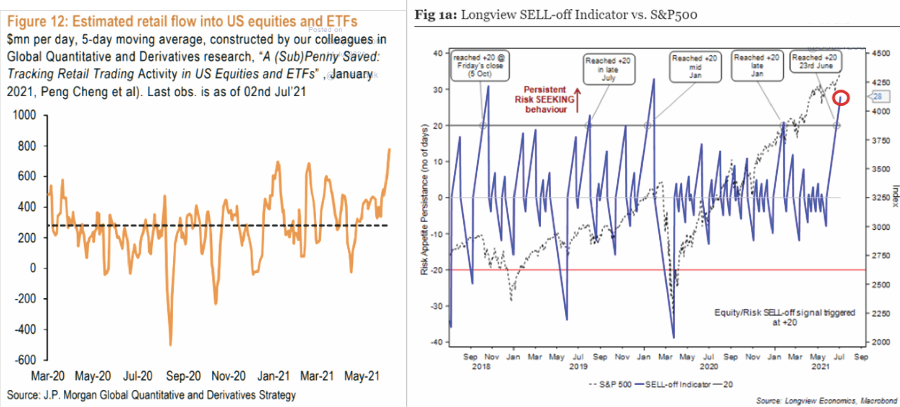

The “Fear Of Missing Out” has infected retail and hedge funds alike as they ramp up exposure to chase performance.

We have previously discussed the near “mania” of retail investors taking on exceptional risk in various manners. From increasing leverage, engaging in speculative options trading, and taking out personal loans to invest, it’s all evidence of overconfident investors.

However, that “risk appetite” is not relegated to retail investors alone. Professional managers, institutions, and hedge funds are “all in” as well.

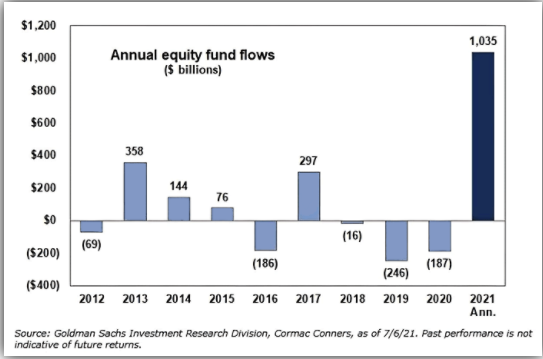

Money Flows Are Huge

The evidence of “professional investor” exuberance is the massive inflows of capital. The first half of 2021 outpaced every year since the Financial Crisis lows.

