by Lance Roberts on Real Investment Advice:

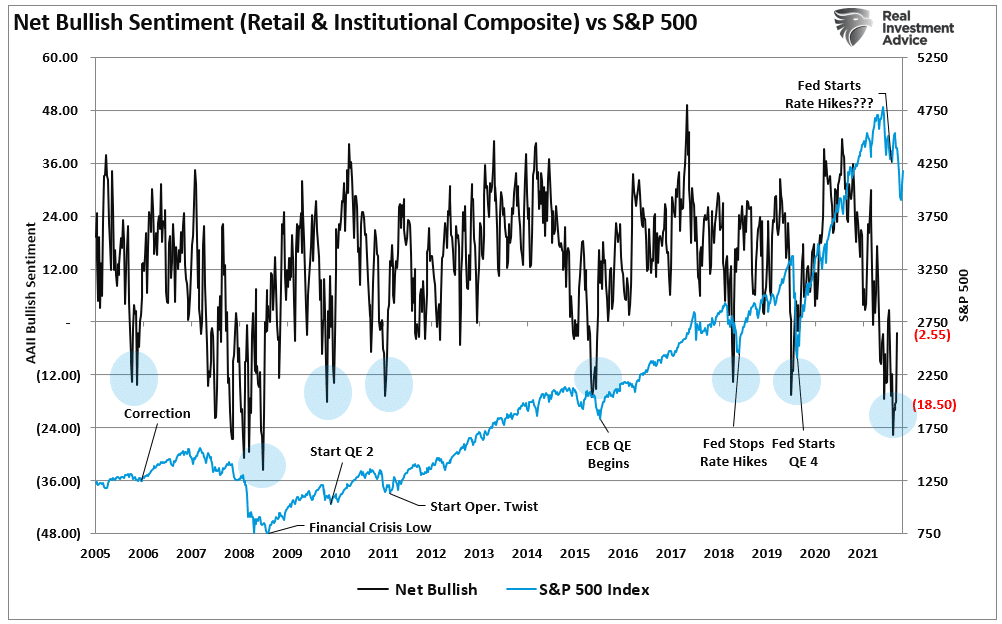

For example, the net percentage of bullish responses from the American Association of Individual Investors (AAII) and the Institutional Investors index (INVI) are near previous bear market lows. Such is despite the sharp rally over the last two weeks.

