From J Taylor’s Gold, Energy and Tech Stocks newsletter:

I am indebted to former Federal Reserve economist Lacy Hunt for his insights in a recent interview he did with Adam Taggart that I used in my presentation on March 10 at the Metals Investor Forum. Lacy explained that massive federal debt taken on by policymakers not only cannot stimulate growth, as the Keynesians believed, but in fact beyond a certain point actually starts to result in significantly slower growth than would otherwise be the case. In his talk, Lacy provided several academic studies that documented that truth. What it means is that the United States and the Western world in general are facing a dramatic decline in our living standards. The simple explanation is that because we enjoyed so much consumption in the past through debt financing, we will be paying for it in years to come by a dramatic decline in future consumption.

In the interview with Adam Taggart, Lacy was asked if there is any way he could envision a serious inflationary problem. His response was that the only way that could happen is if the Fed became the spender of last resort rather than the lender of last resort. He explained that he didn’t think the Fed would become the spender of last resort this year or as long as Jerome Powell remained as Federal Reserve chairman. But if the Fed did change to the role of spender of last resort rather than the lender of last resort, Gresham’s law would apply (bad money chases out good money) and America would turn into a banana republic with 95% of households becoming economically devastated. Biden has candidates lined up as possible successors to Chairman Powell—people who would have the Fed be lender of last resort through Modern Monetary Theory (MMT).

In other words, it would mean an end of an “Independent” Federal Reserve.

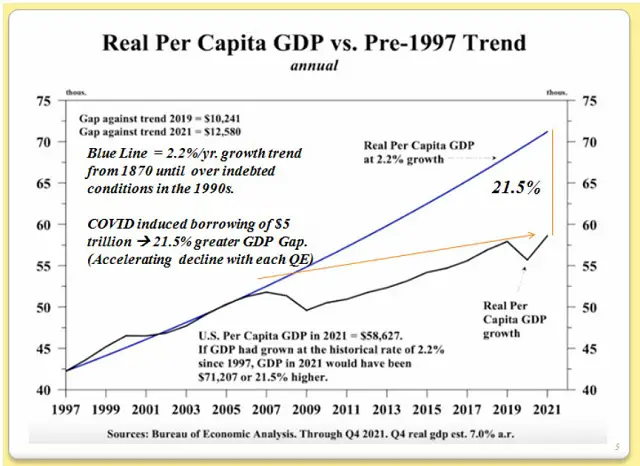

The blue line in the following graphic represents America’s GDP Trend line growth of 2.2% per year dating back to 1870. But with massive money printing then QE in 2008, real GDP started slowing dramatically, as the black line illustrates. Then, as the Fed printed massive amounts of money into the system to keep rates low (because the system couldn’t handle higher rates), funded by Federal borrowings, by the time COVID related policy rolled around, real GDP (black line) fell 21.5% below trend GDP. Instead of per capita GDP being $71,207 it was only $58,627 GDP in 2021. What the various academic studies revealed by Lacy Hunt demonstrated was that after debt/GDP rises beyond 60%, additional debt-funded expenditures by government start to lead to declining GDP in a non-linear manner. And once debt/GDP rises above 90% for at least five years, economic growth slows very dramatically. Their study covered 26 historical major public debt overhang episodes in 22 advanced economies that had debt/GDP ratios greater than 90%. The conclusion of the Gold study was: (1) The economic growth rate is reduced by slightly more than one-third, and (2) When debt/GDP is greater than 90%, rates are not likely to rise, even when tighter monetary and fiscal conditions are implemented.

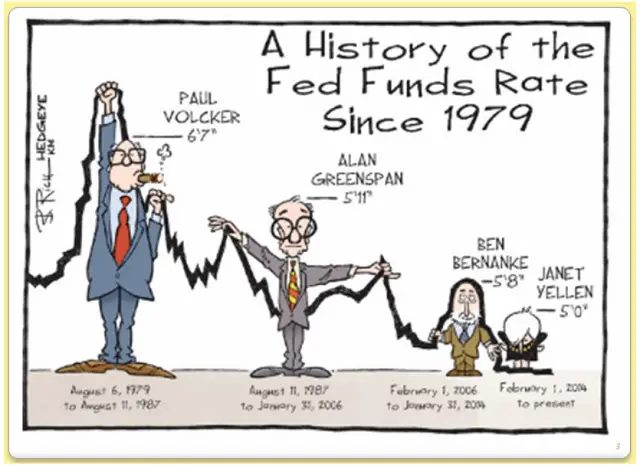

Observing the interest rate picture in the U.S., my assumption is that interest rates don’t rise much under high debt/GDP environments because the highly indebted economies simply can’t survive higher rates. In each of the credit cycles since Paul Volcker raised Fed funds to double digits, we have seen lower highs and lower lows. But now that interest rates have hit zero, perhaps there is nothing left to do but to create a new currency regime.

To give you a sense of how impotent Keynesian stimulus is once you hit higher levels of debt, note that during the 1870-to-1997 timeframe, $1 of new debt would generate $0.62 of additional GDP. Income generated from an additional dollar of debt financing has declined as debt/GDP rose from $0.62 to a low of $0.25 in 2021.

Why do diminishing returns take place as debt/GDP rises and in a nonlinear manner? One reason is that highly indebted countries simply have to allocate a sizable amount of income to pay principal and interest. The higher the debt, the less money available to spend on purchase of goods and services, so GDP declines. Secondly, with lower rates that come with high levels of debt, lenders are not able to price risks into the interest they charge and so lending into the real economy declines, thus negating the rise of industry that creates higher-paying jobs. When banks don’t lend, the money multiplier declines dramatically and when people don’t spend, the velocity of money declines.

So Lacy Hunt makes a very good argument for deflation, assuming that the Fed doesn’t adopt MMT and become the spender of last resort instead of the lender of last resort. If there were reason to believe the Fed wouldn’t cave to political pressure from the ruling elite to print money whenever the next crisis hits, so that they would suffer some pain along with the folks Hillary Clinton labeled as “deplorable” then I might think Lacy Hunt’s deflationary depression will be the more preferable market cleansing mechanism. However, now that there will likely be massive price increases resulting from all manner of sanctions against Russia and all manner of supply chain disruptions over land, sea, and air, I suspect that Alasdair Macleod will be proven right when he said the following in his March 3, 2022, missive: “The political class has become complacent. For them, their central banks will continue to fund the state’s excess spending while maintaining monetary and financial stability. And one can easily imagine that in dealing with matters of state, central banks are no longer consulted; their support is simply assumed.”

We can hope that is still a possibility because a deflationary depression is preferable to a hyperinflationary depression. And indeed, I just noticed that Senator Joe Manchin has nixed Senate approval for a Federal Reserve seat for Sarah Raskin, a Woke Democrat who advocates endless spending policies for all manner of “progressive” causes. She would presumably be all in favor of MMT. But when push comes to shove, as it most certainly will when we head into the next recession/depression, Republican and Democrat alike will demand that the Fed pump more money into the system. But with Russia and China now increasingly in command economically and holding a corner on essential commodities, another round of massive money printing may signal the last days for fiat money and the dollar. A gold and commodity monetary system with China and Russia calling the shots may be close at hand. Two notable tidbits: (1) Russia’s debt/GDP is <20%. It has a fixed rate income tax of 13% and it has very limited regulation against production; and (2) China has debt but it’s owed to itself, unlike the U.S., which is the world’s largest debtor nation. Both countries own lots of gold. Guess where that leaves the U.S. currency, given a U.S. debt/GDP of 130%!