by Doug Kass

- Peak Housing, Peak Autos, a Pivot in Monetary Policy Spell Peak Global GDP and an Economic Slowdown in late 2018 and in 2019

- Watch the Fixed-Income Markets (and the flattening yield curve) That Are Providing the “Tell” that Slower Growth Lies Ahead

- The Buzz of Synchronized Global Growth Has Faded

- What Makes Equities Even More Vulnerable is that the Leading Component of the Markets, ‘FANG,’ Has Become Diminished and Is Now ‘GA’

- Tops Are Processes, and We May Be in That Process Now

“In one corner, U.S. Treasury Secretary Mnuchin in a truly out-of-character gaudy, shiny white satin robe brandishing a big 3%. Opposite the optimist is the old guard Federal Reserve representing nearly 800 of the country’s PhDs. They’ve donned black as night robes with a difficult-to-make-out 2% on the back. In the case you get out more than we do, you’ve arrived at the battle royal for potential gross domestic product (GDP) growth! Mnuchin contends the U.S. economy is “well on the path” to sustained annual growth of 3% for “several years.” The Fed’s army of economists foresees a much lower speed limit of 1.8%.” –Danielle Dimartino Booth, The Daily Feather

While the global markets have generally ignored terrorist attacks, a series of currency crises, trade concerns, an arguably untethered President Trump (who has conflated hastily crafted policy with politics) as well as other adverse political, geopolitical and market-unfriendly “big picture” events over the last several years, it is my view that the growing ambiguity seen in the high-frequency economic data around the world forms the principal risk to equities.

Peak Housing

In case you missed this from last Friday, Redfin (RDFN) , the residential real estate brokerage firm, fell 22%.

On the conference call Redfin CEO Glenn Kelman said this: “For the first time in years, we are getting reports from managers of some markets that homebuyer demand is waning, especially in some of Redfin’s largest markets.” He specifically cited Seattle, Portland and San Jose, but also said “The trend is continuing in July and reports are now coming in from Washington, D.C., Boston, VIrginia and parts of Chicago as well that the homes there are getting harder to sell.”

We know the reasons and it’s been stated in my Diary for weeks:

- Mortgage applications are turning negative on a year-over-year basis

- Mortgage rate resets and higher mortgage rates are a headwind to new home sales and refinancings (at an 18-year low)

As reported by my pal Peter Boockvar, the U.S. housing market outlook is moderating:

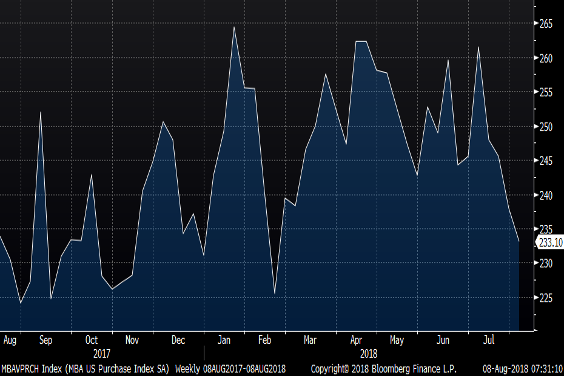

With mortgage rates at a 7 year high and the average price of a home at a record high, mortgage applications to buy a home fell 2% w/o/w and down for the 4th straight week. It is now down by 1.6% y/o/y and the index is at the lowest level since mid-February. Refi’s fell by 4.5% w/o/w and 35% y/o/y. This index stands at the weakest level since December 2000. This follows new home sales, existing home sales, and housing starts reflecting a plateauing in the pace of transactions.

PURCHASE APPLICATIONS

From my perch, a combination of sky-high home prices (which in many areas of the country are back above mid-2000s cyclical highs) and rising mortgage rates are squeezing home affordability, and a Peak Housing moment is upon us.

In the recently reported robust second-quarter GDP print of 4.1%, residential construction was the only category that turned negative. That follows a contraction also seen in the year’s first quarter.

Peak Autos

“(Auto) sales in the last month will underscore investor fears that auto sales have peaked and that, without ever-higher incentives to keep consumers interested, demand will continue to soften.” –Bloomberg

Ward’s Automotive reported a 16.7 million U.S. SAAR (seasonally adjusted annual rate) of sales for the month of July; that is the weakest July sales month in four years:

Source: Zero Hedge

Auto industry sales are likely to get much worse in the year ahead.

As I mentioned in a recent Bloomberg interview, the recent consumer confidence report was noteworthy for the depressed spending intentions. According to my economist pal David “Rosie” Rosenberg:

“Plans to buy an automobile (over the last two readings) exhibited the weakest back-to-back showing in over five years.”

“Peak Autos” has been a theme of mine over the last 12 months; General Motors GM is on my Best Ideas List as a short, placed on that list at $43.43 in October 2017.

Remember: Cyclical stocks always look cheap at the top of a cycle.

Despite the hedge fund community’s endorsements by Ed Wachenheim and others, and the business media’s almost universal optimism on these name, it remains my view that GM and Ford F are “value traps.” (Note: Both companies recently guided lower in sales and profits).

Despite stagnating real personal incomes and large household debt loads, the proliferation and the popular extension of subprime auto debt (“a dollar down and off to the races” and the perpetual extension of loan maturities) and large auto price incentives have served to lift car sales over the last few years well above replacement needs. For several reasons, the favorable gap previously seen between auto sales and replacement needs is likely to reverse over the next few years.

