I started trading stocks in the late 90s, it was an exciting time; the internet was coming of age, and investors, or rather day traders, were extremely excited about the riches of this new digital era. I was in my early 20s, and I had very limited investing knowledge at the time, nonetheless, I opened an online trading account and used half my college tuition money to speculate on internet stocks. A year later, my capital had multiplied by twenty folds! And notions of being a financial genius floated within my head. My remarkable success attracted the attention of many friends, even family friends, and at the ripe old age of 21, I was dispensing financial advice (mostly stock tips) to people double and triple my age. To those older than me, I became a sort of Sherpa to a new world where finance and technology intertwined into a new and exciting reality. Trading tech stocks during the technology boom was an intoxicating experience; popular names such as Netscape, AOL, Yahoo, JDS Uniphase, Cisco Systems, Juniper Networks, Ebay, Qualcomm and Amazon among others skyrocketed day after day to unbelievable highs. It seemed as if all one had to do to become rich was to open a brokerage account, and buy whatever tech stock was in vogue. Investment legends such as Warren Buffett were written off as out of touch for they did not comprehend the peculiarities of this new paradigm, where valuations, profitability, or even revenues were of little interest. Traditional valuation metrics were replaced by new measures such as eye balls and available bandwidth. In July 2000, Vinod Khosla at Kleiner Perkins Caufield & Byers, explained it so:

A lot of people look at the traditional measures for the economy and start scratching their heads about this long period of growth we’re enjoying. That’s because the traditional measures are industrial measures; they miss what’s really going on. The old econometric models take into account the cost of oil, but they totally ignore the cost of bandwidth. The old yardsticks don’t make sense any-more because what’s going on today is a fundamental change in the structure of our economy.

The old world, with its physical constrains seemed to have been replaced by a new virtual world, a terra nova of infinite growth possibilities. I felt fortunate to live at a time of such amazing optimism and change, a world where a kid my age could make more money in a day than his dad could earn in a year.

I don’t wish to spoil the end of this fairy-tale, but to my disappointment, the good times didn’t last, and the trees, in which I parked my capital, didn’t grow to the sky. After peaking at over 5000 points on March 10th 2000, the NASDAQ crashed into a brutal two-year bear market that took it all the way down to 1100 by October 2002, an 80% decline. Of course, the bursting of the technology bubble did not eliminate the internet, on the contrary, the internet continued to grow, and a host of new successful technology companies came to the scene in the ensuing two decades. Those who believed in this new world were vindicated, but few of us made real money out of it.

After losing my shirt in the technology crash, I developed a unique interest in investment bubbles, and read countless books on the subject. One of the books that marked me was Irrational Exuberance by Professor Robert Shiller; in the book, Shiller beautifully captures the essence of what fuels a speculative bubble:

“Irrational exuberance is the psychological basis of a speculative bubble. I define a speculative bubble as a situation in which news of price increases spurs investor enthusiasm, which spreads by psychological contagion from person to person, in the process amplifying stories that might justify the price increases and bringing in a larger and larger class of investors, who, despite doubts about the real value of an investment, are drawn to it partly through envy of others’ successes and partly through a gambler’s excitement.”

He then goes on to say,

“Errors of human judgment can infect even the smartest people, thanks to overconfidence, lack of attention to details, and excessive trust in the judgments of others, stemming from a failure to understand that others are not making independent judgments but are themselves following still others—the blind leading the blind.”

The process of price increases bringing on more price increases is a phenomena I have noticed in all the investment bubbles I have studied over the last twenty years. However, a price increase by itself is usually not sufficient to sustain a bubble, something more needs to be present, something that captures the imagination, and for that we can refer to another excellent book, ‘A Short History of Financial Euphoria’ by the economist John Galbraith. Galbraith cites ‘newness’ as one the key drivers to a financial euphoria:

All speculative episodes are driven by the thought of something new, exciting that catches the public imagination. It’s rich in imaginative prospects, but light on realistic prospects. Speculators take pride in a discovery or new innovation (financial or other), thinking they’re ahead of their time (much like early adopters of new tech). Eventually, others recognize it and pile in. Financial innovations are less innovation and more a twist on a past financial concept or product, unknown to a new generation of speculators. “The world of finance hails the invention of the wheel over and over again, often in a slightly more unstable version.”