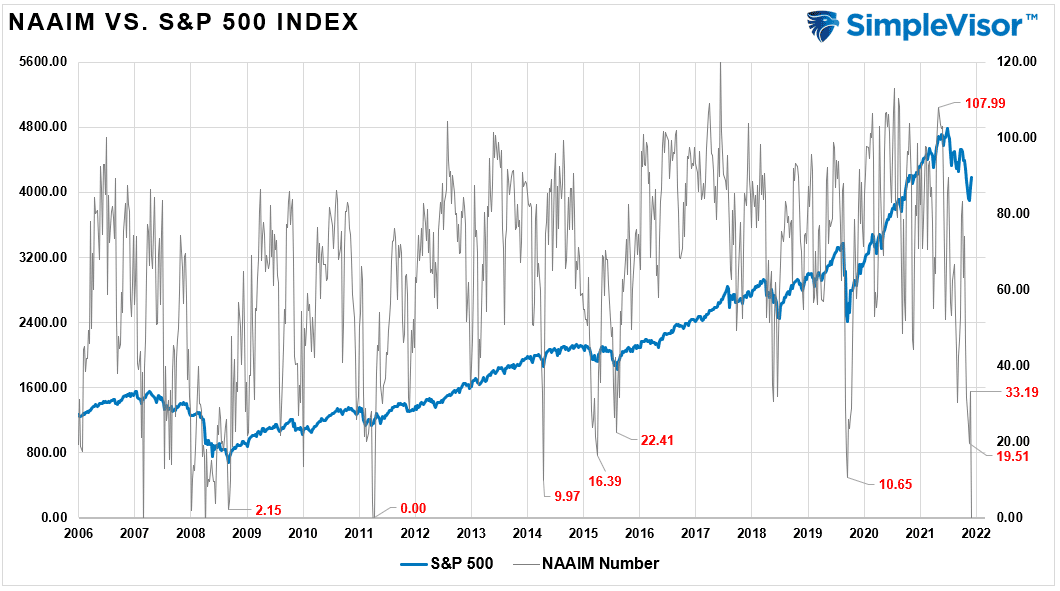

Despite hopes for a rally, the National Association of Investment Managers (NAAIM) shows the same bearishness.

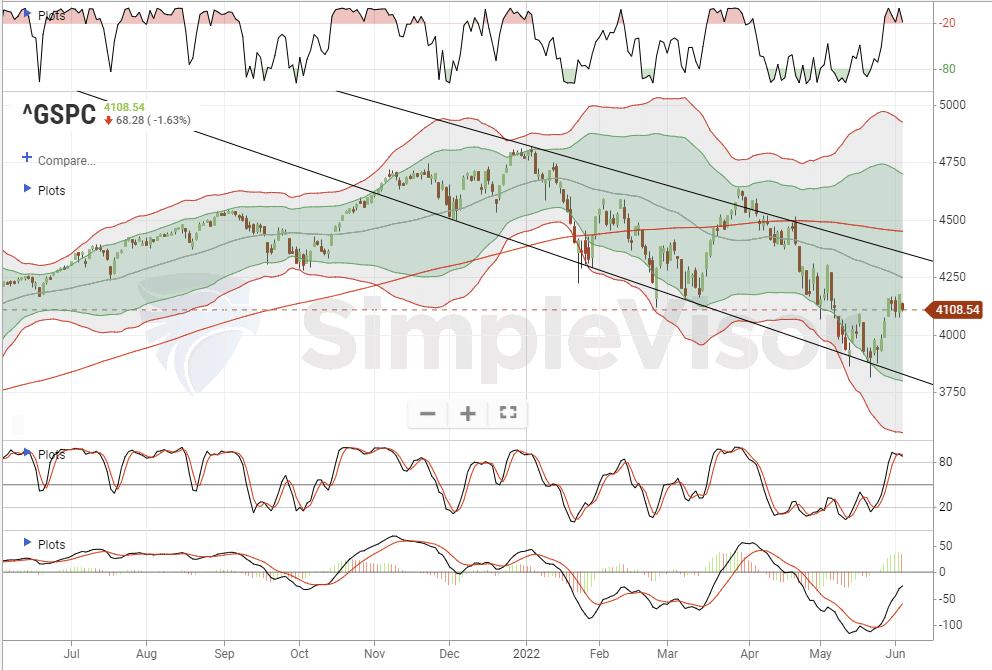

With sentiment so negative, one would assume that a bear market was in full swing, along with an economic recession. However, while it seems investors are terrified of the market and its outlook, the sell-off since January has remained quite orderly. As shown, the S&P 500 index took almost 6-months to decline nearly 20% from its previous peak.

However, what is interesting is that if investors are terrified, why are they not selling?

Investors Are Terrified, But No Sign Of Fear

Despite nearly 6-months of continuous selling, rampant headlines of impending doom, and CNBC’s constant “Market’s In Turmoil” specials, little “fear” remains below the surface. A couple of different gauges provide a view of market “stress.”

