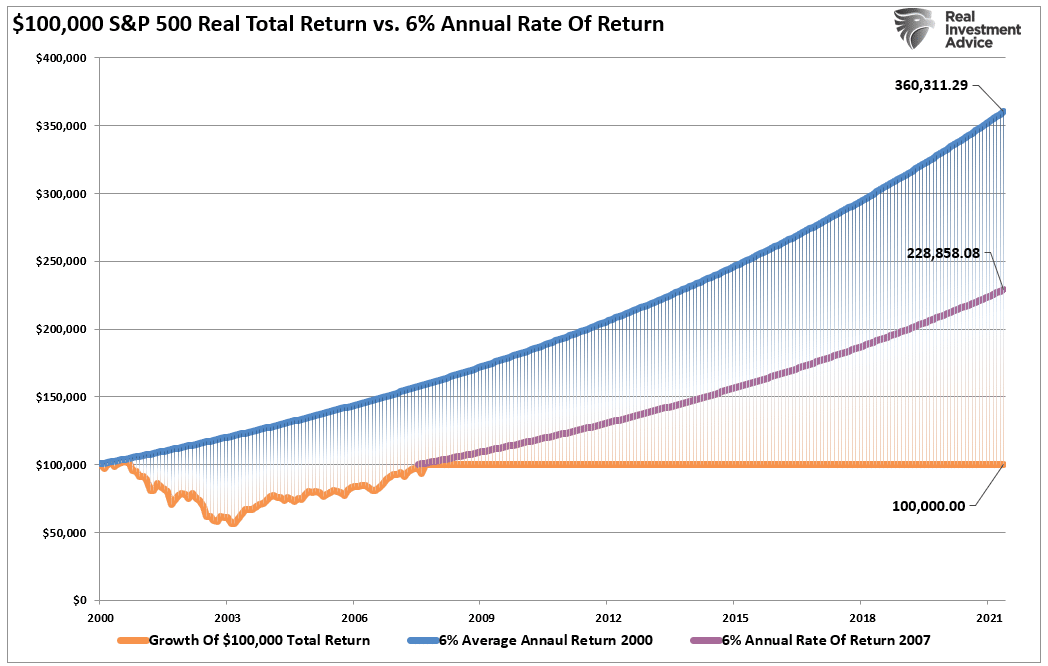

We assume an individual invests $100,000 at the turn of the century. They ride the market down and back up to their original value in 2007. Then, having “learned their lesson,” they see the signs of an impending market crash and go to cash. While they avoided the 50% decline in 2008, remaining in “cash” has put them significantly behind their 6% annualized return needed to meet financial goals.

This is certainly a more extreme example. However, there are many individuals who remain out of the markets today due to fear of suffering a “mean reverting” event.

However, is there a better way?

Reduce Cash Rather Than Liquidate

You cannot, over the long term, effectively time the market. Being all in or out of the market will eventually put you on the wrong side of the “trade.”

However, you can manage risk and protect investment capital.

When it comes to managing risk there are many sophisticated methods for doing so, and entire books have been written on the subject. But risk management doesn’t have to be overly complicated. Even a very basic moving average crossover can be a valuable tool over the long-term holding periods.

Will such a method ALWAYS be correct? Of course, not.

However, will such a method keep you from losing significant amounts of capital? Absolutely.

