For anyone inside or outside of the U.S., it goes without saying that things are indeed heating up in the land of the free.

President Trump faces an unprecedented second impeachment just days before the Biden administration is scheduled to take the keys to the White House in a transition of power that has been anything but orderly, as the recent march on the U.S. Capital made graphically clear.

Those seeking financial guidance, however, don’t need political commentary from market professionals or arm-chair sociologists.

Nevertheless, there are universal economic as well as historical paradigms (as to debt, rates, inflation fiat currencies etc.) and forces at play today that are both relevant and predictive to market action.

As someone with an office in Switzerland, I will therefore do my best to stay “neutral” in the left vs. right morass and focus instead on indicators and trends upon which most of us can agree.

Politics—Cynicism Regardless of Party

Toward that end, most would agree that politicians of all stripes, generations and zip codes have had one thing in common throughout history: To get or stay elected.

Sadly, the call to alleged “public service” has more often than not been a call to private ego as politicos of every flavor chase what Nietzsche aptly described as a “Will to Power.”

There are, of course, wonderful exceptions (pick your heroes) to this cynical rule, but many of us would now contend that our leaders, left, right, or center, have rather large egos and very small economic IQ’s.

As the famous French moralist, Francois de La Rochefoucauld observed centuries ago: “The highest offices are rarely, if ever, filled by the highest minds.”

Bad Decisions, Bad Politics, Keg-Party Markets

Ever since Nixon welched on the U.S. dollar in 1971 and took away this global reserve currency’s gold backing, currencies around the world have behaved like teenagers at a keg party without a chaperone.

That is, policy makers were free to party on a national credit card, the debt of which they either extended or serviced with printed, fiat currencies.

Such subsequent partying from DC to Brussels, London to Tokyo easily explains how and why global debt went from $5T in 1971 to $280T today.

In short, take away a gold standard or chaperone, and let the debt party rage.

Debt, of course, can be fun—for a while.

Fun Debt?

Markets use debt to leverage massive multiples and inflate otherwise profitless companies to nosebleed over-valuations.

Households use it pay for unaffordable cars, medical bills and educations.

Nations use it to pay for endless wars ($9T since 2003) or monetize otherwise unaffordable welfare programs (“unfunded liabilities” at $210+T) and broken pensions ($2T deficits) in drunken disregard for reality and a penchant to can-kick (i.e. ignore) growing public debt ($27.7 T and counting) by simply printing more dollars ($7.1T and counting) to cover a compounding bar tab.

Destructive Debt, Misreported Inflation

Of course, creating more fiat (i.e. fake) currencies to monetize all-too-real debt obligations is a fool’s errand. It kills currencies and destroys economic growth.

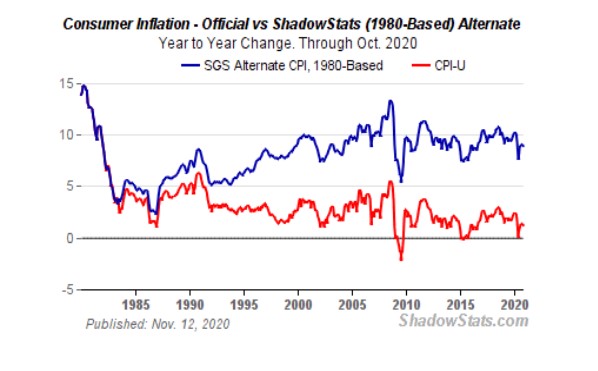

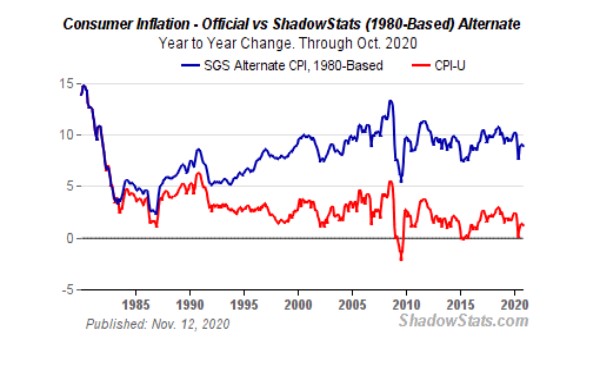

Oddly, modern policy makers and vote-seekers have convinced themselves and the world that inflation has been outlawed, when in fact, it has simply been misreported.

