There was a good bit of excitement on Tuesday with the release of the retail sales report, which came in stronger than expectations. However, the bounce will be difficult to maintain as tapped out consumers face high unemployment and a slow recovery.

As we have discussed many times previously, the consumer is the lynchpin to the economy, comprising roughly 70% of economic growth.

The most valuable thing about the consumer is they are “financially stupid.” But what would expect from a generation whose personal motto is “YOLO – You Only Live Once.” However, this is why you “never count the consumer out,” as they always find a way to go further into debt.

Consumers are also why companies spend billions on social media, personal influencers, television, radio, and internet advertising. If there is an outlet where someone will watch, listen, or read, you will find ads on it. Why? Because psychologically, consumers are “trained” to “shop till they drop.”

As long as individuals have a paycheck; they will spend it. Give them a tax refund; they will spend it. Issue them a credit card; they will max it out. Give them a government stimulus check; they will spend it as well. Don’t believe me, then why is consumer debt at record levels?

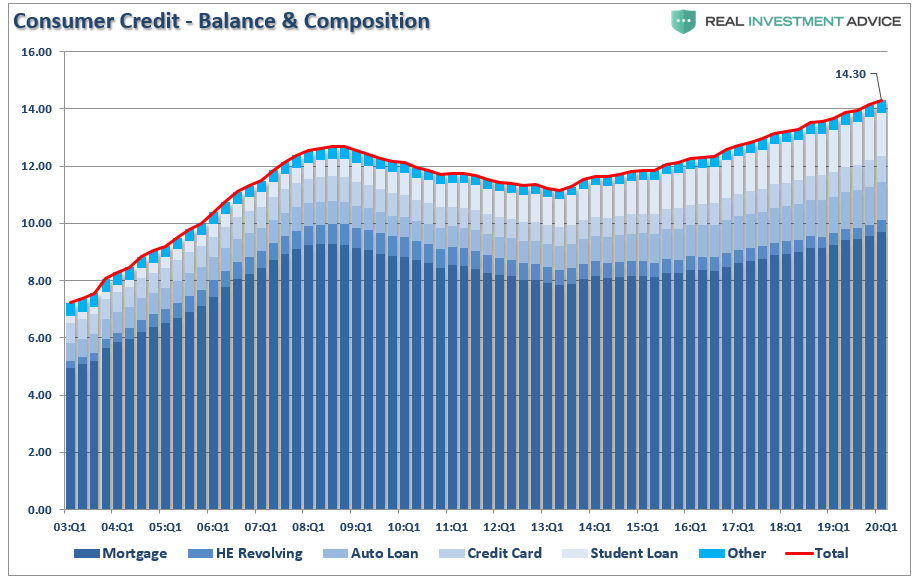

Debt-Driven Consumption

If consumers were even partially responsible, financial guru’s like Dave Ramsey wouldn’t have a job selling products to get people out of debt.

However, consumers spending themselves further into debt is what keeps stock markets going higher and the economy going. Note, that I said “going,” and not “growing,” Take a look at the chart below:

In 1980, household credit market debt stood at $1.3 Trillion. To move consumption from 61% to 65% of GDP by 2000, it required an increase of $5.5 Trillion in debt. Since 2000, consumption as a percent of the economy has risen by just 3% over the last 20 years. To support that increase in consumption, it required an increase in personal debt of more than $11 Trillion.

You should not dismiss the importance of that statement. It has required twice as much debt to increase consumption by 3% of the economy since 2000 than it did to increase it by 4% from 1980-2000. The problem is quite clear. With interest rates already at historic lows, consumers heavily leveraged and economic growth running at sub-par rates; there is not much capability to increase consumption that would replicate the economic growth rates of the past.

