“It’s okay to be wrong; it’s unforgivable to stay wrong.” – Marty Zweig, (October 16, 1987 Wall Street Week – at six minute and 40 second mark!)

As observed on Wall Street Week 31 years ago by Lou Rukeyser, the Dow Jones Industrial Average “crashed” by more than 230 points in the week ending October 16, 1987 – knocking out all previous records. In the aforementioned video (above) Lou cited a tumbling in Treasury bonds, jitters in the Persian Gulf, an discouraging political situation, scary layoffs on Wall Street and, of course, the mindless computer based (“portfolio insurance”)selling. (Full disclosure I managed some of the family’s wealth while a General Partner at Glickenhaus and Co.)

Sound familiar? It is (as last week’s market dive was also conspicuous in it’s character)!

But the worst was yet to come on the following Monday (October 19, 1987) , when the DJIA dropped by 22% on the day.

As I have often noted history rhymes – though history doesn’t necessarily repeat itself. And (as Benjamin Disraeli reminded us), what we have learned about history is that we have not learned about history.

Beginning early this year I argued that the market was in the process of making an important top. I described a market top and bottom as resembling an ice cream cone – that tops are processes and bottoms are events.

With the benefit of hindsight it is clear that the market’s nine year uptrend and Bull Market have likely been broken.

The question is whether we are entering a full fledged Bear Market.

While I believe we may get some seasonal respite over the next two weeks, I would conclude (with the normal caveats) that we have not only broken the Bull Market uptrend but that the odds are rising that we may be approaching a Bear Market.

At 103 months, we are currently into the second longest Bull Market in modern investment history. (The 1990-2000 Bull Market lasted 110 months). On average, those seven Bull Markets have lasted 76 months. And, on average, the mean decline from the peak of the last six longest Bull Markets has been -51%.

Here are the top ten reasons why we may be entering a Bear Market:

1. Markets Generally Move in Anticipation of a Change in the Rate of Economic and Corporate Profit Growth – That Path and Trajectory Are Deteriorating: Since 1860 there has been at least one recession in each decade – representing 47 recessions since the Articles of Confederation was approved in 1781. We have not yet had a recession in the current decade but, my view is that this decade will not be spared and that we will likely be in a recession in the second half of next year. (See my 15 Surprises for 2019).

2. President Trump is Making Economic Uncertainty and Market Volatility Great Again (#MUVGA). Trump’s more frequent and incendiary twitter utterances and behavior reflects badly on him, his office and our country. His conduct and policy (often seemingly written ad hoc on the back of a napkin) are arguably beginning to adversely impact our markets as his Administration’s dysfunction and policy (conflated with politics), and have begun to reduce business and consumer confidence and is starting to negatively influence the real economy.

We are in a unprecedented politically toxic and divisive backdrop – which was underscored during Wednesday’s funeral for President George H.W. Bush. As my good pal Mike Lewitt (‘The Credit Strategist’) wrote over the weekend,

“The saddest thing is not that Bush passed – it was his time – but that his generation is succeeded by a bunch of greedy, narcissistic empty suits.”

This is happening at a point in history where the world has grown more complex, interrelated, networked and flat. With these conditions in place, there are more dominoes today than yesterday and more yesterday than the day before. Again, from Mike,

“The next crisis is approaching and not only is it self-imposed but we are ill-equipped to manage it precisely bc there are few men like George H.W. Bush to lead us.”

a. The United States is leaning more and more “purple” – moving to the Left at a time that the Right is feeling terribly insecure after 10 years of The Screwflation of the Middle Class (something I initially discussed in an editorial I wrote for Barron’s in 2011). The schism between the “haves and have nots” has not been addressed by policy (and has been worsened by the trickling up from the tax bill, which was intended to trickle down and by such provisions as real estate tax and mortgage interest limitations which have served to dent the residential real estate market).Further neglecting or failing to narrow this split will likely have grave social, economic and market ramifications down the road (or sooner).

b. It is becoming increasingly clear that the 2016 election was materially a vote against Hilary Clinton. Trump’s road to nomination in 2020 is growing more precarious and the odds, after barely winning the first time, are not favorable that he wins reelection (given the Wisconsin voting results as well as the outcomes in Michigan and Pennsylvania). It is hard to see markets prospering with Washington D.C. in such a mess – preventing anything from getting done on deficits, debt, taxes, spending and infrastructure.

