By Wolf Richter for WOLF STREET:

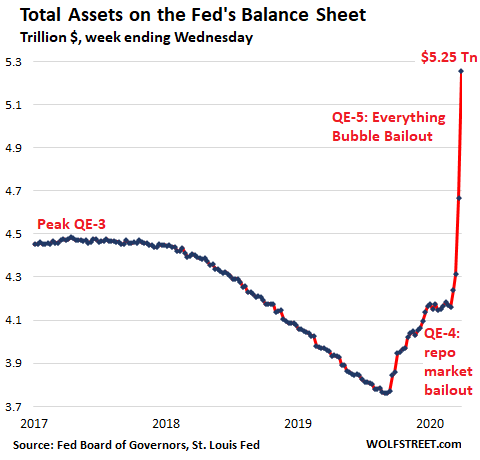

Total assets on the Fed’s weekly balance sheet, released this afternoon, spiked by $586 billion in one week, to $5.25 trillion. This doesn’t even include yet the bulk of the mortgage-backed securities (MBS) the Fed bought over the past two weeks because the Fed books them when its trades settle, and MBS trades take a while to settle. So they will show up later.

Over the past two weeks, total assets have ballooned by $942 billion – again not including the bulk of the MBS it bought during that time, which will be booked when they settle. Money creation at its finest:

If the Fed had sent that $942 billion it created over the past two weeks to the 130 million households in the US, each household would have received $7,250. But that didn’t happen. That was helicopter money for Wall Street.

Since mid-September when the Fed started bailing out the repo market that had blown out, total assets on the Fed’s balance sheet soared by $1.41 trillion. If the Fed had sent that $1.41 trillion to the 130 million households in the US, each household would have received $10,840. But that didn’t happen either. It was helicopter money for Wall Street.

Total assets on the Fed’s balance sheet are composed mostly of:

- Treasury securities, which include Treasury notes and bonds, short-term Treasury bills (T-bills), Treasury Inflation-Protected Security (TIPS), Floating-Rate Notes (FRN)

- Mortgage-backed securities (MBS)

- Repurchase agreements (repos), both overnight repos and term repos.

- A newly active line item, “Loans.”

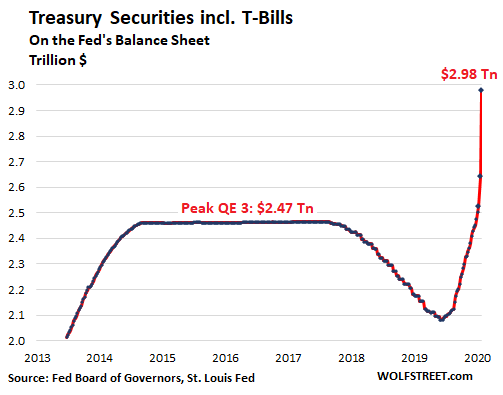

Treasury securities spike, but T-bills flatten

Over the past week, the Fed added $338 billion to its Treasury securities, buying all types and maturities. Since the repo market blowout in mid-September, the Fed has added $877 billion in Treasuries. The total balance spiked to $2.98 trillion:

The Fed is now purchasing Treasury securities of all kinds, and of all maturities. But within that group, T-bill balances have remained nearly flat over the past two weeks, after soaring at a rate of about $60 billion a month since the repo market blowout. In other words, the Fed is only replacing maturing T-bills with new T-bills and is now adding nearly exclusively longer maturities.

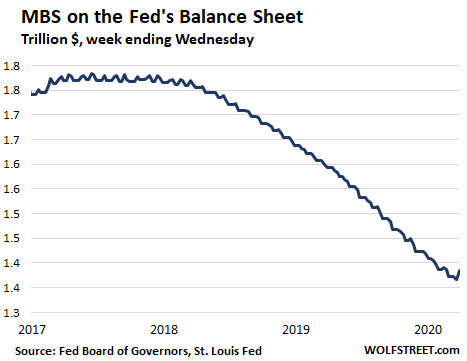

MBS are not yet fully reflected.

After reducing its balance of MBS by about $20 billion a month, every month all last year and into this year, the Fed announced that it would again pile into MBS, buying hand-over-fist to bail out the MBS market – both residential and commercial MBS – that has been imploding.

But it doesn’t show yet to the full extent. It takes a while for MBS transactions to settle. Since the Fed puts its new MBS on the balance sheet when the transaction settles, the purchases since this has restarted are barely starting to show up. Last week, the MBS balance fell to the lowest level since October 2013. On the balance sheet this week, MBS rose by $18 billion to $1.38 trillion, a barely visible uptick:

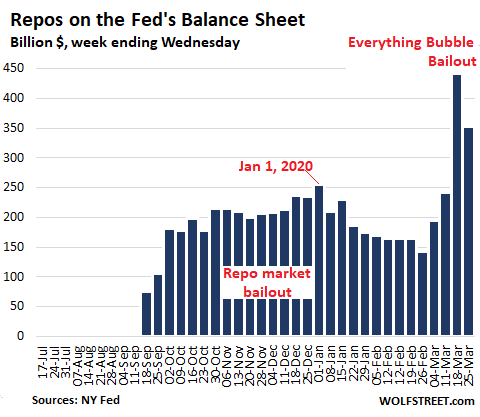

Repos fizzle.

The Fed is now offering overnight repos and term repos of combined over $1 trillion a day. In other words, nearly unlimited cash for the repo market. But there are few takers, and most of the repos are now by far undersubscribed. This has caused the repos on its balance sheet to tumble by $90 billion from the prior week, to $352 billion:

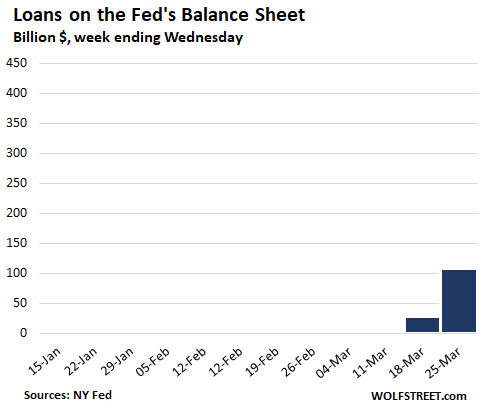

The newly hot bailout “Loans.”

During Financial Crisis 1, the Fed’s asset account “Loans” contained large balances. Those loans were eventually paid back to the Fed and the balances then dropped close to zero and remained there through two weeks ago. But last week, this account jumped from zero to $28 billion. And this week, it jumped to $109 billion. These are the amounts the Fed has lent out as part of its new bailout liquidity programs and direct lending programs. It even provides some details:

- Primary credit: $50.8 billion

- Primary Dealer Credit Facility: $27.7 billion

- Money Market Mutual Fund Liquidity Facility: $30.6 billion

This chart is on the same scale as the repo chart, with plenty of room for these loans to expand, as I expect they will since these programs just kicked off:

The Fed has become a full-bore record-breaking global market manipulator with its printing press to keep the Everything Bubble it had created over the past decade from imploding, or imploding further, or whatever. And it’s all helicopter money for Wall Street.