Most importantly, with interest rates rising and likely to rise further, it is getting prohibitively expensive for manufacturers to offer incentives and deals tied to loans, so the consumer will be faced with fewer discounts on new cars. Indeed, J.D. Power reports that for the first time in almost five years the auto industry recently has cut back spending on incentives.

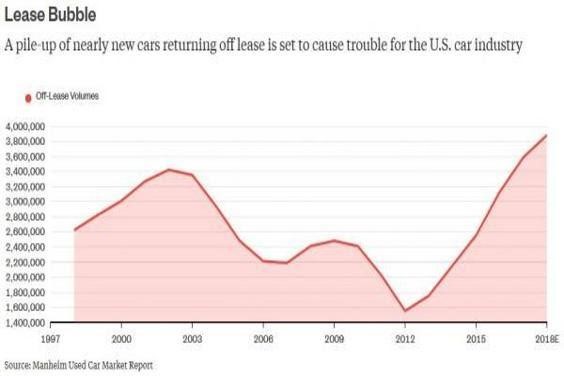

What makes things worse is the large number of cars coming off lease and ending up for sale in the used car lots of dealers. The “lease bubble” (below) is providing auto buyers with lower-priced alternatives to the new models.

Here are 10 troublesome charts on auto loans from Zero Hedge. If you are long the auto stocks, read the material closely.

Perhaps the most significant is the record level of average vehicle new and used car loans, at $31,100 and $19,500, respectively. But, with rates rising, so do dollar payments per month — on average, at more than $515 per month on new vehicles, which is stretching affordability for most borrowers. Meanwhile the average loan terms of 69 months for new cars and 64 months for used cars are also likely stretching limits.

Banks and other financial institutions are seeing the risks to the above loans and aggressively are slashing their auto loan origination activity, leaving captive original equipment manufacturer (OEM) finance companies to fill the void.

Look out below, and brace for a sharp fall in auto industry sales over the next year.

A Monetary Pivot

From Rosie this morning:

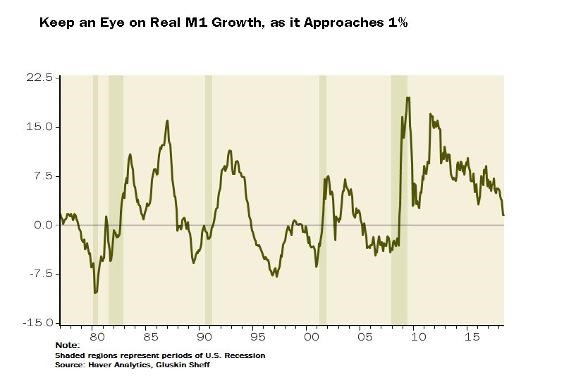

“All of the monetary aggregates have slowed substantially, and real M1 growth is flagging a 1% stall-speed growth economy once we get passed all the pre-tariff buying activity and fiscal sugar-high that skewed Q2.”

The monetary pivot is not a concession to the U.S.; global central bankers are also reversing course.

Peak GDP

- A services slowdown may already be occurring as a July economic pivot may be in place

- Peak auto sales is not a sector outlier

- Look for consensus estimates of GDP to be revised lowered in the months ahead

Investment and economic wisdom is always 20/20 when viewed in the rear-view mirror.

The recent weak growth in nonfarm payrolls points to the issue of slowing domestic economic growth, already seen in a weakening auto sector.

But, to me, there are other more powerful July signposts that indicate that economic growth is becoming more ambiguous:

- According to National Association of Credit Management data, which measure both manufacturing and services, July’s GDP proxy slowed by almost 1% to 3% from June’s strong rate of nearly 4%.

- The July ISM Manufacturing/Services growth proxy has halved to 2%.

- The July ISM Manufacturing survey for new orders fell to the lowest pace in 14 months.

- ISM Services, reported on Friday morning, missed big, falling to the lowest level in nearly a year.

- ISM Services backlogs dropped to a two-year low in July (51.5). We are in a services economy — 80% of the population resides there — and in our evolving economy a services downturn, rather than manufacturing, can presage an economic slowdown.

- In the Friday jobs report, July services job creation was the slowest month in 2018.

- July business activity, a dependable indicator, fell by 7.4 points from June; that’s the sharpest drop since late 2008.

- The spread between business activity and employment has narrowed to 0.4 points; when it turns negative, companies are overstaffed.

Not only do we face Peak GDP, we are seeing Peak Global GDP growth, as witnessed by a two-year low in Citigroup‘s European economic surprise index. It was only seven months ago that synchronized global growth was the buzz.

Bottom Line

While bulls are anticipating acceleration in the rates of U.S. and non-U.S. economic growth and an extension in the expansion in corporate profits, the reality, based on recent high-frequency economic data, is that the global economy is slowing in its trajectory and that growth in corporate profits will tail off shortly.

This is a nonconsensus view and forms the basis for my ursine market view.

Tops are processes and it is my continued view that a 2018 high in the S&P 500 Index was made in late January.

What makes equities even more vulnerable is that FANG has become GA. (Note the narrowing markets: Microsoft (MSFT) , Netflix (NFLX) and Amazon (AMZN) have accounted for more than 70% of the rise in the S&P Index year to date).

I remain at my largest net short exposure in quite a long time.