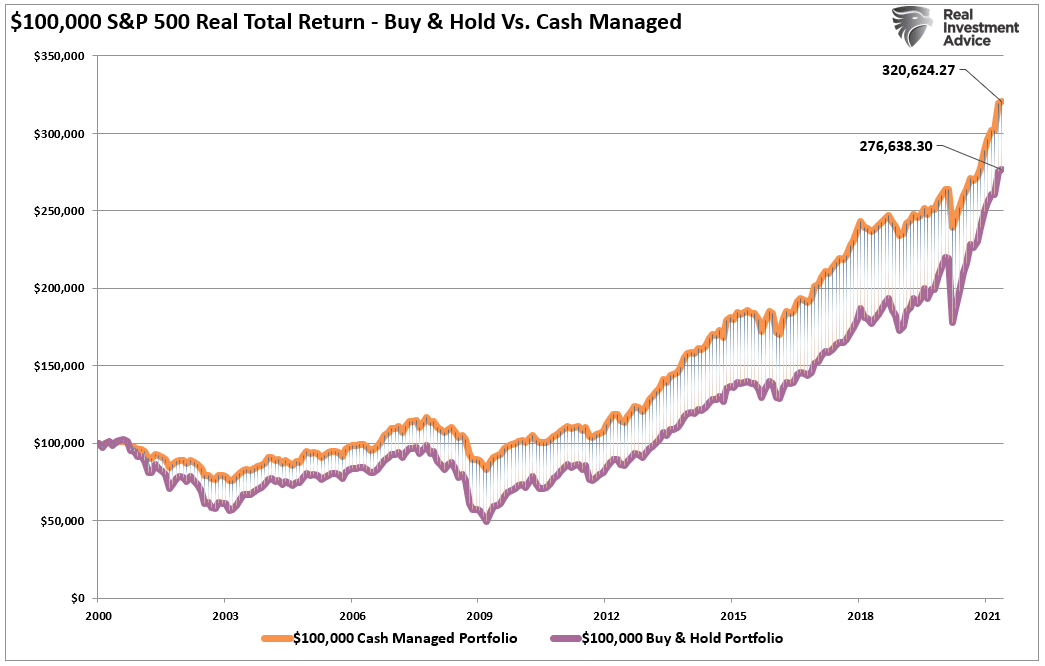

Let’s use our basic example from above. We will assume our investor understands market risk but is very slow at making transitions. In this example, we assume our investor:

- Puts 50% of his capital in 2000 and immediately gets swept into the “Dot.com” crash.

- Being concerned about the decline, they remain 50% invested until mid-2004.

- Finally investing the rest of their capital, they participate with the market before selling down by 50% in 2008.

- They don’t increase back to 100% equity exposure until late 2010.

- From 2010, they remain fully invested until reducing to 50% cash in 2017.

- They remain 50% cash until the end of 2020 before going back to full equity exposure.

As shown, even though our hypothetical investor was late exiting and re-entering the market, they still substantially outperformed a “buy and hold” investor over the same time frame.

Never Go 100% Into Cash

Our inherent human biases make us extremely fallible creatures when investing. Inherently, we will all do precisely the opposite of what we should do. First, we will “buy high” as “greed” overtakes our base logic. Then, we will “sell low” as “panic” over mounting losses.

But we can do better but understanding our essential behavioral traits and learning that we can manage the amount of risk that we take in our portfolio management strategies.

- Avoid the “herd mentality” of paying increasingly higher prices without sound reasoning.

- Do your own research and avoid “confirmation bias.”

- Develop a sound long-term investment strategy that includes “risk management” protocals.

- Diversify your portfolio allocation model to include “safer assets.”

- Control your “greed” and resist the temptation to “get rich quick” in speculative investments.

- Resist getting caught up in “what could have been” or “anchoring” to a past value. Such leads to emotional mistakes.

- Realize that price inflation does not last forever. The larger the deviation from the mean, the greater the eventual reversion will be. Invest accordingly.

Despite the inherent belief that we are long-term investors, we all consistently get swept up in the market’s short-term movements. Of course, with the media and Wall Street pushing the “you are missing it” mantra as the market rises; who can blame the average investor for “panic” buying market tops and selling out at market bottoms.

It’s Never Easy

The problem with going to all cash in a portfolio is that it becomes psychologically challenging to redeploy that cash in the future. To better navigate markets over time, choose a base level of exposure that you will never go below no matter how bad it gets in the market. (We utilize a base of 25% of total equity allocation targets.)

The benefit of having a base level of exposure is that as the market begins to recover, it becomes psychologically easier to “buy into” an existing allocation that is beginning to recover. However, since invested capital got protected from the decline, that capital gets quickly reallocated to equity risk at depressed levels.

While it may seem logical to go to cash to avoid “crashes,” the risk of mistiming the event can have the same negative impact on financial goals as the crash itself.

Notably, managing risk is not the same as avoiding risk.

We can’t invest capital without the acceptance of risk. However, we can take actions to minimize the impact of risk when things don’t work out as anticipated.