Authored by Jesse Colombo via RealInvestmentAdvice.com,

Last week, I wrote a detailed piece in which I explained that U.S. recession risk was rising quite rapidly and that the coming recession is likely to be far more severe than most economists expect because there are so many dangerous new bubbles inflating currently and because the global debt burden is much worse today than it was before the Great Recession. In the current piece, I will show more warning signs of the coming recession as well as discuss reliable recession indicators to keep an eye on as we get closer to the recession.

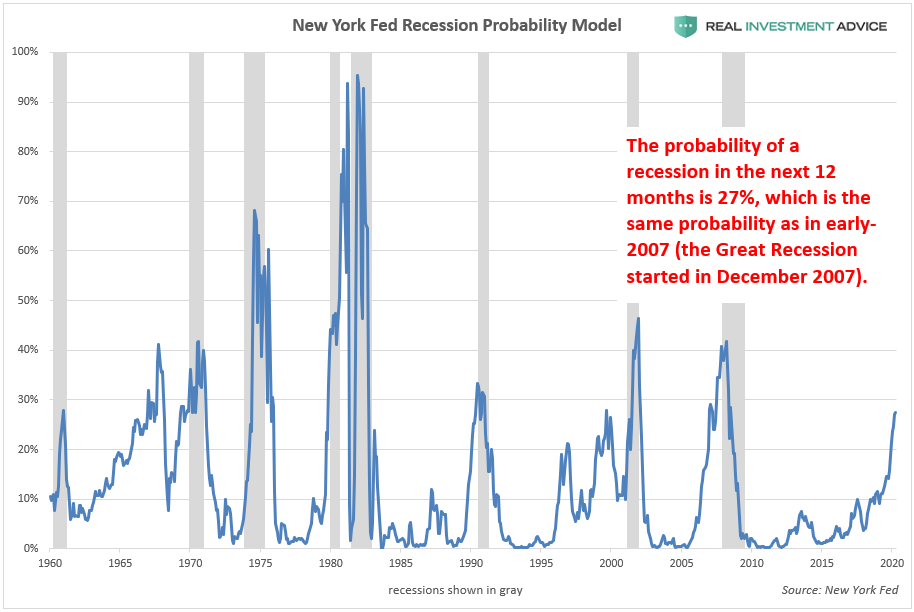

The first chart is of the New York Fed’s recession probability model, which is warning that there is a 27% probability of a U.S. recession in the next 12 months. The last time that recession odds were the same as they are now was in early-2007, which was shortly before the Great Recession officially started in December 2007. This recession indicator has underestimated the probability of recessions in the past several decades (it never rose higher that 42% in 2008, when we were already in a recession), so the probability of a U.S. recession in the next 12 months is likely even higher than 27%.