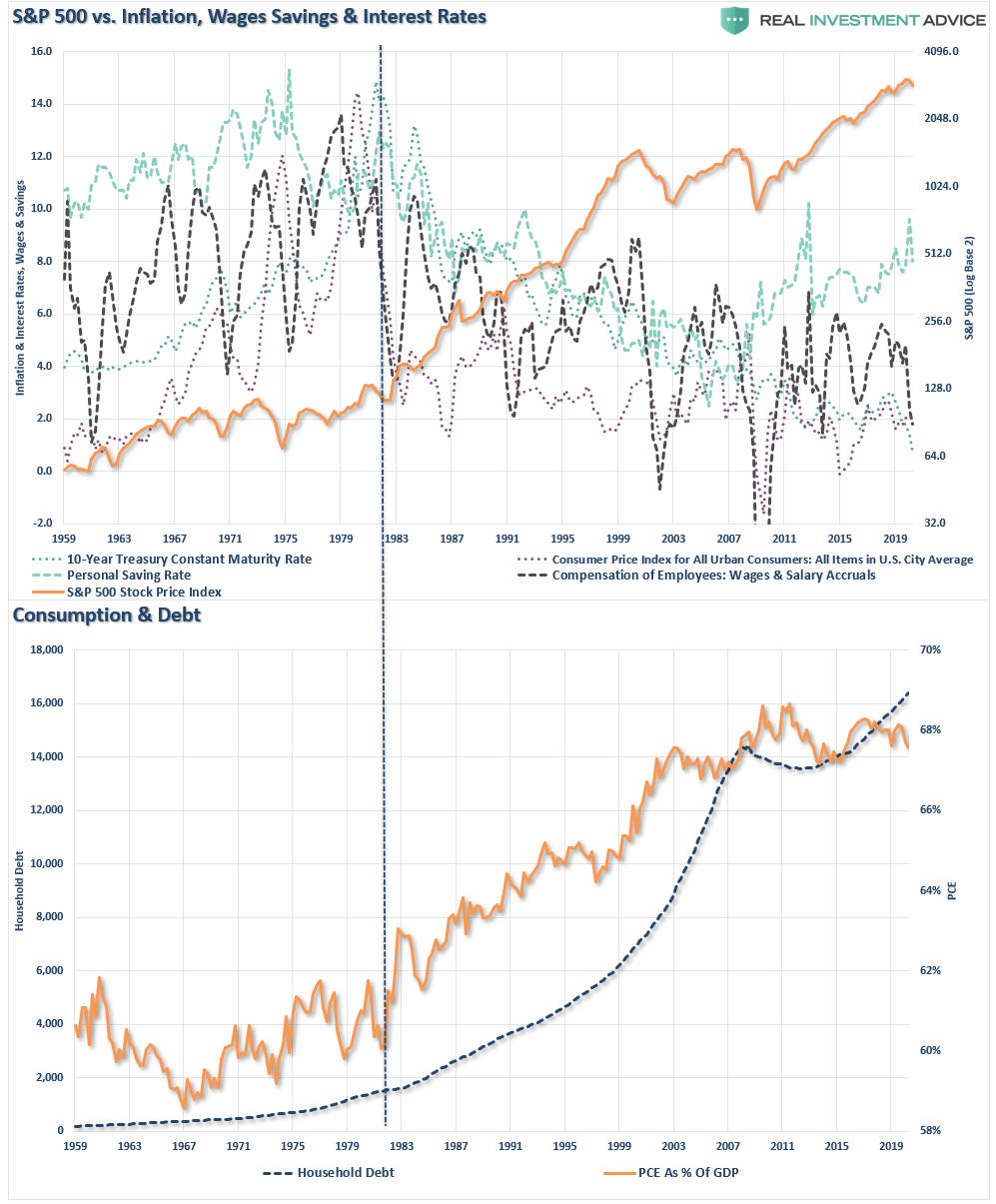

The Mirage Of Wealth

The mirage of consumer wealth has been a function of surging debt levels. “Wealth” is not borrowed but “saved.” Such is a lesson too few individuals have learned.

This record level of household debt is also why the Fed’s measure of “Saving Rates” is entirely wrong. It is also why economic growth will continue to weaken as debt continues to deter disposable incomes away from consumption into debt service.

“The ‘gap’ between the ‘standard of living’ and real disposable incomes is shown below. Beginning in 1990, incomes alone were no longer able to meet the standard of living so consumers turned to debt to fill the ‘gap.’ However, following the ‘financial crisis,’ even the combined levels of income and debt no longer fill the gap. Currently, consumers cannot fill the record $2654 annual deficit to maintain their lifestyle without more debt.”