Ironically, John Galbraith’s book was published in July 1994, merely a year before the famed Netscape’s IPO (August 1995) which marked the start of the 1990s technology boom. One wonders if the tech bubble would have formed if Galbraith’s book had been a best seller; the answer is probably not, and the reason can be found in the book itself as Galbraith argues this exact point:

Warnings of speculative euphoria are treated in the short run as an attack, as envy and lack of faith in the asset’s potential and the wisdom of the market. Participants defend their vested interest. Doubters are castrated as unimaginative or “too old” or “too out of touch” to understand the new paradigm driving values.

Whether it is the technology bubble in the 1990s, the Tulip bubble in the 1600s, the Mississippi bubble and South Sea Bubble in the 1700s, the stock market bubble of the 1920s, the real estate and stock market bubble in Japan the 1980s, or crypto-currencies bubble in the 2010s, such bubbles seems to share a number of common characteristics in the way they are inflated and around the time they are deflated. It is this bubble deflation, or bubble bursting phase that fascinates me the most, and is the subject of this article.

A recurring feature of a bursting investment bubble is the culmination of absurd statements and assertions by an otherwise seemingly reasonable individuals right around the parabolic top of such phenomena. The most famous example of these is the famed statement by the Yale economist Irving Fisher, who asserted in September 1929, a month before the catastrophic Dow Jones collapse, that “stock prices have reached what looks like a permanently high plateau.”

Many such absurd assertions and speculations can be found around the top of subsequent bubbles; those who can spot such ‘delusions’ if we can call them so, stand a decent chance of generating an above average return by positioning themselves for the approaching burst of the bubble in question. To further drive my point, I will briefly examine a series of historical bubbles as I make my way to the bubble referenced in the title of this article.

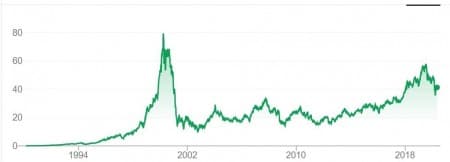

Cisco Systems – 1st Trillion Dollar company

In the late 1990s, Cisco Systems was a tech investors darling, with its routers and networking gear at the core of the internet and communication revolution, the company growth potential seemed infinite. By early 2000, Cisco Systems had become the most valuable company on earth with a valuation exceeding half a trillion dollar as its P/E ratio raced above 120. In other words, investors were paying $120 dollars for a claim on one dollar of Cisco’s earnings. In March 2000, Cisco’s excessive valuation didn’t stop Paul Weinstein, an analyst with Credit Suisse First Boston, from forecasting the company reaching a trillion dollars in market value within 24 to 36 months:

“We humbly submit that over the next two to three years, Cisco could be the first trillion-dollar market cap company–and don’t think they wouldn’t love it,” Mr. Weinstein wrote in his “strong buy” recommendation.

Weinstein was by no means alone, George Kelly at Morgan Stanley was equally buoyant (Wall Street, banks often piles up on the top of a bubble, in the hope of gaining favour with the ‘hot’ company, thus increasing the bank chance of securing a piece of any upcoming lucrative underwriting or investment banking business):

“One of the reasons investors value Cisco so highly right now is that, unlike Microsoft, Cisco doesn’t have the uncertainty of a Justice Department settlement–it’s a much cleaner situation,” Mr. Kelly said. “Second, Cisco has had a tremendous track record of continuous upside surprises. And Cisco is viewed as opening several new markets, the biggest of which is optical, which is expected to be an explosive market.”

Michael Neiberg, lead communications equipment analyst at Chase Hambrecht & Quist, chipped in as well:

“If you had picked a price point to sell [high] at anytime in the past 10 years, you would have been wrong,” he said. “They have such an impressive track record of growing … that the financial community isn’t thinking in terms of a multiple of what they’re earning this year, but what they will be earning three or four years down the line.”

Weeks after these rosy predictions were made, Cisco Systems went on to lose 87% of its value from its zenith in early 2000 to its nadir in late 2002:

It is important to note that no company had ever traded at a one trillion valuation at the time, hence, when analysts started making such hyperbolic predictions, right at the top of a parabolic stock price move, investors should have taken this as an ominous sign.