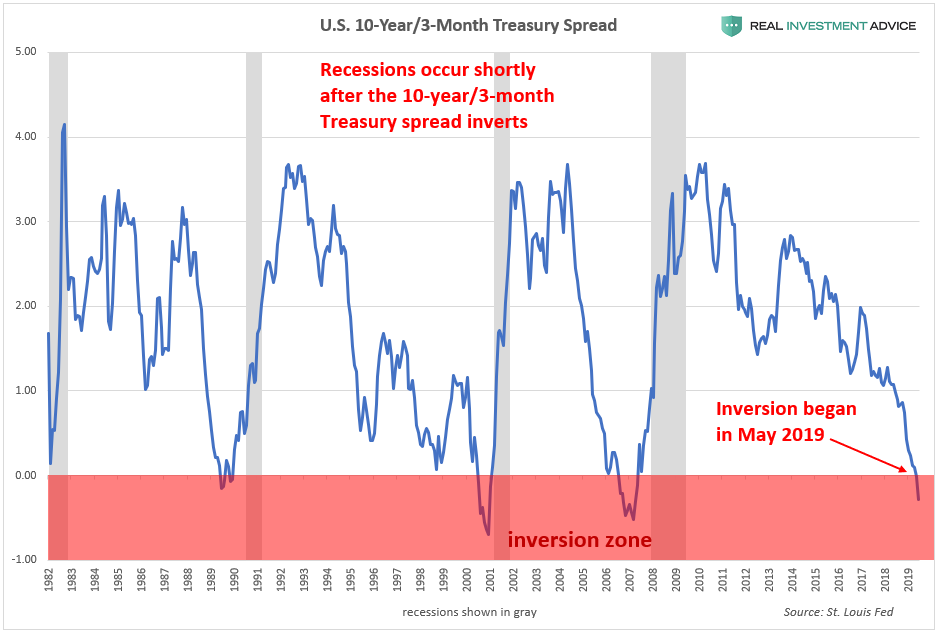

The New York Fed’s recession probability model is based on the 10-year and 3-month Treasury yield spread, which is the difference between 10-year and 3-month Treasury rates. In normal economic environments, the 10-year Treasury yield is higher than the 3-month Treasury yield. Right before a recession, however, this spread inverts as the 3-month Treasury yield actually becomes higher than the 10-year Treasury rate – this is known as an inverted yield curve. As the chart below shows, inverted yield curves have preceded all modern recessions. The 10-year and 3-month Treasury spread inverted in May, which started the recession countdown clock.

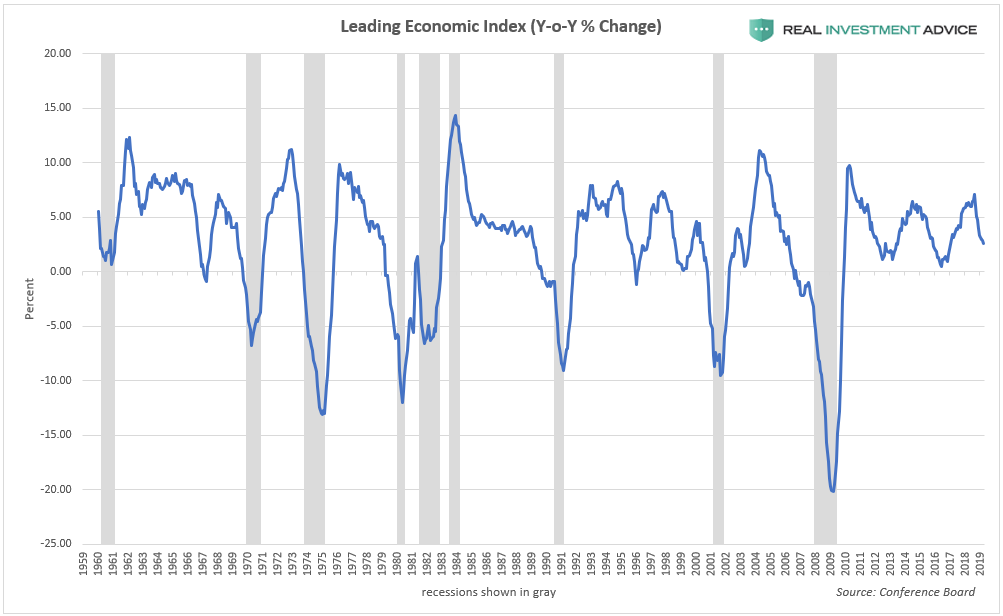

The Leading Economic Index (LEI), which is comprised of economic indicators that lead the overall economy, has been slowing down quite rapidly in recent months. When the year-over-year growth rate of this index drops into negative territory, recessions typically occur shortly after. While the current LEI slowdown hasn’t dipped into negative territory yet, anyone who is interested in monitoring the risk of a recession should keep an eye out for that scenario.