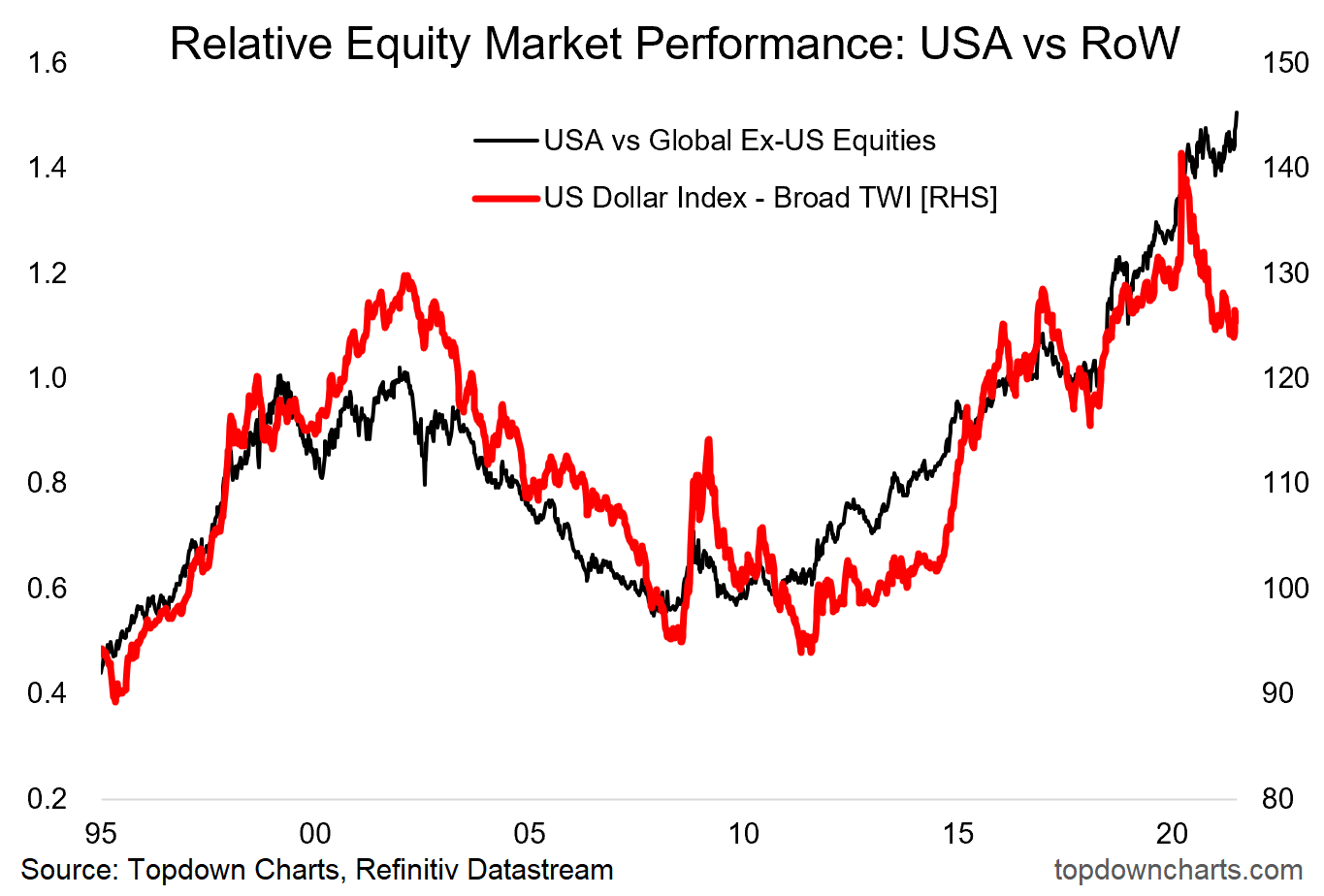

That surge in inflows came from a rotation of foreign investors. The inflows are a function of expectations for more robust economic growth in the U.S. relative to their home country. The divergence in performance between the “Rest Of The World” and the U.S. represents the performance chase.