The gap between the standard of living and incomes is another reflection of the wealth inequality which is pervasive in the economy.

Less Than Meets The Eye

While there was a massive jump in retail sales in May, a look below the headlines revealed a different picture. As noted by Mish Shedlock:

“Despite the surge, sales numbers are back to levels seen in late 2015 and early 2016. On a year-over-year basis, sales are 6.1% below May 2019. Total sales for the March 2020 through May 2020 period are down -10.5% from the same period a year ago.

Here are the 5-month totals:

- Total: -4.7%

- Motor Vehicles and Parts: -10.5%

- Furniture: –18.1%

- Electronics and Appliances: -19.3%

- Building Materials: +6.7%

- Food and Beverage Stores: +13.1%

- Health & Personal Care: -2.4%

- Gasoline: -16.7%

- Clothing: -42.9%

- Sporting Goods: -9.9%

- Department Stores: -21.0%

- Nonstore Retailers: +16.6

- Food and Drinking Places: -22.3%”

Notice the only positive sectors were those directly related to the partial reopening of the economy. Such was not unexpected, but it is also likely unsustainable. The stimulus checks are gone and more checks may be problematic to get through a deeply divided Congress. The additional $600 in unemployment benefits runs out next month, and there is only talk of a bill to extend them at reduced levels.

Unemployment is still a problem.

No Getting Back

Given that retail sales make up roughly 40% of personal consumption expenditures which in turn comprises roughly 70% of GDP, the impact to sustained economic growth is important to consider. As noted unemployment is running at very high levels, but without a substantial pickup in retail sales, re-employment may be disappointing.

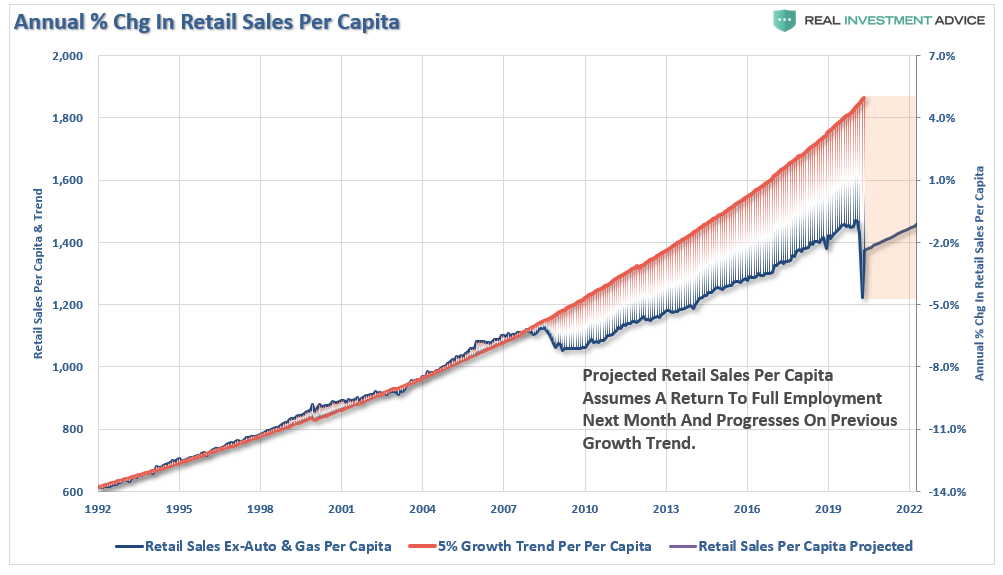

What the headlines miss is the growth in the population. The chart below shows retails sales divided by the current 16-and-over population. (If you are alive, you consume.)

Retail sales per capita were previously on a 5% annualized growth trend beginning in 1992. However, after the financial crisis, the gap has yet to be filled and currently runs at just a 3% growth rate. Assuming we recover to full-employment next month, and retail sales return to its 3% growth trend, retail sales will take another step backward.