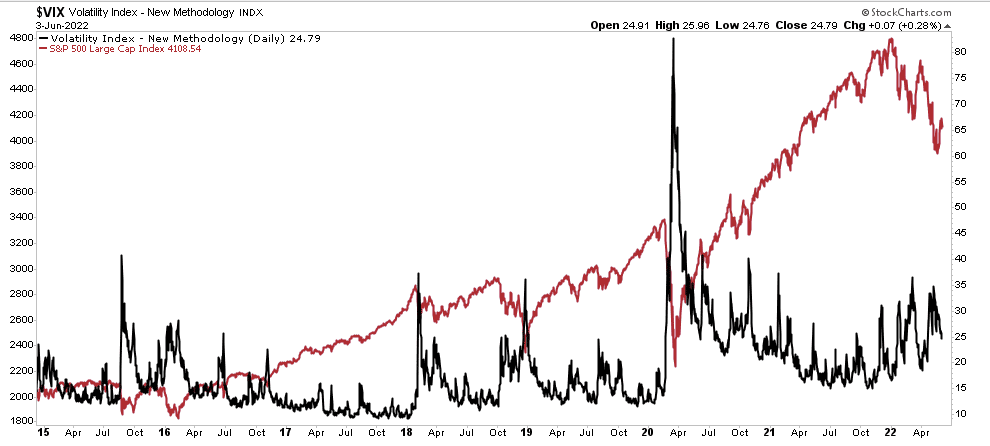

The first is the Volatility Index, or VIX, more commonly referred to as a “fear gauge.” The VIX is a financial benchmark operating in real-time. It gives investors an indication of volatility expectations in the market for the coming 30 days. Historically, spikes in the VIX correlate to market bottoms as investors dump equities.

Despite the recent selling pressure in the market over the last couple of months, volatility remains subdued, suggesting little panic in the markets.

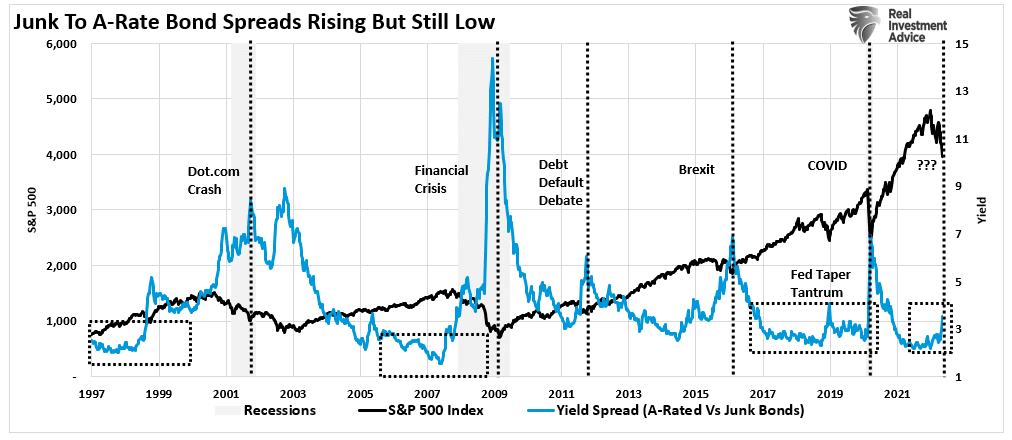

Another measure of market stress comes from the bond market by calculating the difference in yields, or spreads, between various bonds. One standard measure is the yield difference between “junk” and A-rated bonds.

While that spread has risen as of late, which one would expect with recent market stresses, it remains very low by historical standards when markets were in the “grips of a bear.”

If the market were indeed in the grips of a capitulatory selling event, I would suggest both measures of market stress would be substantially higher.

That suggests that even though the media and investors are highly concerned about the markets, they aren’t doing much about it.