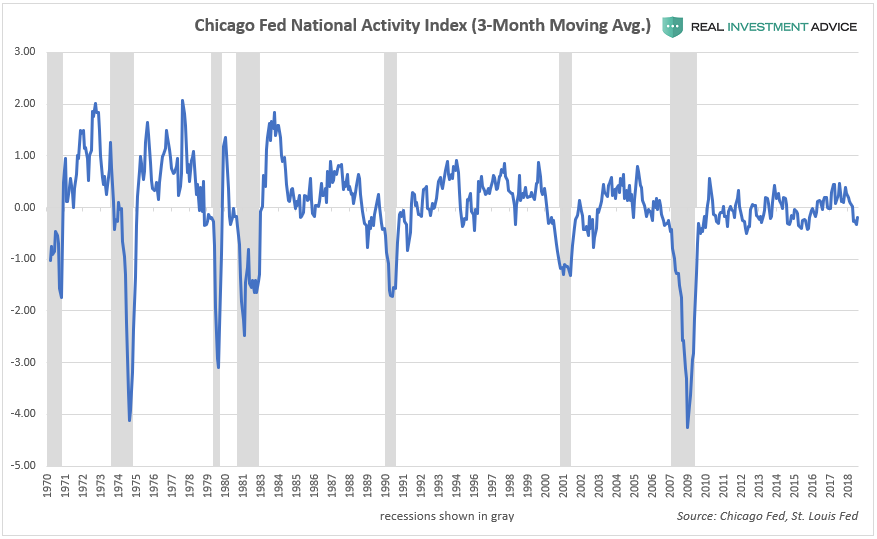

The Chicago Fed National Activity Index (CFNAI), which is comprised of 85 indicators of national economic activity, has been contracting in recent months. Sharp contractions of the CFNAI’s 3-month moving average typically signal imminent recessions. The CFNAI’s contraction isn’t quite at recessionary levels just yet, but if it drops it -0.5 or even lower, that will provide further confirmation that a recession is imminent.

In May, the U.S. Manufacturing Purchasing Managers’ Index fell to its lowest level since September 2009:

South Korean exports, which are seen as a barometer for the health of the global economy, have been falling in recent months:

It’s not surprising that South Korea’s exports are falling as global trade plummets:

Global Trade Collapsing To Depression Levels: https://t.co/t15uvC1fdZ @zerohedge $FXI $EWJ pic.twitter.com/zaLdsW0rs8

— Jesse Colombo (@TheBubbleBubble) May 15, 2019

Major appliance shipments collapsed 17% in April, which is a recession warning sign:

Look at this chart of major appliance shipments – collapsing 17% YoY in April – and tell me we aren’t heading into a recession. pic.twitter.com/dwKzt7u8SX

— David Rosenberg (@EconguyRosie) May 23, 2019

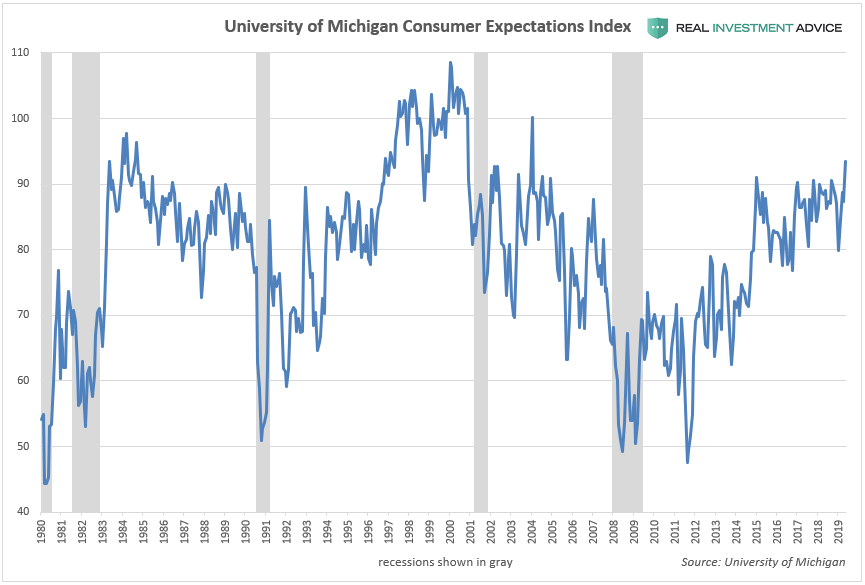

One popular indicator that is used to monitor recession risk, the University of Michigan Consumer Expectations Index, shows no sign of an imminent recession – quite the opposite, actually. Just beware when it starts to drop very sharply like it did before the last several recessions.