c. “The Orange Swan” has grown increasingly untethered in the face of divisive and extremely partisan midterm elections (that brought the House under Democratic control), the implicit threats of the Mueller investigation, the hostility of the Kavanaugh hearings, the controversy surrounding the Khashoggi killing, etc. The White House’s dysfunction and repeated personnel changes would be laughable if they weren’t so sad. Most recently, a hardline approach on trade (with China) seems to have tipped over the markets in recent days. Increasingly, short term solutions are being advanced in the face of long term problems. (A classic example is our burgeoning deficit, endorsed by both parties, that is unchecked and is running wild this year).

d. As we are move further from the midterm elections. my core expectation is that the President will likely be impeached by the House. Though there may be far less reasons for Senate Republicans to tie their political futures to such an individual – especially with a plethora of qualified Republican presidential hopefuls – the Senate vote on impeachment could be closer than many expect.

3. A Pivot in Monetary Policy: For years a zero interest rate policy in the U.S. has served to repair the domestic economy as it came out of the Great Recession in 2007-09. Unfortunately it has had second order consequences like pulling forward economic growth – already seen in Peak Housing and Peak Autos. Artificially low rates have served to protect many corporations who have been temporarily resuscitated. Some of those should not have been permitted to survive – and they won’t in the next recession. This served with liberal loan terms (“covenant lite”) could produce a surprisingly steep economic downturn compared to consensus expectations.

4. Economic Growth and Profit Estimates Are Substantially Too High: With U.S. Real GDP forecast to fall back into the +1% to +2% range in 2019’s first half and turning negative in the second half, the contraction in valuations (so apparent thus far in 2018) may continue in 2019. (See my 15 Surprises for 2019). Over there, matters are worse. England has never been more divided (Brexit), Italy (one of the largest economies in the EU) is on the economic deathbed, Deutsche Bank (DB) (and its monstrous derivative book, poor loan quality and systemic money laundering) is the most dangerous financial institution in the world and two of Europe’s most important leaders (Merkel and Macron) are so unpopular that both may be on the way out.

5. The Chinese Challenge to U.S. Hegemony Is a Battle For the Next Century – It Will Likely Be Long Lasting, Disruptive to Current Supply Chains and Costly to Profits: We have likely started a lengthy ‘Cold War in Trade’ with China – a time frame measured in years not (three) months.

6. The Apple Complex (its suppliers) Have Been Upended by a Maturing High-End Smart Phone and Weakening iPhone Market and The Social Media Space is Under Increased and Costly Regulatory Scrutiny: These factors have a broad impact on the market leading technology stocks and for the market as a whole. Moreover, over the last decade technological progress has outpaced regulatory supervision – but this is now being reversed as the social media companies now face the existential threat of rising regulations. The costly imposition of regulatory oversight is something I have been writing about for over a year.

7. An Avalanche of Debt: The private and public sector are levered more than any time in history as, rather than addressing the flaws in our system, we tried to solve the last debt crisis with trillions of dollars of more debt. It is the existence of this mountain of debt that has delivered a fragile economic recovery despite a 2 1/4% Federal Funds rate. Given this, a rate hike of only 25 basis points today has about the same impact of 75 basis points a decade ago. As such that accumulated debt loads are vulnerable to a weakening economy and/or rising interest rates (there have been eight rate hikes since the 2016 election.

8. The Market’s Structure Has Made Equities More Vulnerable Than At Any Time Since October, 1987 (see the Wall Street Week interview from October 16, 1987, above): Passive products and strategies (which are generally agnostic to fundamentals) are the dominant factors in market trading. Like “Portfolio Insurance” 31 years ago, they “buy high and sell low.”

9. With Short Term Interest Rates Now Meaningfully Above the Dividend Yield on the S&P 500 Index – There Is Now an Alternative to Stocks: The dividend yield on the S&P is about 1.8% compared to a one month Treasury note rate of 2.35%, a six month note yield of 2.54% and a one year note yield of 2.68%. Goodbye T.I.N.A. (‘there is no alternative’) to C.I.T.A. (‘cash is the alternative’). In terms of valuations, too many look at Non GAAP earnings (15-16x forward EPS) and ignore the record difference between Non GAAP and GAAP which would move the price earnings ratio to close to 20x. As well price to book, price to sales, market capitalization to GDP and Shiller cyclically adjusted P/E ratio speak (graphic) volumes about the degree of overvaluation today.