Investors Aren’t Selling

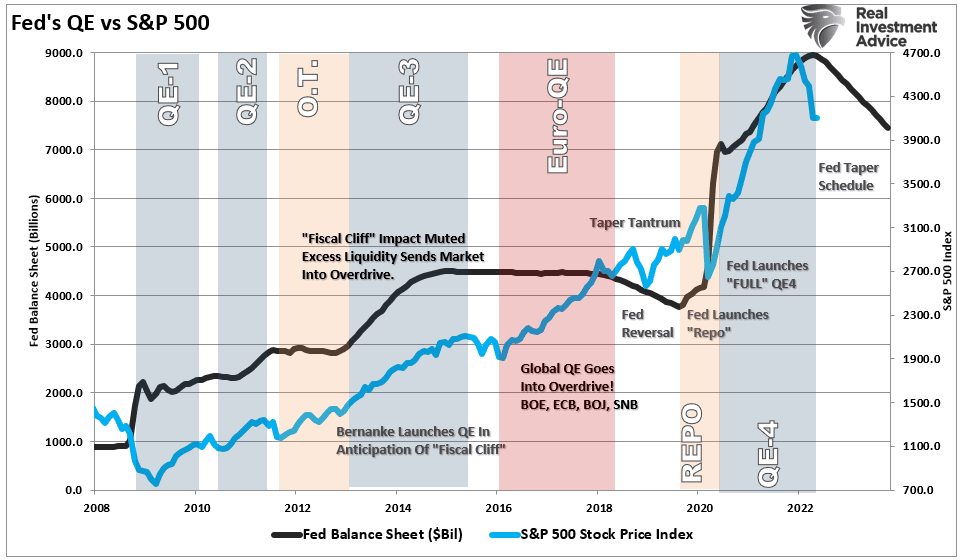

Over the last decade, repeated rounds of monetary interventions created a sense of moral hazard in the financial markets.

What exactly is the definition of “moral hazard.”

Noun – ECONOMICSThe lack of incentive to guard against risk where one is protected from its consequences, e.g., by insurance.

The massive Federal Reserve interventions, bailouts, and zero rates provided a perverse incentive to take on extreme forms of risk, from speculative IPOs to SPACs to Cryptocurrencies. Investors believed the Fed was protecting them from the consequences of risk. In other words, the Fed effectively “insured them” against potential losses.

The lesson taught to investors was that the Fed would bail out any market decline. Therefore, the “fear of missing out”overrides the “need to get out.”

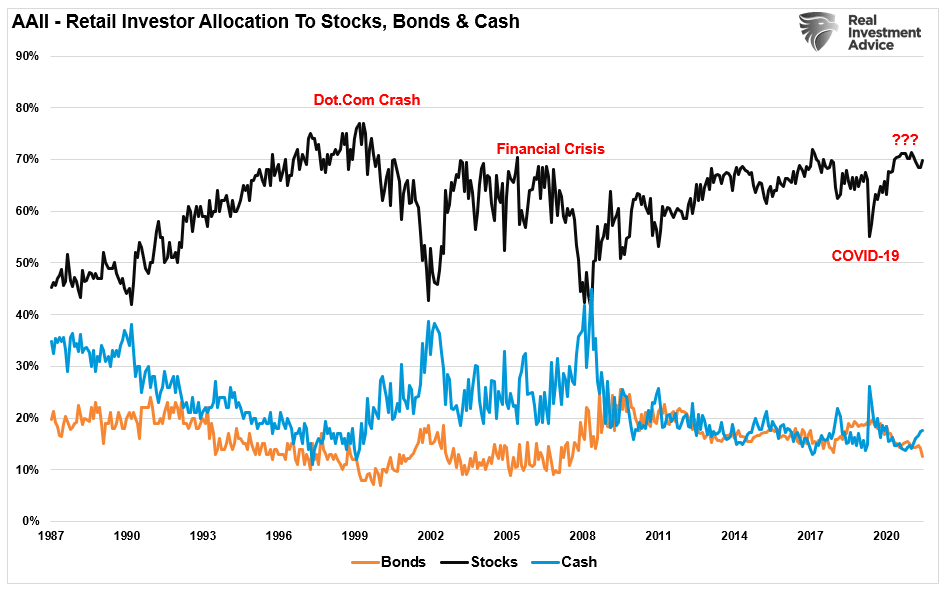

As shown below, the AAII investor allocation to stocks, bonds, and cash tells the story. Despite AAII investor sentiment at very bearish levels, the allocation to equities remains very high while bonds and cash remain low. Interestingly, seemingly terrified investors are still unwilling to sell for the “fear of missing out.”

