by Doug Kass

A combination of so-called “demand pull” and “cost-push inflation” is sending up feedstock costs and interest expenses to levels that I believe will soon lead to a marked contraction in U.S. corporate profit margins.

In fact, we already saw this phenomenon in first-quarter earnings reports across a host of industries, from consumer-packaged goods to social media. While the cut in U.S. corporate-tax rates has mostly masked these drags and headwinds, the rising cost of everything will likely worsen in the year(s) to come.

For example:

- Interest Costs Are Climbing. The Federal Reserve is raising interest rates and reducing its balance sheet’s size The European Central Bank will soon follow as it tapers its own quantitative-easing program.

- Energy Costs Are Making New Highs. Rising oil prices are a tax on consumption.

- Commodity Prices Are Rising. Lumber and steel are just two of the commodities that are bolting higher.

- Labor Costs Are Growing. A November midterm-election “blue wave” of Democratic congressional victories might only accelerate the trend.

- Trucking/Transportation Costs are Exploding. Every single good that’s transported is costing much more to deliver.

- A Strengthening U.S. Dollar. This weighs on U.S. trade, as well as on multinationals who export products.

- Regulatory Expenses Are a New Threat to Technology/Social Media. There’s little doubt that Alphabet/Google (GOOG) , (GOOGL) , Facebook (FB) , Twitter (TWTR) et al. will have to accelerate hiring of compliance people and others who monitor and supervise the dissemination of personal data. This will place a new drag to profits.

These influences are occurring at a time when U.S. and global economic figures growing more and more ambiguous, earnings-per-share comparisons are becoming more challenging and the U.S. deficit is swelling (see here and here).

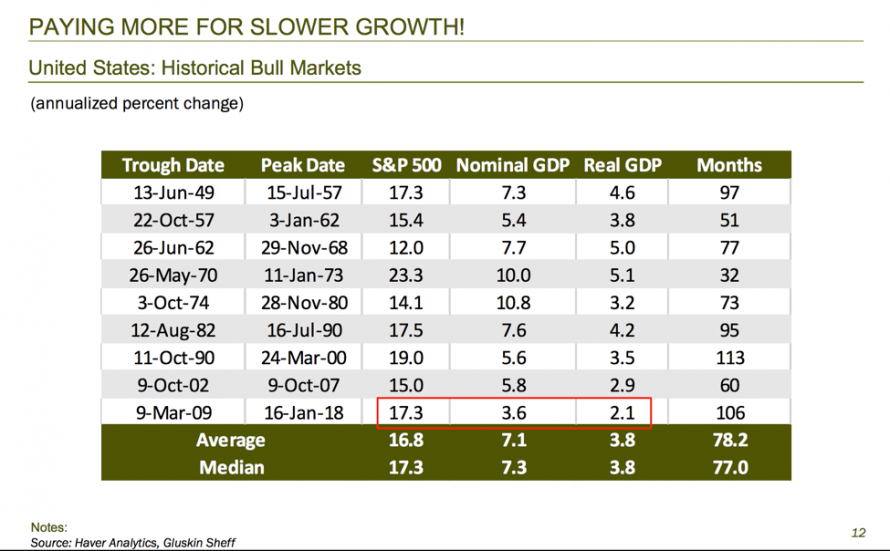

Valuation Worries

Valuations are higher than most recognize when measured against feeble economic growth and too-optimistic EPS forecasts

Gluskin Sheff’s David Rosenberg last week delivered an interesting report with the chart below, which shows that investors are paying more for less U.S. economic growth. He concluded that U.S. stocks have only been so expensive only 9% of the time in history:

Here’s a good take on Rosenberg’s analysis from my pal Lance Robert’s Real Investment Advice

“The market is currently overpriced and overvalued by about a third. While investors can certainly bid up prices in the short-term, the long-term fundamentals will eventually come to play.

With households more exposed to financial assets currently than at any other point in history, the next downturn will be greatly exacerbated by the “panic” that ensues. As you can see in the chart above, the last two peaks in this ratio almost perfectly coincided with the dot-com crash and the 2008 financial crisis.

David [Rosenberg’s] most salient point came from a quote from Federal Reserve Bank of San Francisco. He pointed out that, having access to tons of research, they themselves admit that equity valuations are so stretched that there will be no returns in the next decade: “Current valuation ratios for households and businesses are high relative to historical benchmarks … We find that the current price-to-earnings ratio predicts approximately zero growth in real equity prices over the next 10 years.”

Basically, the Fed is giving investors an explicit warning that the market will ‘mean revert.’ But revert, doesn’t mean stop at the mean.

According to David’s calculations, if the household net worth/GDP ratio reverted to the mean, savings rates would go from 2% to 6%. As a result, GDP would go down 3%, which would have nasty consequences for the economy and, in turn, stocks. Just something to think about.”

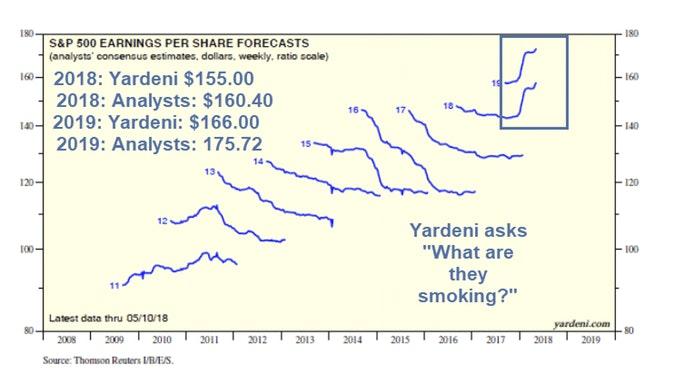

With a moderating trajectory of economic growth and rising cost pressures, I believe that 2018-19 consensus EPS forecasts are too optimistic.

Edward Yardeni’s post: What Are Stock Industry Analysts Smoking? further illustrates the risk that companies might not realize current profit forecasts. Here, the difference between Yardeni and the consensus comes closer into focus:

The Bottom Line

Valuations are high, particularly in light of how much (or how little) economic growth that we’re seeing. The end of global quantitative easing is also at hand, while feedstock costs of all breeds are rising.

Add it all up and this might be a good time to derisk, as the possibility of stagflation looms ever closer. The bottom line: Investors are paying too much for stocks given slowing economic and corporate-profit growth, coupled with the pressure of rising costs of all kinds.

Doug Kass

Since 2004 Doug Kass has served as President of Seabreeze Partners Management, Inc. He runs a hedge fund and individual managed accounts, co-authored “Citibank: The Ralph Nader Report” with Ralph Nader and the Center for the Study of Responsive Law in the 1970s and wrote “Doug Kass: A Life on the Street” two years ago (John Wiley). Since 2003 Mr. Kass served as a guest host on CNBC’s “Squawk Box” and has guest hosted Bloomberg’s “Market Surveillance” for the last five years. Along with Jim Cramer, Doug is the principal contributor to Real Money Pro.