10. Technical Damage: Uptrends in place for nearly a decade have been reversed.

More Marty

On a more upbeat note, here is some more wisdom from the legendary Marty Zweig:

- Patience is one of the most valuable attributes in investing.

- Big money is made in the stock market by being on the right side of the major moves. The idea is to get in harmony with the market. It’s suicidal to fight trends. They have a higher probability of continuing than not.

- Success means making profits and avoiding losses.

- Monetary conditions exert an enormous influence on stock prices. Indeed, the monetary climate – primarily the trend in interest rates and Federal Reserve policy – is the dominant factor in determining the stock market’s major decision.

- The trend is your friend.

- The problem with most people who play the market is that they are not flexible.

- Near the top of the market, investors are extraordinarily optimistic because they’ve seen mostly higher prices for a year or two. The sell-offs witnessed during that span were usually brief. Even when they were severe, the market bounced back quickly and always rose to loftier levels. At the top, optimism is king, speculation is running wild, stocks carry high price/earnings ratios and liquidity has evaporated. A small rise in interest rates can easily be the catalyst for triggering a bear market at that point.

- I measure what’s going on and I adapt to it. I try to get my ego out of the way. The market is smarter than I am so I bend.

- To me, the “tape” is the final arbiter of any investment decision. I have a cardinal rule: Never fight the tape!

- The idea is to buy when the probability is greatest that the market is going to advance.

Bottom Line

“More than any other time in history, mankind faces a crossroads. One path leads to despair and utter hopelessness. The other, to total extinction. Let us pray we have the wisdom to choose correctly.” – Woody Allen

Slowing economic growth, lower than expected profit growth, an untethered President, a dangerous change in market structure (impacting the trading transmission) and the other conditions listed in my Top 10 (above) provide robust headwinds to the U.S. stock market in 2019.

A hugely underappreciated fact is that because of the large accumulated debt loads in the private and public sectors over the last decade, a 25 basis point rate hike today is equivalent to almost a 75 basis point rate hike in 2008. So the eight hikes since the 2016 election is equivalent to almost 24 hikes of the past!

As is often the case in a maturing economic recovery and an extended Bull Market we are now finding out who is swimming naked. That tide is moving out further than at any time since the Generational Low in March, 2009.

Volatility, inversely related to liqudity, has entered a new regime – not seen since the early 2000s – providing a further challenge to investors’ confidence as they have grown unaccustomed to large daily market swings.

The Bull Market uptrend, in place for almost a decade, is now being threatened – investors are underpricing and under appreciating risk.

I am sticking to my baseline expectation that the market has been making an important top since late January, 2018, and that a Bear Market may be imminent.

Indeed, the four decade benign backdrop for financial assets may now be over.

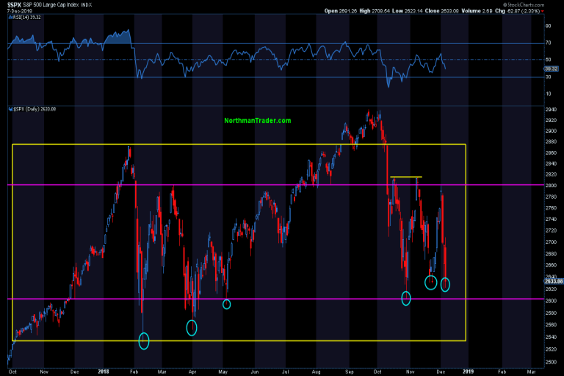

I remain in the 2550-2775 S&P trading range camp over the next month (the Index closed at 2633 on Friday) – implying a slightly positive reward v. risk ratio skew:

Source: NorthmanTrader.com

There were some positive divergences (e.g., number of NYSE new highs v. new lows) on Friday as well as some other near term positives including the positive RSI and MACD divergences which resemble the 2015 and 2016 lows and show the potential for double bottoms.

While my view is that we might get some seasonal strength in the next few weeks, the upside will likely be limited and could set the stage in 2019 for a far more challenging year than in 2018.

Heed Marty Zweig’s pearls of wisdom (above).

I am.