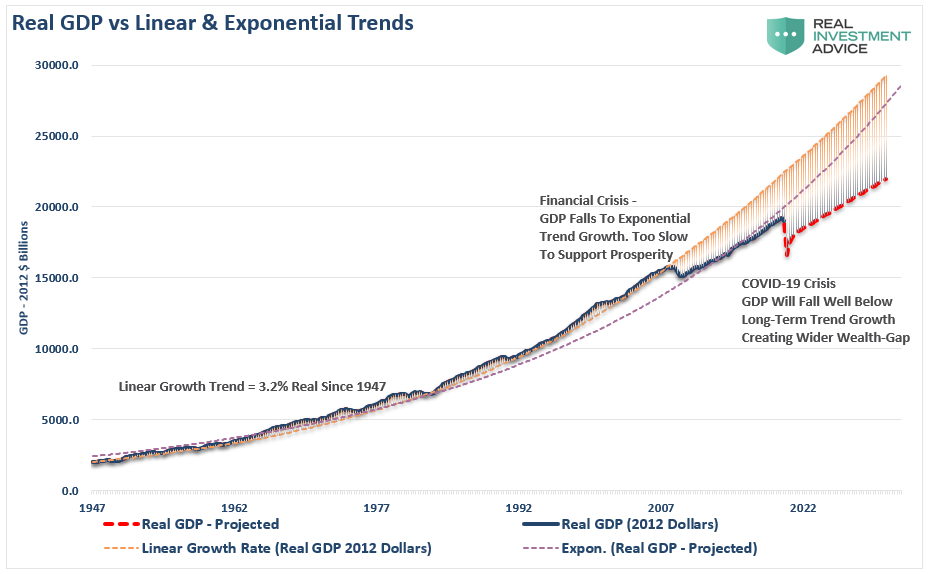

Such is the same outcome as we discussed last week with expectations for economic recovery. To wit:

“Before the “Financial Crisis,” the economy had a linear growth trend of real GDP of 3.2%. Following the 2008 recession, the growth rate dropped to the exponential growth trend of roughly 2.2%. Instead of reducing the debt problems, unproductive debt, and leverage increased.”

Employment Problem

There are two reasons for this, which are continually overlooked or worse simply ignored, by the mainstream media and economists. The first is that despite the “longest run of employment growth in U.S. history,” those who are finding jobs continues to grow at a substantially slower pace than the growth rate of the population. The economic shutdown exposed this weakness.

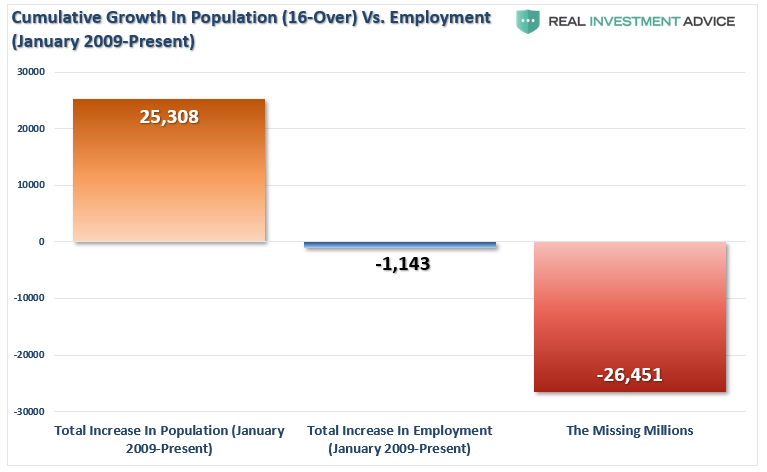

“Since the beginning of the last economic expansion, the working-age population has grown by 25.3 million while employment has fallen by 1.14 million through May. As the BLS confirms above, there are over 26 million who are “missing” due to how employment is calculated.”