U.S. building permits and housing starts are popular economic indicators that are used to monitor recession risk. Right now, they are not warning of an imminent recession, thankfully. But if building permits and housing starts weaken significantly in the near future, it will provide further confirmation that a recession is near.

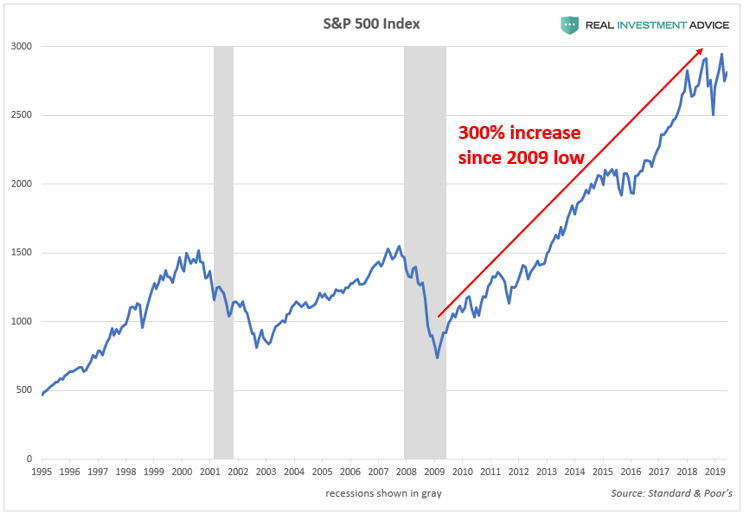

One of the most basic recession indicators is the stock market itself. When the stock market experiences a bear market (a decline of 20% or more), that is typically a sign that the economy is rolling over into a recession. For now, the stock market is not warning of a recession, but beware that it can unravel very quickly due to how inflated it currently is.

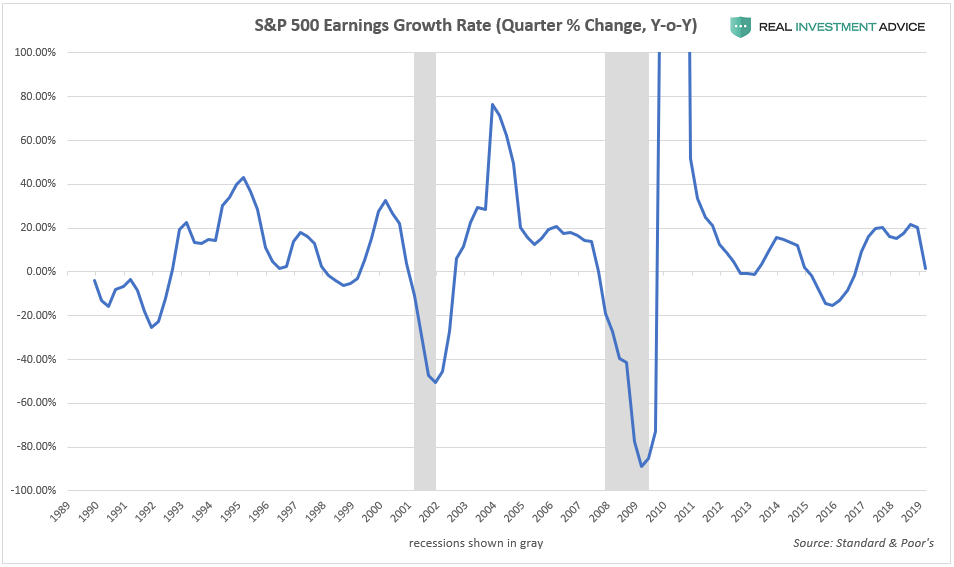

Corporate earnings growth is another valuable recession indicator to watch. Corporate earnings growth drops significantly and turns negative when the economy rolls over into a recession. After growing at a nearly 20% annualized rate in 2017 and 2018, Q1 2019 earnings growth hit a wall, growing only 1.5%. If corporate earnings start to contract in the next few quarters, that would confirm that a recession is near.