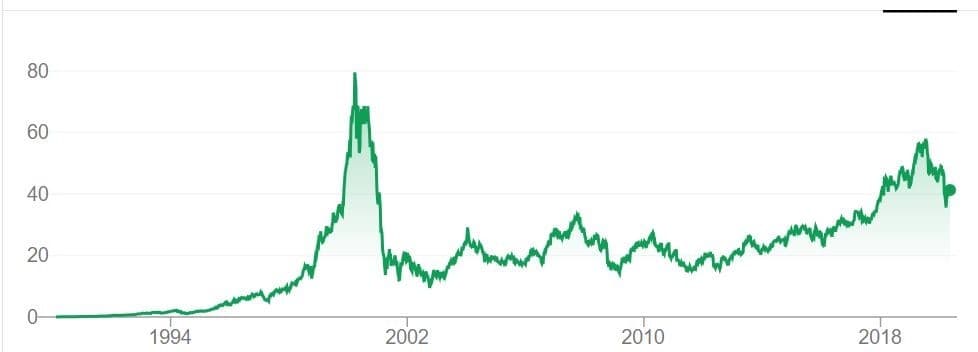

Qualcomm – $1000 a share

In early 1999, Qualcomm, the company beyond the CDMA wireless technology, traded at merely $25 a share, by the end of the year, analysts were projecting the stock to hit the nice round number of $1000 a share. The combination of wireless communication and the internet ignited a euphoric interest in Qualcomm, unlike other technology companies, Qualcomm was riding two secular growth trends: wireless and the internet. After the stock spent 1999 hitting a new high after another, the move accelerated towards the end of the year and culminated with a $1000 a share price target by Walter Piecyk at PaineWebber on December 29th 1999, from the Wall Street Journal:

Within minutes, Qualcomm shares were climbing so quickly that some traders complained they couldn’t keep up with the demand. They ended the day at $659, up $156, or 31%. The shares blew through their 52-week high of $528.50, and ended up 26-fold from their 52-week low of $25.3125 a share. The buzz surrounding the trading topped news bulletins on business television, market newswires and Internet investment chat rooms.

CNN Money, provided more color:

When an “it” stock really goes ballistic, conventional analysis becomes pointless. It’s all about momentum. Buy first, think later. bother with research now? This thing’s a rocket! As the momentum maniacs piled in after Piecyk’s call, Internet message boards were swamped with sophomoric posts, often fixated on hourly price fluctuations. On the day of Piecyk’s call, 3,034 posts poured into Yahoo!’s Qualcomm message board. Old-timers bemoaned the “RIP factor”–the low ratio of intelligent posts. Intoxicated with profits, one gleeful investor crowed, “I AM A GENIUS.” A fellow philosopher contributed this pithy and profound insight: “1000 yea baby yea.”

As was the case with Cisco Systems, the parabolic stock run, the frenzied trading, and Wall Street analysts hyper bullish price calls marked the top of the move. The stock spent the next two years losing 90% of its value, it took investors twenty years to see the stock reach and exceed its 1999 high:

The parabolic hype pattern we witnessed with Cisco Systems and Qualcomm has played out with countless other 1990s technology names, including the ones that survived the technology crash and went to on to exceed their old highs by a wide margin, names such as Apple and Amazon. But even in the case of these successful companies, it took between ten and twenty years for these stocks to reach their 1990s highs. It is possible for an investor to be right about the future of a company, and yet make no money on it for decades, if they have paid far too much for the stock during a speculative frenzy.