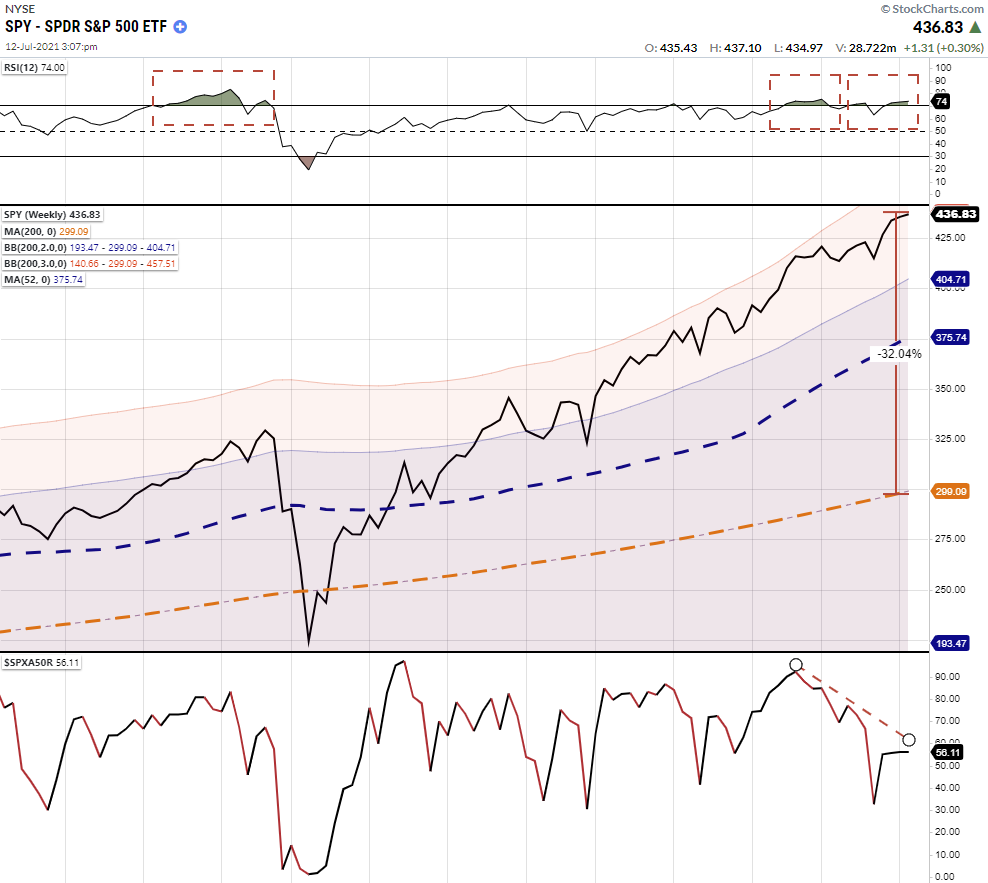

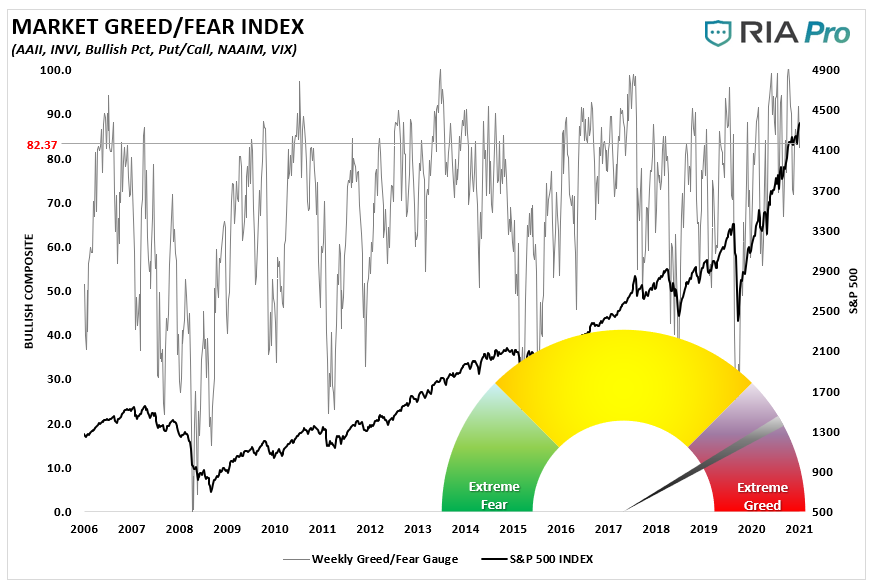

One issue is the extreme overbought and deviated conditions of the U.S. market. Such conditions, when coupled with a deterioration of participation of stocks, remain a concern. (Bottom panel)

A Mental Formation

Nonetheless, given the $120 billion a month in “Quantitative Easing” by the Federal Reserve, it is not surprising to see the “performance chase” in action. As noted in “Market Will Soon Reach 4500,” it all comes down to the “psychology” of QE:

“The key to navigating Quantitative Easing! and Fed policy in general is to recognize that their effect on the stock market relies almost entirely on speculative investor psychology. See, as long as investors get inclined to speculate, they treat zero-interest money as an inferior asset, and they will chase any asset with a yield above zero (or a past record of positive returns). Valuation doesn’t matter because investors psychologically rule out the possibility of price declines in the first place.” – John Hussman

In other words, “Quantitative Easing” is a mental formation. Therefore, the only thing that alters the effectiveness of the Fed’s monetary policy is investor psychology itself.

Such was a point we made in the “Stability/Instability Paradox.”

“With the entirety of the financial ecosystem now more heavily levered than ever, due to the Fed’s profligate measures of suppressing interest rates and flooding the system with excessive levels of liquidity, the ‘instability of stability’ is now the most significant risk.”

Given professional managers are subject to “career risk,” they get forced to “chase performance.”

