by upfina

It’s very common for investors to try to figure out if the current long expansion is near its end in which case a recession would start. The chart below is a bit more nuanced because it includes four categories.

Model of Economic Activity from @BofAML recently shifted into "sub-trend" regime for first time in more than a decade@tracyalloway @SoberLook pic.twitter.com/3w9Nirkvxs

— Liz Ann Sonders (@LizAnnSonders) October 18, 2019

In expansions, the economy is either in a boom or a soft patch. In recessions, the economy is either sub-trend or in a deep recession. The results aren’t as clean as we made it sound since sub-trend periods have occurred in and out of official NBER recessions. If the economy is sub-trend in an expansion, it’s very close to being in a recession. If the economy only gets as far as being sub-trend in a recession, the recession was mild.

This is Bank of America’s big data indicator. It’s nifty to notice how nearly all of this expansion has been a soft patch. This explains why the economy can last longer without falling into a recession. There was only a quick boom after the tax cut. This explains why it may have been viable to do a stimulus after the expansion was nine years old. Total growth wasn’t high. It’s notable that the economy is now sub-trend which is the first time that has occurred since the beginning of the last recession. The other two slowdowns didn’t count as sub-trend.

Obviously, this doesn’t mean growth is the weakest of the cycle. It’s not according to industrial production growth or consumption growth. It’s also not according to the weekly activity index. The September ECRI coincident index had 1.8% growth which is still above the trough of about 1% growth in 2016. The soft data is certainly terrible, but it might be too early to justify the economy being in the sub-trend category.

Global Recession Thought Of As Less Likely

The Bank of America survey below asked fund managers how likely it is that the global economy sees two quarters of negative GDP growth in the next year.

That's because a high number of them are expecting a recession within the next 12-months. pic.twitter.com/QUXn78tgbY

— Alex Barrow (@MacroOps) October 17, 2019

The net percentage had been the highest in years this summer, but managers have recently become slightly more optimistic. Many are projecting an increase in global growth in 2020 because of a boost in emerging markets. The IMF expects growth increasing to 3.4%, while Oxford Economics only sees growth improving from 2.9% to 3.1%. Now would be a great time to make a long bet because the 2020 picture is so uncertain. The problem is there is little evidence of growth rebounding. As support, the bulls only have the global monetary stimulus and India’s corporate tax cut.

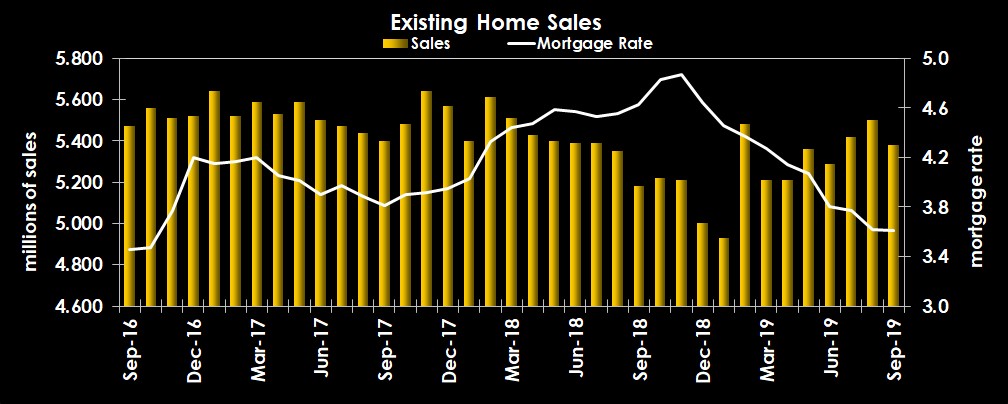

Existing Home Sales Fall Slightly

The September existing home sales report had a tough monthly comp and an easy yearly comp which explains why it had -2.2% monthly growth and 3.9% yearly growth. Yearly growth was the best since March 2017. This was the 3rd straight month of positive yearly growth. Specifically, sales fell from 5.5 million to 5.38 million as you can see from the chart below. This beat estimates for 5.44 million. You can look at this report positively or negatively. On the negative side, year to date sales are down 1.7%. On the positive side, the 3 month average of sales increased to 0.6% to 5.433 million which is its 4th straight gain and the highest since May 2018.

The existing housing market needs more inventory to sell more homes. That’s a big holdup as inventory was 1.83 million units which is down 2.7% from last year. Inventory was 4.1 months in September. That’s up from 4 months in August and down from 4.4 months last year. Home sellers will be motivated if prices rise. They rose 5.9% to $272,100. That’s the highest yearly growth since January 2018.