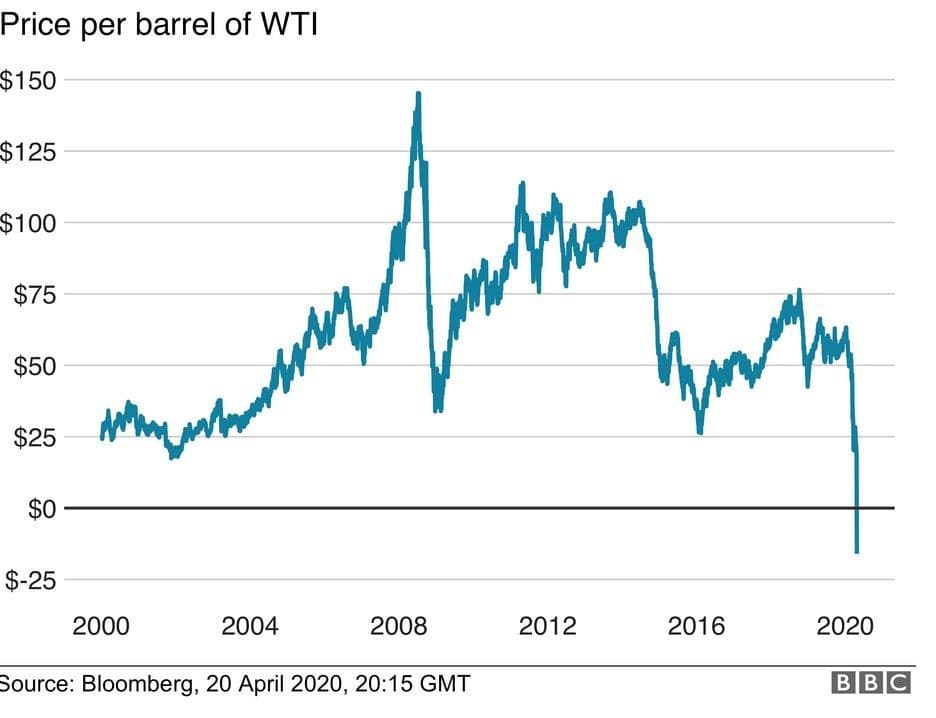

Oil – $200 a barrel

In January 2008, as the subprime crisis was brewing and Bear Sterns approached its demise, oil prices hit $100 a barrel for the first time in history. By May of the same year, as WTI exceed $120 a barrel, Goldman Sachs warned that oil was heading towards $200 a barrel:

Mr Murti said the energy crisis could be coming to a head as a lack of adequate supply growth was becoming apparent. He said: “The possibility of $150-$200 per barrel seems increasingly likely over the next six to 24 months.” He added that the spare capacity of the Organisation of the Petroleum Exporting Countries to cushion against unexpected supply shocks was very low.

The fact that the global economy was facing acute economic challenges in the summer of 2008, didn’t dent the oil price rally, nor did it lesson analysts enthusiasm for oil prices:

Oil recently hit US$135 a barrel, more than double where it was a year ago. And the once unimaginable prospect of oil at US$200 a barrel is gaining currency among the world’s most respected oil watchers. Jeff Rubin, chief economist with CIBC World Markets, predicts oil will rocket to that level by 2012. Goldman Sachs figures we’ll get there even sooner. Other analysts, meanwhile, have begun to float more startling figures, of oil at US$250, even US$300 a barrel.

As you can imagine, the parabolic move in oil, and the increasingly bullish analysts rhetoric, marked the top for oil prices. The WTI contract topped at $147 a barrel in July 2008 before collapsing all the way to the $30s by December. Twelve years later, oil prices remain nowhere close to the egregious summer 2008 analysts price calls. Peak oil, the idea that the world was running of oil was one of the factors that drove oil prices ever higher at the time. Many of those forecasting higher prices in the summer of 2008 failed to account for the impact of technology in unlocking new oil reserves, nor did they adjust for a potential weakness in demand as prices soared and the global economy weakened. Parabolic price moves tend to numb critical thinking at the moment it is needed most.

Bitcoin – $1 million a coin

During the 2010s, a digital currency of an unknown origin named Bitcoin, grew from an obscure financial innovation into a worldwide phenomena. As the crypto currency increased in value, it attracted hoards of investors, speculators and gamblers from the four corners of the globe. In a sense, Bitcoin was the first global bubble, a bubble that knew no creed, color, or ethnicity. As Bitcoin raced towards its all time high of $17000-$19000 a coin (depending on the exchange) and reached roughly $300 billion in total value in December 2017, predictions around the digital currency future value became practically surreal:

Former hedge fund manager James Altucher thinks bitcoin will reach $1 million in three years … “There’s only going to be 21 million bitcoins minted ever in history. That’s also going to drive demand,” Altucher said.

Others, went even further:

Bitcoin has a value potential of at least $90 trillion … The calculation is $90 trillion divided by 21 million, which is approximately $4.3 million per bitcoin.