Using the CPI scale in place before the fiction writers at the Bureau of Labor Statistics joined forces with the academy-ward-winning actors at the Fed pretending to “target” (or now “allow”) higher than 2% inflation, it becomes clear that actual rather than reported inflation today is closer to 10%, not the open lie of 2% performed on stage each day at the FOMC.

Yet for those seeking the true inflationary effects of years and years of spitting fiat dollars out of a Fed money printer, just follow the money.

That is, dollars created by a Fed mouse click on Constitutional Ave (ah, the ironies…), goes to the Treasury, then to the Primary Dealers (i.e. those TBTF banks which failed in 08) and finally to the securities markets.

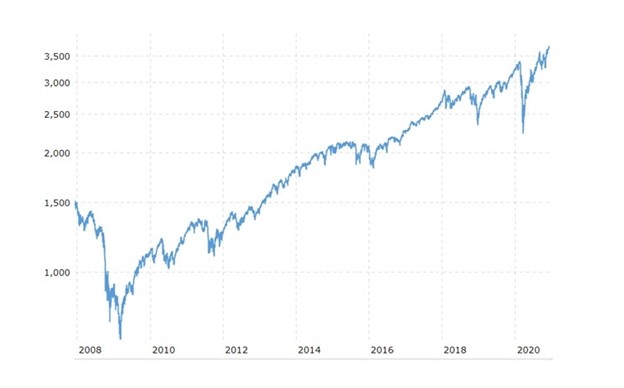

Thus, if you want to see where inflation shines brightest, just look at the grossly inflated S&P since 2008.

Rate Suppression—The Bloody Mary Approach to Delaying a Hangover

Then of course, there’s the esoteric and seemingly academic topic of interest rates…

Once again, our thespians at the Fed will pretend to be “considering rate adjustments.”

But with public debt soon passing $30T and climbing, we all know the Fed will never raise rates this generation, for the simple reason that they can’t afford to.

So long as the cost of debt (rates) are stappled to the floor of history, debt levels can equally surpass the record books of history.

But here’s the rub: What happens when rates go up?

The soothsayers behind MMT (Magical Monetary Theory) will tell you inflation and rates won’t go up, as the central banks won’t let them.

Like Santa Claus, that’s a very comforting thought.

Unfortunately, natural bond market forces rather than unnatural central bankers ultimately get the last say (and dark laugh) when it comes to rising rates.

With over $18T worth of negative-yielding bonds in circulation, it’s only a matter of time and headlines before someone yells “fire” in a crowded bond theater whose exit door (i.e. liquidity) is the size of a mouse hole.

With little to no yield for over-bought risk, bond holders will eventually become bond sellers, and when bonds sell off, their prices tank and hence their yields skyrocket.

Of course, when yields sky rocket, rates spike.

And when rates spike: Party over.

But for those who still trust the experts or believe that fancy buildings filled with fancy credentials will never allow a great nation (or union of nations) to financially fall, let us, as indicated above, agree on our history, even if we can’t agree on our politics.

My American friends think I’m too harsh on U.S. policies, so let me make it fair by poking some fun at another place dear to me…

France (Historical Template of Crazy)

Toward the end of the apparently now forgotten 18th century, the French, very much like the U.S. today, was looking pretty fancy on the surface but rotting from within due to social division and debts tied to extended wars, a prior market crash and rising deficits…

Sound familiar?

Well, let’s break it down into equally familiar phases.

Phase 1: A Big Problem in Search of a Miraculous Fix

1789 France was shining on the outside but broke on the inside.

In this French backdrop, as in 2008 America, “there was,” as the U.S. academic and historian, Andrew D. White wrote in 1912, “a general search for some short road to prosperity” (i.e. speedy calls for the printing of money) to give the ailing nation a little “stimulus.”