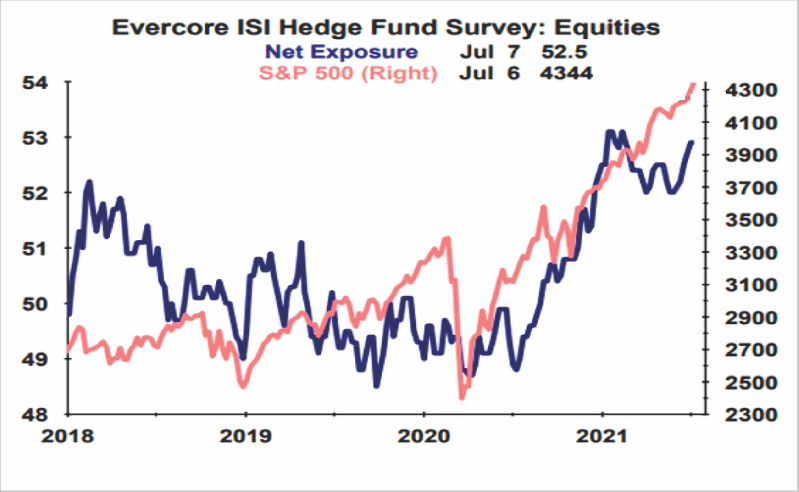

Hedge Funds Are All In

Hedge fund managers are now extremely long “risk” exposure.

As stated, that “career risk” has professional managers chasing performance after suffering a rough start to the year. The need to make up lost ground, or risk losing assets to better-performing managers, rises with the market. Per the Wall Street Journal:

“Client notes from both Morgan Stanley and Goldman Sachs show fundamental stock-picking manager had negative alpha in the first half of the year.

Part of the challenge for professional stock pickers is that markets are heavily rotational. Markets this year whipped back and forth between growth and value stocks. Such makes it difficult for managers to find winning trades.”

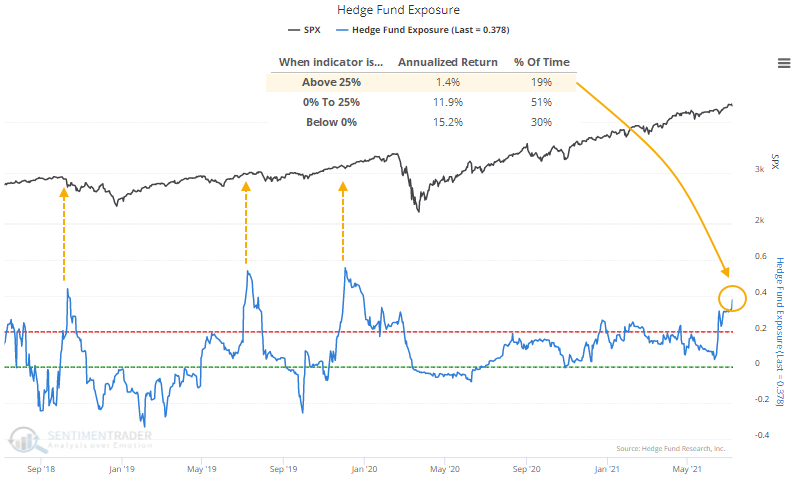

Sentiment Trader had an excellent piece of data to this point:

“The latest estimate of Hedge Fund Exposure shows that funds are nearly 40% net long stocks, a quick rise from almost being flat a month ago. Over the past few years, after such large allocation increases, the S&P gave any further gains back.”