Bitcoin promoters threw the kitchen sink to justify their increasingly inflated price projections: they claimed Bitcoin would re-make the global financial system, replace banks, credit cards, cash, it would create new business models and dominate payment systems, dethrone central banks, and transfer wealth into the hands of the masses. The fact that only a limited number of Bitcoins could be mined or ever be created further added to the investment proposal scarcity value. (The fact that other digital currencies could be created was conveniently sidestepped by those espousing ever higher Bitcoin price targets.)

Once more the same pattern repeats itself: parabolic price move, wild price projections emerge, and a collapse ensues. After hitting its all-time high in December 2017, the digital currency lost 80% of its value within 12 months. Although, Bitcoin has rebounded since, it is still trading 50% below its previous peak.

Tesla – $7000 a share

Tesla, with its popular electric cars and its controversial CEO, Elon Musk, has captured the imagination of many investors. Despite 17 years of loses, many broken promises, and a litany of high-profile skeptics, a bidding frenzy rocketed the stock from $250 a share in late 2019 to over $900 a share by February 2020, at which point, the company market value exceeded the market value of General Motors, Ford and Fiat Chrysler combined. As we have seen with previous bubbles, the parabolic move in the stock price only encouraged the bubble proponents into making wilder, crazier, future price projections: Catherine Wood, a money manger at Ark Invest a renowned Tesla bull, issued a whopping $7000 a price target on Tesla days before its $917 a share peak:

“Our confidence level that this stock is heading for $7,000 over the next five years is very high,” Wood, the founder and CEO of Ark Investment Management, said on “Fast Money.”

Around the same time, Toni Sacconaghi at Bernstein, while acknowledging that Tesla valuation had become disconnected from reality, attempted to justify the unjustifiable:

Using traditional auto valuations and discounted cash flows, he said it would be difficult to justify the current share price, which would suggest Tesla will eventually become bigger and more profitable than Volkswagen. However, he acknowledged that investor perceptions have changed, with Tesla becoming the “ultimate ‘possibility’ stock.”

Nigam Arora, at Marketwatch.com, captured the investors’ mood around Tesla in an article entitled: A perfect combination for Tesla’s stock gains — future fantasies, short selling and FOMO:

Since it is imagination that investors are trading on, there are no restrictions and no constraints. Isn’t it, say, a matter of time before Tesla makes millions of cars a year? Many investors have conviction that it will. Aren’t there too many variables to jump from half a million to many millions? No problem, just add perfect foresight to the conviction Let us not forget about advances in autonomous cars by Tesla, robotaxis, solar roofs and batteries. Could flying taxis from Tesla become our favorite mode of transportation? The sky’s the limit. Tesla is so far ahead that nobody else can possibly catch up. It is a matter of time before everything around us is Tesla, or so the story goes.

A month after closing above $900 a share, Tesla shares collapsed to $351, before rebounding to $819 a share. Today, the stock market capitalization is worth more than the combined market value of: GM, Ford, Fiat Chrysler, Uber, Lyft and Ferrari. Tesla embodies many of the same characteristics of the aforementioned bubbles: a new technology, a parabolic stock price move, a diet of hyperbolic price forecasts, and a valuation that defy all logic and reality. If Tesla’s stock price follows the same pattern of its bubbly predecessors, the stock price has much further to go on the downside.

Conclusion

At the parabolic top of every financial bubble, thrilled investors lose their tether to reality, and as the price of the speculative instrument rallies ever higher, investors’ expectations for additional price appreciation inflate ever more. Whether its Cisco Systems at a trillion-dollar market value, Qualcomm at $1000 a share, Oil at $200 a barrel, Bitcoin at a million dollar a piece, or Tesla at $7000 a share, these far fetched price fantasies are the fuel with which bubbles, and their beneficiaries, attempt to sustain themselves.

To the chagrin of the bubble chasers, history is categorical in this regard, the combination of a parabolic price move, a hype narrative, and the proliferation of wild price projections, is highly indicative of a topping bubble and an impending price collapse. Of course, Tesla shareholders will dismiss this article as irrelevant since history count little in the eyes of those who believe their company to be at the forefront of a new transportation and business paradigm. John Galbraith puts it best:

“There can be few fields of human endeavor in which history counts for so little as in the world of finance. Past experience, to the extent that it is part of memory at all, is dismissed as the primitive refuge of those who do not have the insight to appreciate the incredible wonders of the present”

By Nawar Alsaadi for Oilprice.com