via CBS NEWS:

The Fed’s interest rate hikes are doing more than hitting consumers in the credit cards. They’re also making it much more expensive for the U.S. to carry its debt load.

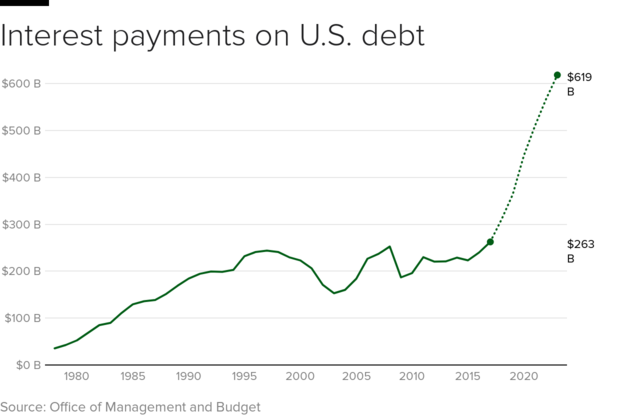

While they’re not currently a subject of President Trump’s Twitter outrage, America’s interest payments have become a point of concern for some on Wall Street. Those payments are projected to triple to more than $600 billion by 2023, reflecting rising interest rates as well as the exploding deficit. That figure approaches the amount the U.S. spends on national defense every year, and dwarfs what it spends on agriculture, Medicaid, income security and veterans’ programs, to name just a few.

“Rarely have deficits risen when the economy is booming. And never in modern U.S. history have deficits been so high outside of a war or recession (or their aftermath),” the Committee for a Responsible Federal Budget wrote in a recent blog post.

In the first full year of Donald Trump’s presidency, the federal deficit rose to its highest level in six years. Next year, it’s projected to rise even higher.

Is this historic abnormality a problem? Some economists think so. The Congressional Budget Office warned about the debt in its latest budget projection. “[H]igh and rising debt would have serious negative consequences for the budget and the nation,” the CBO wrote, adding that high debt makes a fiscal crisis more likely and leaves less room for lawmakers to change tax and spending policies to help solve a crisis.

Former Trump White House Economic Adviser Gary Cohn echoed these fears last week. “We have a huge debt and deficit problem,” Cohn said on “CBS This Morning,” while claiming the deficit was unrelated to the substantial tax cuts he orchestrated last year.

Embattled Fed chairman says he’ll meet face-to-face with president…

Debt Up $1.37 Trillion Since Last Year; $10,743 Per Household…