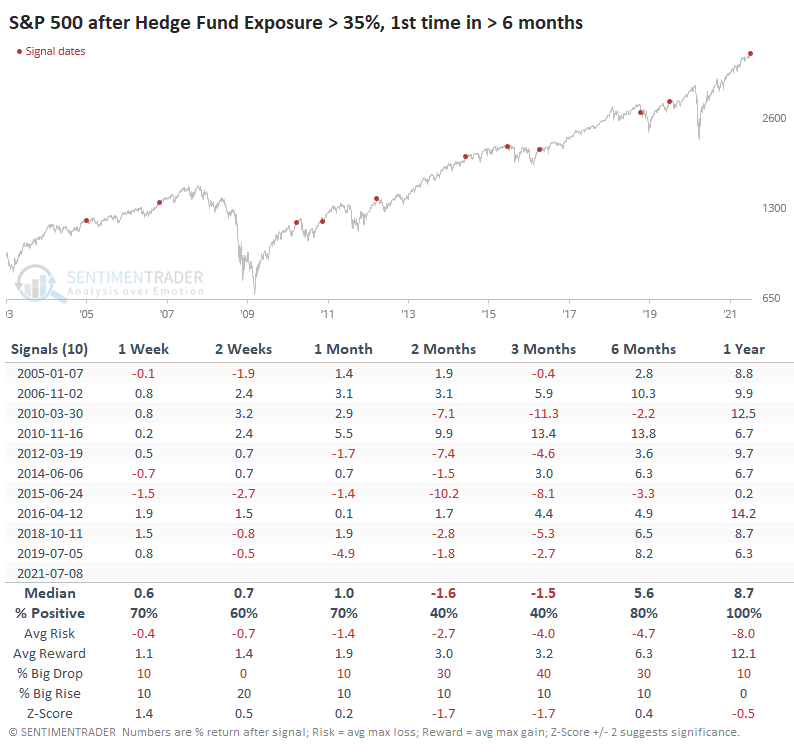

“After any day since 2003 when Exposure was below zero, the S&P 500 returned an annualized 15.2%, versus only 1.4% when Exposure was above 25% as it is now. If we look at the period after the first reading above 35% the medium-term returns were unimpressive.“ – Sentiment Trader

The point is that when professionals investors get “sucked” into performance chasing, it warrants being more “risk” aware.

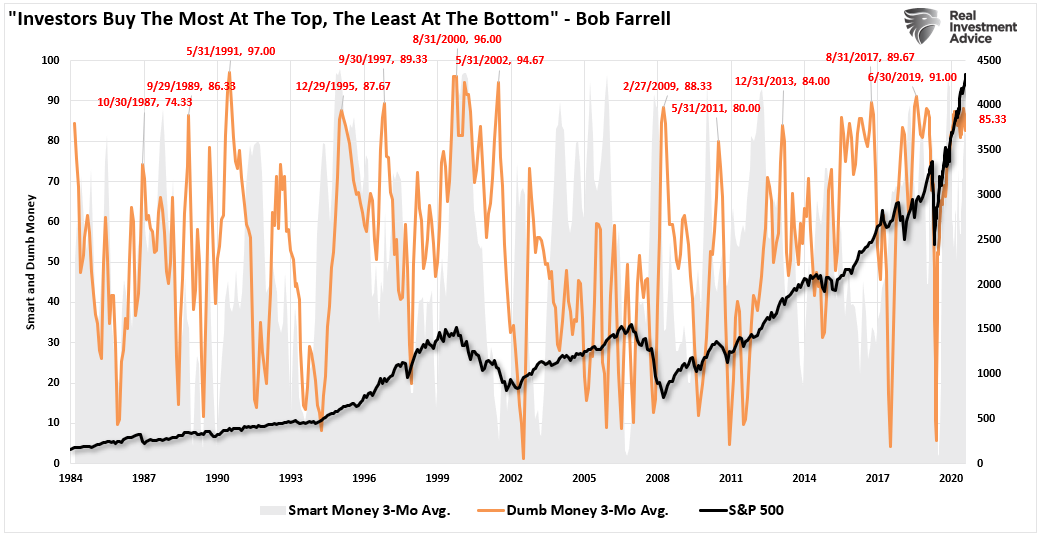

As Bob Farrell once quipped:

“Investors tend to buy the most at the top, and the least at the bottom.”

Smart Vs Dumb Money

None of this should be of any surprise. After more than a decade of monetary interventions, the psychology of QE is now thoroughly ingrained. The problem eventually is that with investors very “long” the market, there will be few “buyers” when it comes time to sell.

The chart below combines investor positioning from both retail and professional investors. While there is room for investors to get even more exposed to “risk,” such levels have historically not lasted long or ended well.