The French Finance Minister at the time was a fellow named Necker.

Unlike Mr. Bernanke of 2008, the Necker of 1789 recognized the short-term seduction yet long term (and fatal) dangers of printing an economy out of harm’s way.

Thus, Necker initially promised to fight off the seductive call of too much free money with classical oratory at the National Assembly, proclaiming the result “could only be disastrous,” as printing was nothing more than “a panacea…a way of securing resources without paying interest.”

Necker worried that it would be hard “to check the over-issue” of fiat money, and how “securely it creates a class of debauched speculators, the most injurious class that a nation can harbor.”

Sound familiar?

Today, the vast majority of American investors (from WeWork to Tesla) are speculators “all-in,” looking to make their fortunes in a stock market that is a frothy casino byevery historical metric.

But against these ultimately prophetic warnings, Marat, “friend of the people” and others seduced the herd/crowds with promises of “stimulating” the economy with just the right amount of French money printing and interest rate suppression.

Sound familiar? Remember Paulson? Geithner? Bernanke? They promised “just the right amount” of QE “accommodation.” Toward, the madness of crowds is back in full force.

And so, in 1790, France made its first real toe-dip into printing money (the equivalent then of our own “QE1”).

Of course, the free French money printing felt pretty good.

The French Treasury of 1790 was understandably relieved, old debts were paid with new, fake money, credit was revived and everyone was happy—much like the post 09 “V-shaped” markets in the U.S.

Phase 2: From “Emergency Measure” to Addiction

But the buzz of printed money began to slowly lose its impact, and within time, the French Assembly, wanted another “fix” of French money printing.

Sound familiar?

Despite original promises by Marat to temper the printing, the addiction became too tempting, and thus another round of money was printed (a veritable “QE2” of its day).

Not everyone felt this was wise.

Mirabeau, for example, spoke of the printed money as “a nursery of tyranny, corruption, and delusion; a veritable delirium…a loan to an armed robber” with inevitable dangers of inflation or a bursting debt bubble.

But soon, even Mirabeau got hooked on the drug of quick fixes. As Professor White later observed in 1912: “the current toward paper money had become irresistible.”

Of course, we have seen that same “irresistible” current from the Eccles building in DC as Fed policy evolved from a one-time 2008 “emergency measure” into a long-term drug dispenser of new money and low-rate debt for years to come—creating and extending an identical market bubble and class of “debauched speculators” as US markets reached for record highs.

Phase 3: The Good Times

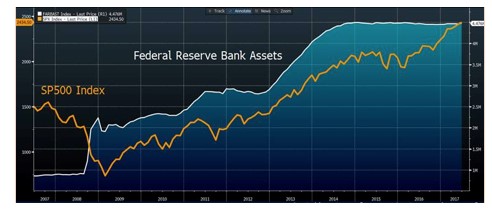

As for those “good times” even the most delirious bull today cannot deny the correlation of our market’s historical rise to the equally historical rise in our money supply (Fed Reserve Assets) and unprecedented debt levels.

Phase 4: Keep the Fantasy Going with Fantasy “Data”

The French lesson also contains the false comfort (i.e. lies) of experts whose bullish rhetoric kept the herd marching obliviously, even comfortably, toward cliffs.

The France of the 1790’s didn’t have Jim Cramer or the Private Wealth Management teams of Morgan Stanley et al, but they had even more talented orators at the assembly.

One, a certain Monsieur Gouy, (who today would have embraced MMT) suggested the French simply liquidate its entire national debt by printing a large amount of money and solve the nation’s pain, “by one single operation, grand, simple, magnificent.”

Sound familiar?

And these were the words of “elite” and “trusted” figures like Talleyrand and Mirabeau—certainly no less bright in IQ than anyone on FOX, CNBC or the FOMC.

But as Andrew White noted in 1912, smart people don’t necessarily understand monetary policy, and calling upon “experts” just because they show boldness and optimism “was like summoning a prize fighter to mend a watch.”

Phase 5: Minority Voices of Reason Ringing the Warning Bells

Then, as now, there were lone voices of dissent, even exasperation.