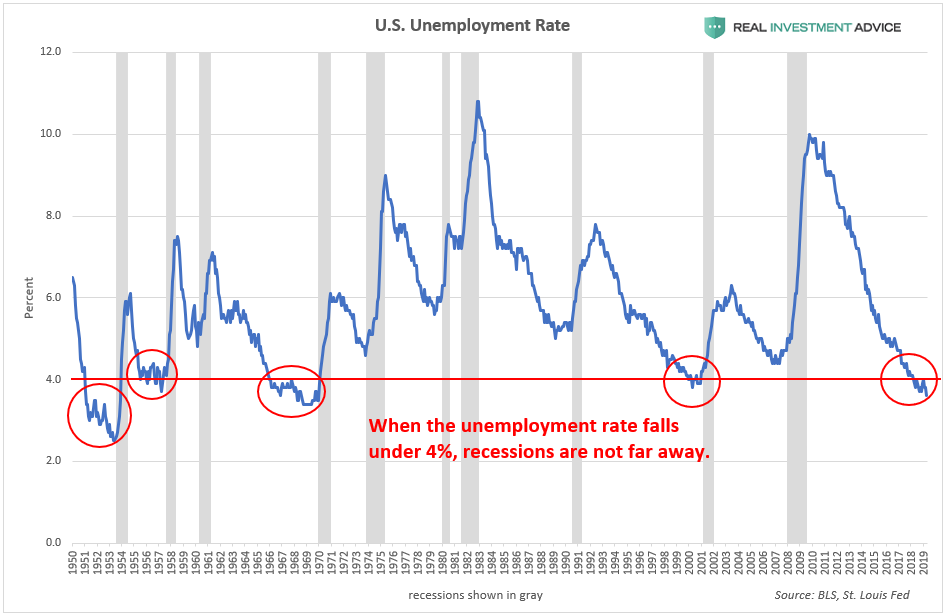

As I have explained in the past, sub-4% unemployment is a sign that the economic cycle is quite mature and that a recession is not far off. The U.S. unemployment rate has been under 4% since early-2018. When the unemployment rate abruptly increases from such low levels, that is a tell-tale sign that a recession has started.