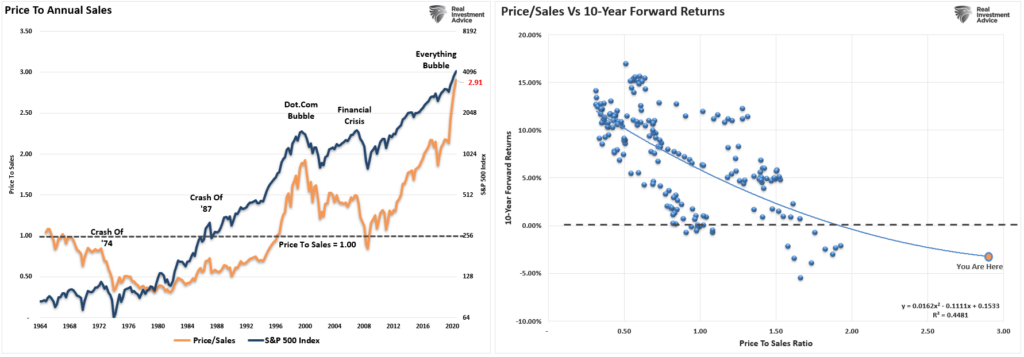

As discussed in “There Is No Way, This Doesn’t End Badly,” virtually every measure of fundamental analysis suggests the markets are expensive.

“10-year forward returns are below zero historically when the price-to-sales ratio is at 2x. There has never been a previous period with the ratio climbing to near 3x.”

However, in the short term, investors are trapped by the “fear of missing out.” While there is plenty of logic for sitting out of an overvalued, exuberant and stretched market, there is a consequence to “missing out.” While a bear market does indeed destroy capital, not participating in a bull market has an equal impact on ending results.

It’s a terrible choice.

Conclusion

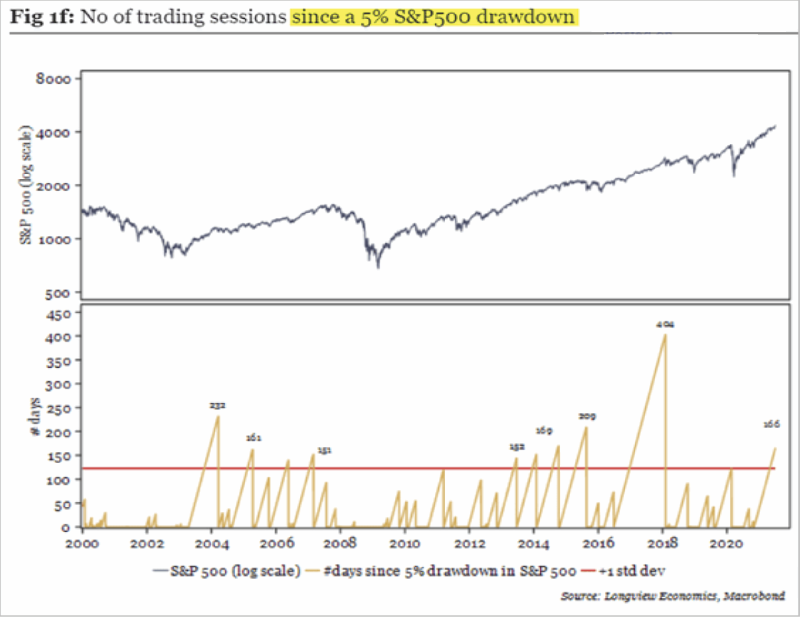

A correction is coming. I have no idea when or what will cause it.

However, the markets are currently in a very long advance without a 5% correction or more. So when it occurs, for whatever reason, it will “feel” worse than it is. That is due to the high level of complacency investors have developed in this market.

While we are only expecting a correction in the near term, you cannot dismiss a “real bear market” either.

It may not be today, next month, or even next year. But there is one truth in a market with all the signs of exuberance.

“Bull markets are built on optimism and die on exuberance.”

All bull markets die eventually. We never know the cause in advance. Ignoring history won’t make the damage any less catastrophic.

Historically, we find that when both valuations and prices have extended well beyond their intrinsic long-term trendlines, subsequent reversions BEYOND those trend lines have ensued.

Every Single Time.

Importantly, these reversions have wiped out a decade or more in investor gains. Think about this. If the next correction begins in 2022 and ONLY reverts to the long-term trendline, investors will reset portfolios to levels not seen since 2008.

A decade of gains will get wiped out.

Such tends to have a very negative impact on an individual’s retirement plans.

If you think that can’t happen, talk to anyone who was thinking about retiring in 2000 or 2008. I am sure they have an interesting story to share with you.