FHFA & MBA Applications

Even though existing home prices spiked, the FHFA home price index showed yearly price growth in August fell from 5% to 4.6%. The strongest area was the Mountain region which had 6.5% growth. The weakest were the Pacific and Middle Atlantic at 3.9% growth. The MBA Mortgage Applications report continued to show strength as the yearly growth in purchase applications was 6% in the week of October 18th. That’s down from 12% growth in the prior week.

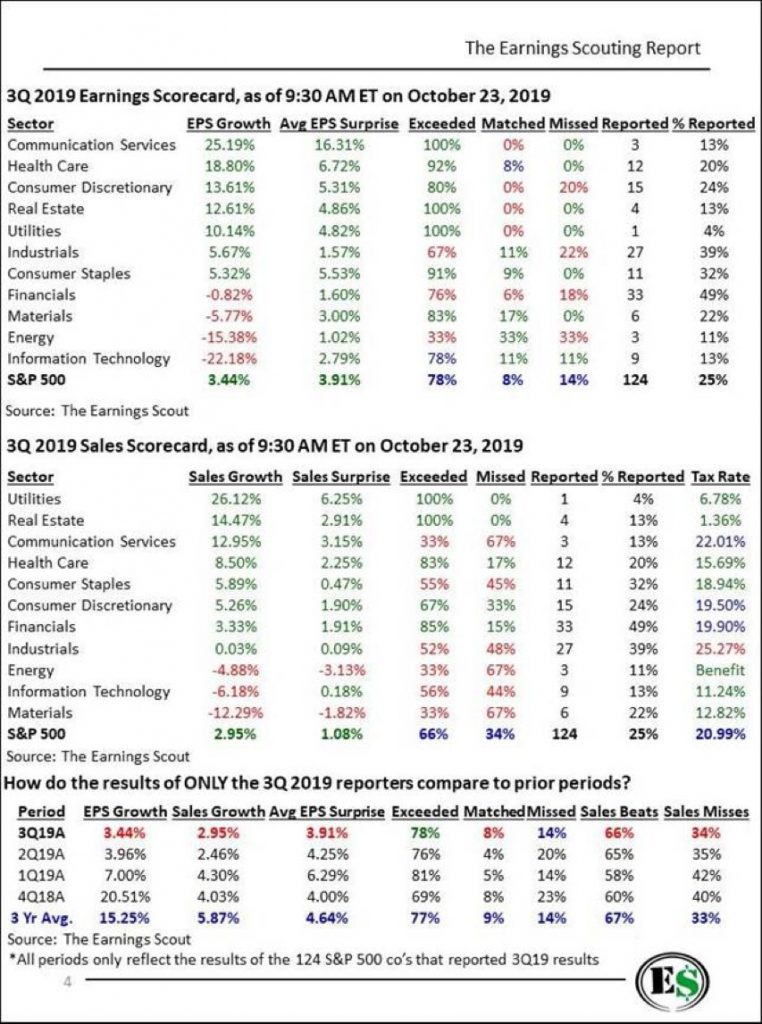

Below Average Earnings Season

Pick which way you want to look at earnings growth. With the first 124 S&P 500 firms reporting results, GAAP net income growth is -10.09%, GAAP EPS growth is -0.46%, non-GAAP net income growth is -2.09%, and non-GAAP EPS growth is 3.44%. EPS growth is greater than net income growth because of buybacks.

As you can see from the tables below, this has been a below average quarter.

The average surprise is 3.91% which is below the 3 year average of 4.64%. 66% of firms have beaten sales estimates which is 1% below average. Tech still has 87% of its firms left to report results which is bad news because it has had terrible growth thanks to the global cyclical slowdown. Weakness is being particularly felt by semiconductors.

Democratic Primary Update

As the front runner in the polls in September, Warren experienced more scrutiny. This ended her momentum in the polls. She recently lost 6 points in the latest national poll by the Economist. Biden now leads in the average of polls by 5.4 points. As you can see from the chart below, Warren went from having an over 50% chance of winning to just a 38% chance. She’s still the leader according to the betting market. Mayor Pete has recent gained momentum in the betting market as he’s at 17%. He is emerging as the moderate alternative to Biden. In the latest Iowa poll, he has 20% which is 2nd to Warren at 28% (Biden is at 12%).