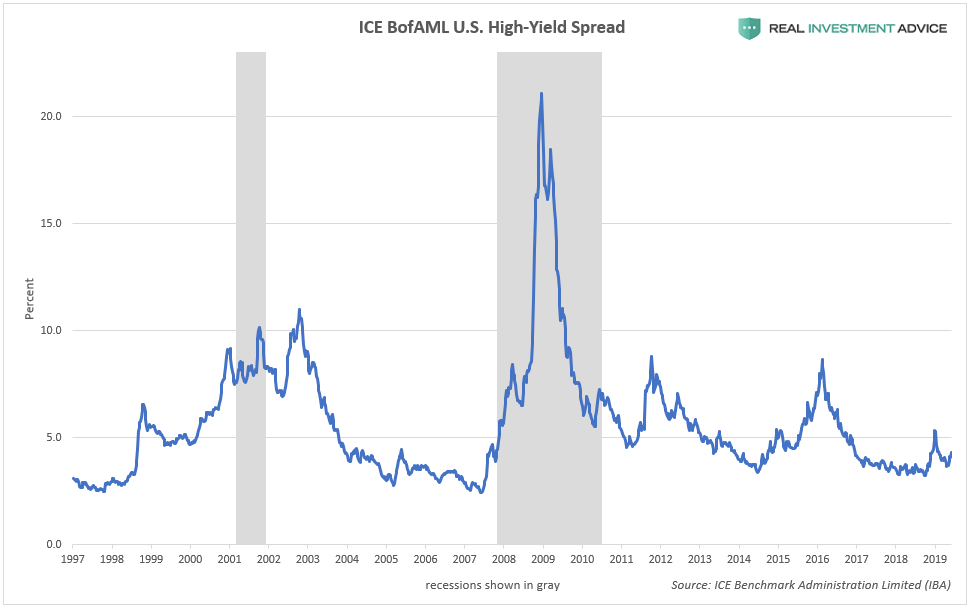

Though technically not a recession indicator, it is worth paying attention to the high-yield bond spread as a measure of how much stress there is in the credit market. The spread tends to increase leading up to and during recessions as investors jettison riskier high-yield bonds in favor of less risky Treasury bonds. Credit market stress is still low at the moment, but can change on a dime.

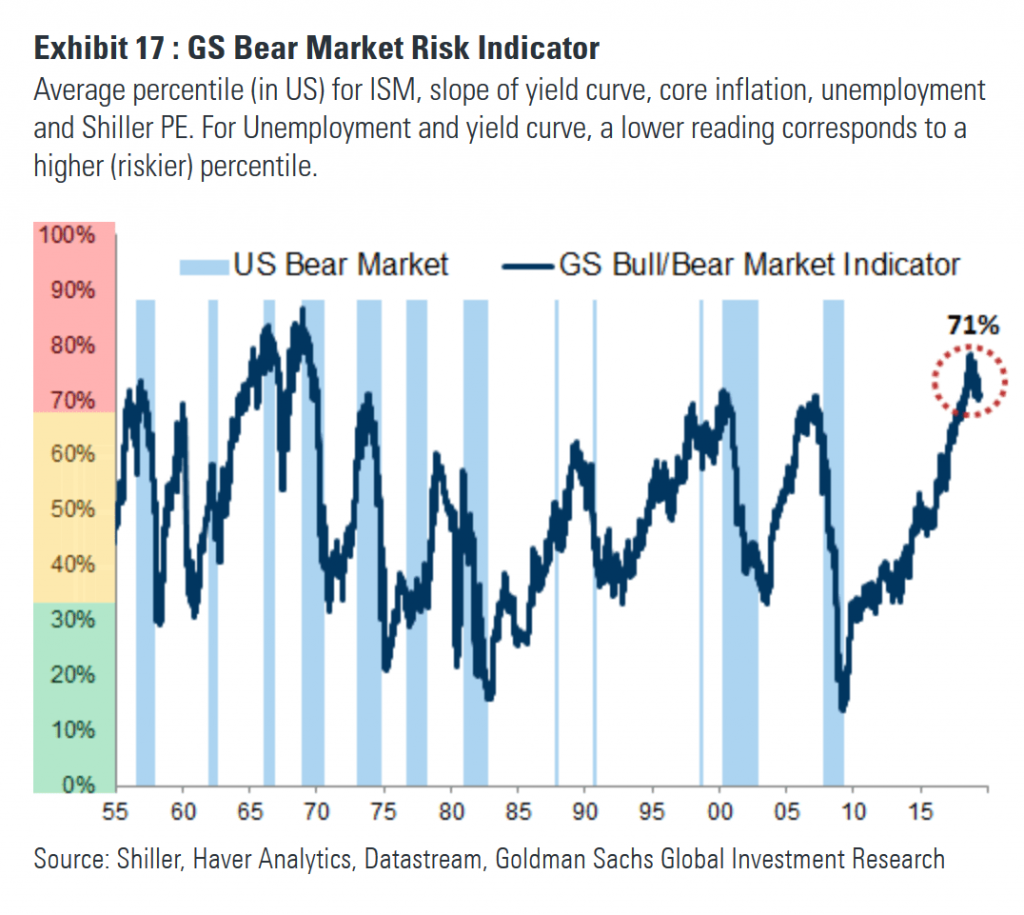

In the past year or so, Goldman Sachs’ Bear Market Risk Indicator has been has been at its highest level since the early-1970s:

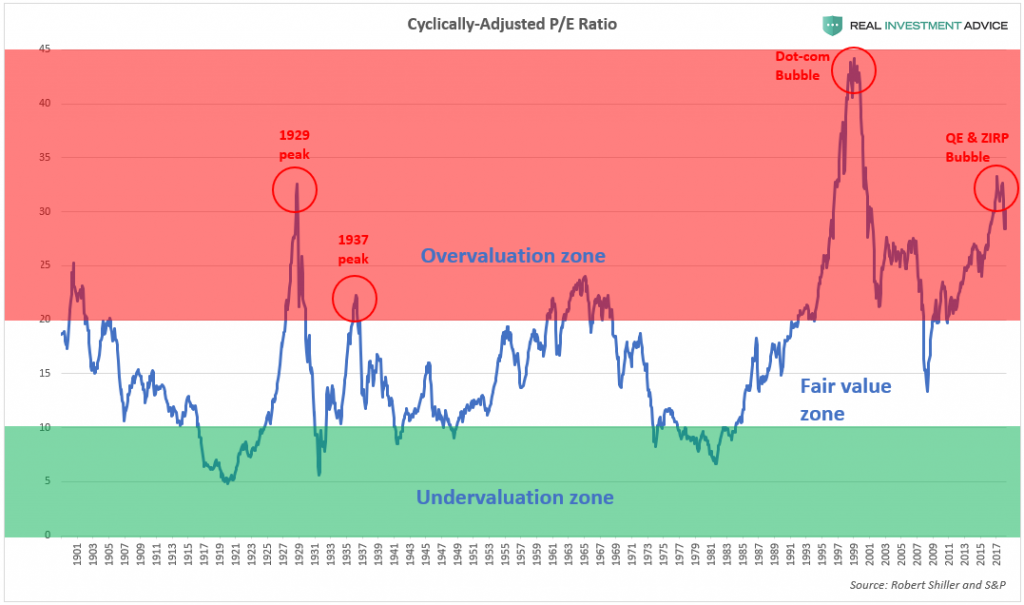

The high probability of a recession and bear market in the next year or so is very concerning because of how inflated the U.S. stock market currently is. The Fed’s aggressive inflation of the U.S. stock market in the past decade caused stocks to rise at a faster rate than their underlying earnings, which means that the market is extremely overvalued right now. Whenever the market becomes extremely overvalued, it’s just a matter of time before the market falls to a more reasonable valuation again. As the chart below shows, the U.S. stock market is nearly as overvalued as it was in 1929, right before the stock market crash that led to the Great Depression.

Another indicator that supports the “higher volatility ahead” thesis is the 10-year/2-year Treasury spread. When this spread is inverted, it leads the Volatility Index by approximately three years. If this historic relationship is still valid, we should prepare for much higher volatility over the next few years. A volatility surge of the magnitude suggested by the 10-year/2-year Treasury spread would likely be the result of a recession and a bursting of the massive asset bubble created by the Fed in the past decade.

While several reliable indicators are giving recession warnings and are worth paying attention to, the U.S. economy is still in the early stages of slowing down and rolling over into a recession. Even if the recession begins in a year or two, that is still too close for comfort considering the tremendous risks that have built up globally during the past decade of extremely stimulative monetary policies. As I have explained in last week’s piece, bubbles are forming in global debt, China, Hong Kong, Singapore, emerging markets, Canada, Australia, New Zealand, European real estate, the art market, U.S. stocks, U.S. household wealth, corporate debt, leveraged loans, U.S. student loans, U.S. auto loans, tech startups, shale energy, global skyscraper construction, U.S. commercial real estate, the U.S. restaurant industry, U.S. healthcare, and U.S. housing once again. I believe that the coming recession is going burst those bubbles, which may cause a crisis that is even worse than the 2008 Global Financial Crisis was.