A fellow named Le Brun attacked the whole scheme in the Assembly, prophetically declaring “that the proposal, instead of relieving the nation, would wreck it.”

Other lone but sane wolves like Boislandry, Du Pont and de Nemours published pamphlets, predicting with haunting accuracy “that doubling the quantity of money simply increases prices, distorts values, alarms capital, diminishes legitimate enterprise and so decreases real rather than speculative demand that the only persons helped by it are the rich who have large debts to pay.”

Stated in 1790, but no less true in 2021.

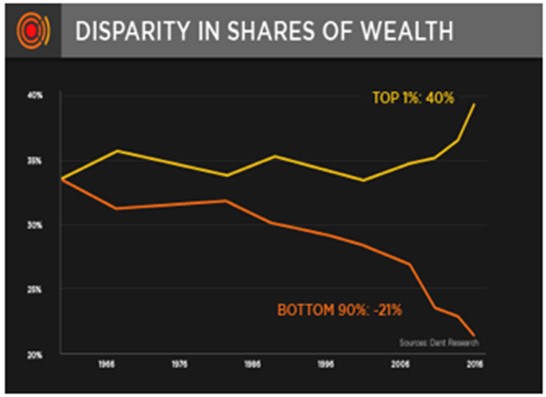

As this familiar graph reminds us, the only real beneficiaries of our totally drunken and fake “recovery” since 2009 have been the wealthy, not the rest of America.

France in the 1790’s, like the US (and EU, Japan…) today, was thus fully committed to a policy of debt and delusion.

White observed that, “the great majority of Frenchmen now became desperate optimists, declaring that printing and debt is prosperity…. The nation was becoming inebriated with false hope.”

Sound Familiar?

Such observations remind me of an equally “inebriated” S&P whose every dip is a buy, or a DOW hitting all-time highs and a bond-market which defies all laws of risk (or yield) because of the artificial safety-net of a Federal Reserve that has completely lost sight of market forces, courage, math, humility and alas: History.

Phase 6: Ignoring Reality—and Data

History warns us that the current party can’t last forever; our “safety nets” are full of weak-spots.

Now as then, “troublesome holes” had begun to appear. As White noted of that debt-soaked and market-topping France, “soon the markets were glutted and demand began to diminish.”

In other words, bubbles were approaching their apex. No one, however, wanted to face these facts.

Phase 7: The First Signs of “Uh-oh”

Without warning, French markets gyrated.

In the years after the easy money started to lose its punch, the markets began to see a series of sudden and steep falls.

Sound Familiar? Remember September of 2015? December of 2018? March of 2020?

Phase 8: Calm the Panic with More Fantasy

The French “solution” then? Simple: More money printing and more low rates…

Sound familiar? Think of Powell in March of 2019, or the unlimited QE of 2020.

Like the French of 1793, the FED went “full Monty” with the money printing.

This didn’t end well for the Frenchies.

As Professor White noted: “Out of this easy money came more speculating and gambling and luxury, and out of this, corruption and false economic data (supra) which grew as naturally as a fungus on a muck heap. It was first felt in business operations and markets, but soon began to be seen in the legislative body and in journalism.”

Sound familiar?

Today, market journalism is less a reporting of facts than it is a pulpit for the Sell-side bordering upon propaganda.

In the France of the 1790’s, like the US of today, financial feudalism created class division as speculators looked to get richer and the poor looked for pitch forks.

As markets reached new highs, investor cash-reserves sank to the basement. Savings vanished.

Sound familiar?

Today, investor cash levels are at all-time lows as our markets reach all-time highs.

Phase 9: Blood in the Streets…

But as for the mania in France then, and the current mania in US markets today, the ending feels eerily similar.

The French money printing experiment came crashing down in dramatic fashion.

We have no guillotine in 2021, but economic heads (and portfolios) will roll in one metaphorical way or another soon enough.

Don’t ask me when. No one really knows. No one.

But the tides are turning toward history…

The 1790’s looked like this in France:

2021 looks like this in the U.S.:

Something to at least think about, n’est-ce pas?