Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

Something is seriously wrong with this system.

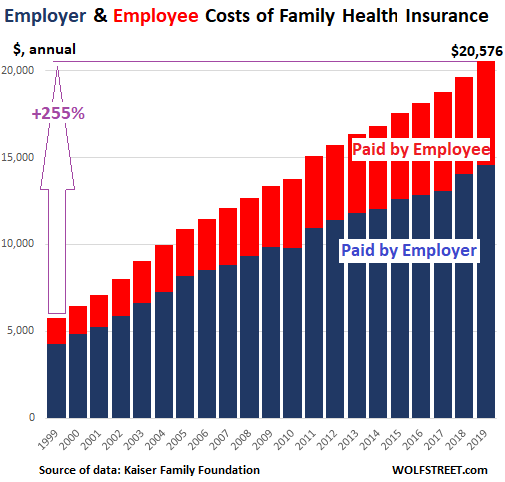

The annual cost of the average health insurance family plan through employers — employer and employee contributions combined – rose another 4.9% in 2019, to $20,576. This is up 255% from 20 years ago, having soared five times faster than the Consumer Price Index (+52%).

Employees paid about 29% of the premium for family coverage ($6,015 annually, red portion) and employers paid about 71% ($14,561 annually, blue portion). Over the past 20 years, the employee contribution has increased by 290%.

These are among the findings of the annual survey of over 2,000 companies, both small (3-199 employees) and large (200+ employees), including non-federal public employers, by the nonprofit Kaiser Family Foundation. Employers and employees both are groaning under the relentlessly ballooning weight of health insurance costs. And the numbers are large: 153 million Americans are covered by employer sponsored health insurance.

At companies with few lower-wage workers, the employee contribution for family coverage was on average $5,968 annually.

But at companies with many lower-wage workers, the employee portion for family coverage was $7,047 annually.

“The single biggest issue in health care for most Americans is that their health costs are growing much faster than their wages are,” KFF CEO Drew Altman said. “Costs are prohibitive when workers making $25,000 a year have to shell out $7,000 a year just for their share of family premiums.”

Many lower-wage workers cannot afford the contributions and forego the health insurance even if their companies offer it. As a result, at companies with many lower-wage workers, only 33% of the workers are covered by the employer’s health insurance, compared to 63% at the other companies.

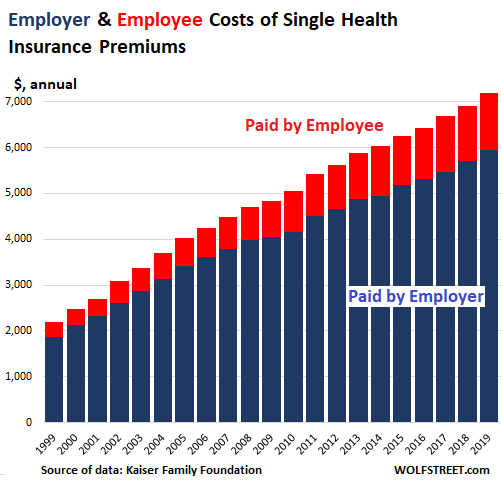

For single coverage of the employee only, the annual cost of the average health insurance premium — employer and employee contributions combined — rose 4.2% in 2019, to $7,188, with the employee paying 17% or $1,242 (up from 14% in 1999) and the employer paying 83% or $5,946 (down from 86% in 1999).

What the above chart shows is that over the past 20 years, the employee contribution to the average single plan has surged by 290%, compared to 52% for CPI. The employer portion has increased 200% over the same period.

Employers, who over the years have been straining to deal with the surge in these healthcare costs for their employees, have shifted ever more costs directly to the employee. This includes increasing the employee portion of the premium – see above. And it includes raising the deductibles (the portion of medical costs that the employee must pay before the insurance kicks in), copayments (fixed dollar amounts), and coinsurance (a percentage of the charge).

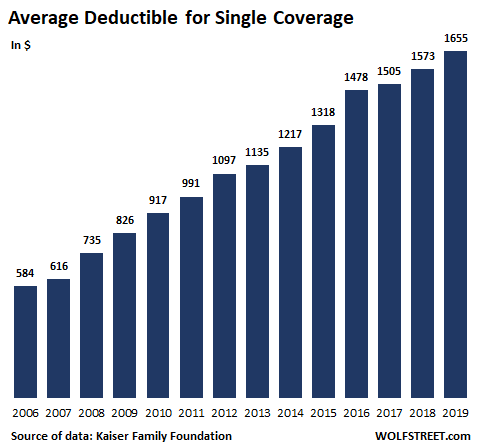

In terms of the deductible by itself, for employee-coverage only (single), the average annual amount in 2019 across all types of plans for employees who have a deductible rose by 5.2% to $1,655. Over the past 20 years, deductibles have increased by 183%:

Not all employees have a deductible, but the proportion has been growing: This year, 82% of employees face a deductible, up from 63% in 2009.

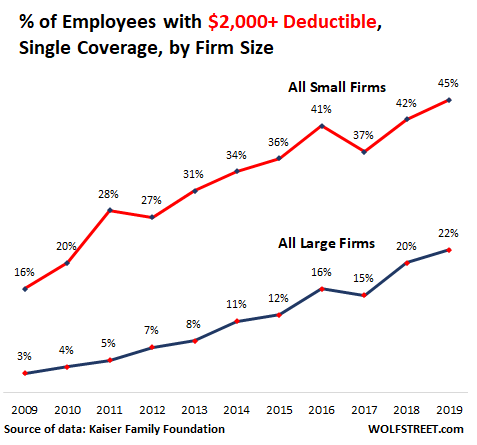

And the deductibles are getting big for a larger number of people: 45% of the employees at small companies have deductibles of at least $2,000, up from 16% in 2009; and at large firms, 22% have deductibles of over $2,000, up from 3% in 2009:

But there are big differences in the amounts of the deductibles by employer size: Employees at small firms (up to 199 employees) get hit with an average annual deductible of $2,271; employees of large firms (200+ employees) face an average deductible of $1,412.

Health care and insurance are large parts of the US economy. Effectively cracking down on the costs of the system would by definition crush the revenues of the companies in that system. And some of those companies would have to restructure and others would disappear.

But in terms of the overall economy, employees and employers would spend or invest the money that they saved on health care and insurance. For employers, it could mean money would be available to expand operations, hire more people, and pay higher wages.

The service sectors are Hopping. The #1 Biggie is Hopping the Fastest. It all adds to GDP! Read… The Financialization of the US Economy