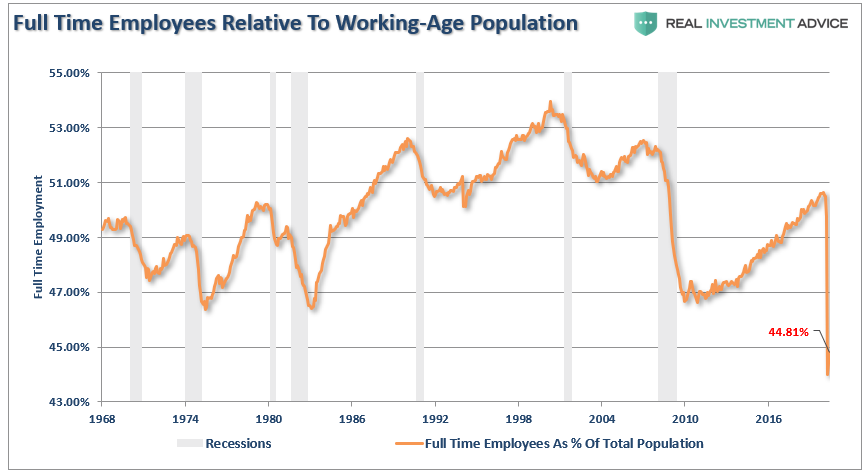

“What is crucially important to the economy is full-time employment, which creates enough income to expand economic growth. The number of full-time employees to the working-age population is at 44.81%, which is not high enough to support economic growth.”

If you don’t have a job, and primarily live on government support (as 1-in-4 Americans currently do), it is difficult to consume at higher levels to support economic growth.

Consumers Are All Tapped Out

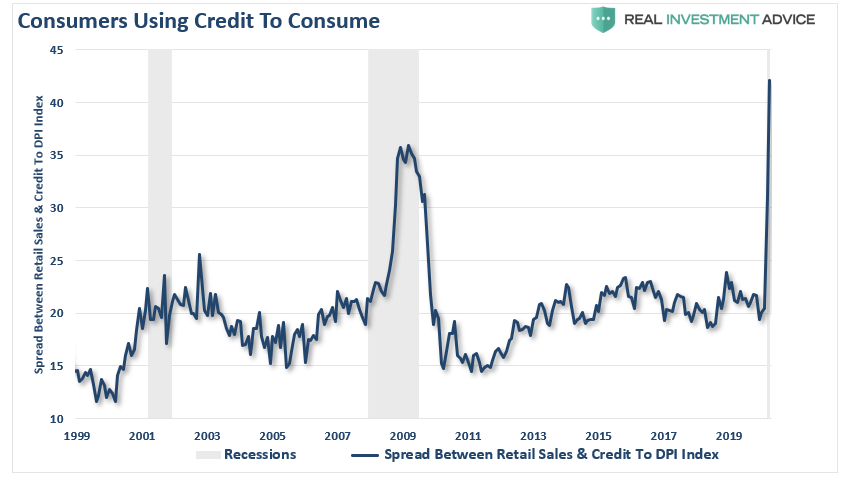

Secondly, while stimulus checks and extra-benefits may provide a temporary boost to incomes, that income boost is only temporary. The reality is that 80% of Americans continue to live paycheck-to-paycheck and have little saved in the bank. With years of wage stagnation, the cost of living now exceeds what incomes and debt increases can sustain.

It is also why despite the annual hopes of “stronger economic growth,” the 3-year average of economic growth continues to deteriorate. With consumers forced to consume more on credit, such will lead to a slower economic recovery as the ability to tap additional credit becomes problematic.

The impact on the economy from record levels of unemployment will have a wide range of impacts forestalling an economic recovery. The first, is a deep suppression of wage growth, which is derived from both recessionary drags and job losses.