I should qualify that statement.

While investors aren’t selling just yet, it doesn’t mean they won’t.

There is a point at which every investor will “sell.” For some, it may be a 10% decline. For others, it may be a 40% decline. However, at some point, “everyone sells.”

Since 2009, every time the market dipped, weaved, or bobbed, the Federal Reserve ran to the rescue by increasing monetary interventions. Not surprisingly, many investors hope they will do so again sooner rather than later.

The problem for the market comes when investors begin to realize that with inflation running over 8% annually, the Fed may NOT be coming to the rescue anytime soon.

Eventually, Everyone Sells

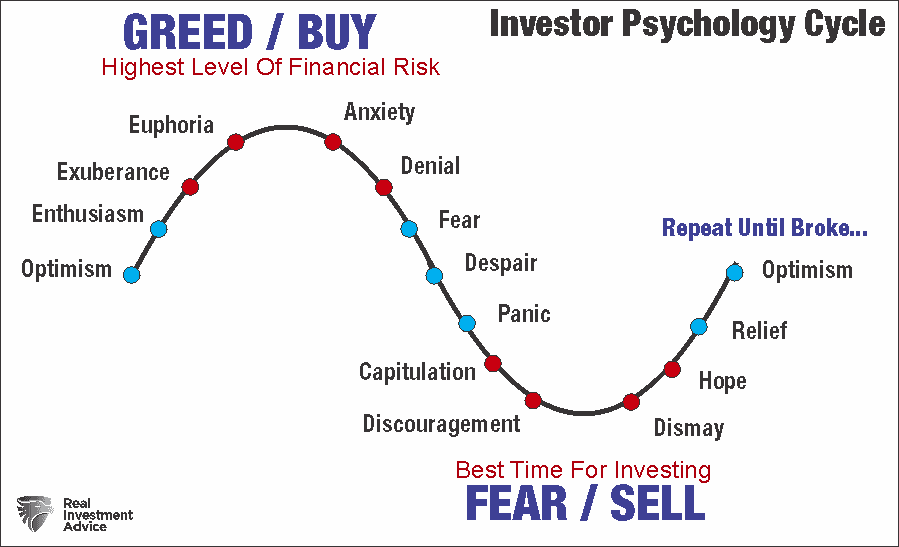

As noted, there is a price where “everyone sells.” The “emotional” strain eventually erodes investor confidence in their previous decisions. This is crucial because there is generally no investment strategy or discipline.

The “herding effect” and “loss aversion” are the most significant behaviors that compound the issues of investor mistakes over time. As markets rise, individuals believe the current price trend will continue indefinitely. The longer the rising trend lasts, the more ingrained the belief becomes. Eventually, the last “holdouts” finally “buy in” as the market evolves into a “euphoric state.”

As markets decline, there is a slow realization that “this decline” is not a “buy the dip” opportunity. As losses mount, the need to “avert loss” increases until individuals seek to “avert further loss” by selling.

This behavioral trend runs counter-intuitive to the “buy low/sell high” investment rule.

Such is the point investors now face as losses mount on financial statements, and every decision made seems to be wrong.

Given the lack of “panic, capitulation, and discouragement,” it is highly likely this particular market cycle is not yet complete.

We continue to suggest using rallies to reduce risk, rebalance allocations, and increase cash levels opportunistically. Such generally provides better outcomes than forced selling when markets fall apart.

As noted, the biggest challenge for most investors is the lack of an investment strategy or discipline from the outset. Such provides the basis for investment decisions based on fundamental, technical, or statistical analysis rather than emotion.

Of course, if you don’t know what an investment strategy or discipline comprises, that may be the best place to start