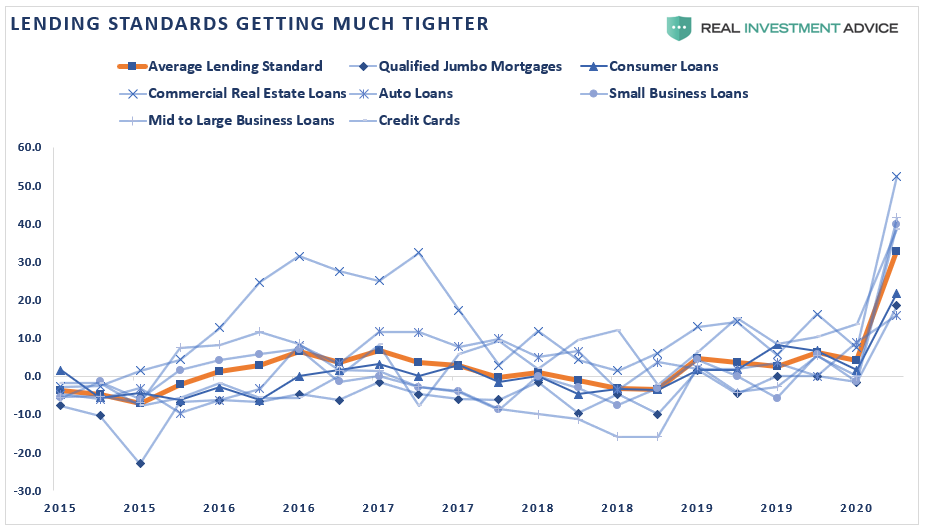

Tightening Up

As stated, with reduced incomes, it is harder to make ends meet harder to obtain additional credit. Given consumers are dependent upon credit to “fill the gap,” and with banks tightening lending standards, access to credit will become more difficult.

Both of these factors will likely ensure the expected “V-shape” recovery in the economy is overly optimistic. While the data has certainly bounced as the economy is reopened, the headwinds will likely stall the advance.

One of the ongoing problems with the data is that aging demographics, massive monetary interventions, and the structural change in employment has skewed the seasonal-adjustments in economic data. These issues skew every report from employment, retail sales, and manufacturing to appear more robust. Such is a problem mainstream analysis continues to overlook but will be used as an excuse when the data reverses.

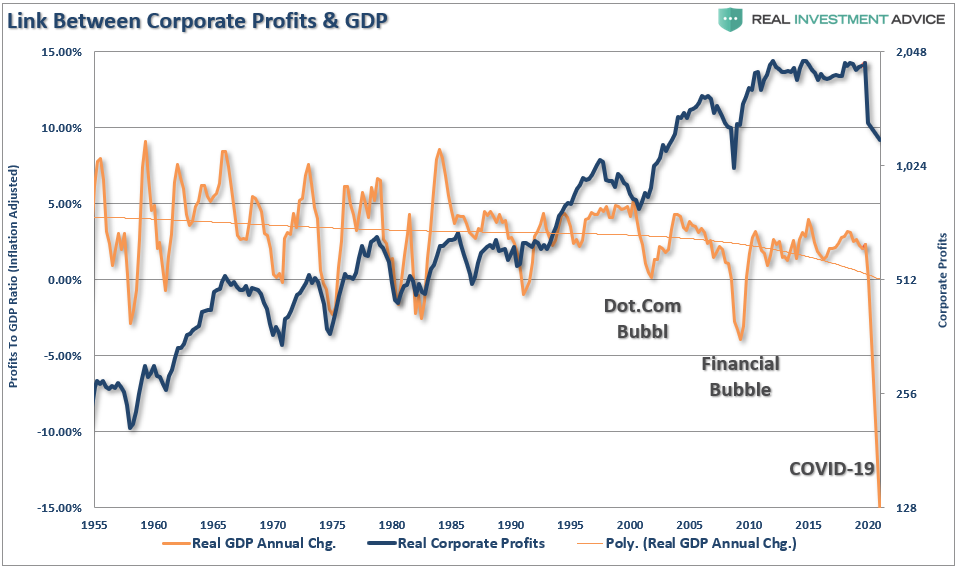

Deterioration in economic confidence is hugely important. The most significant factors weighing on consumption are job losses which crush spending decisions by consumers. Such starts a virtual spiral in the economy as reductions in spending put further pressures on corporate profitability. Lower profits lead to more unemployment, and lower asset prices, until the cycle is complete.

Conclusion

As I discussed last week, the current detachment of the stock market from the economy is likely an illusion that will not last long.

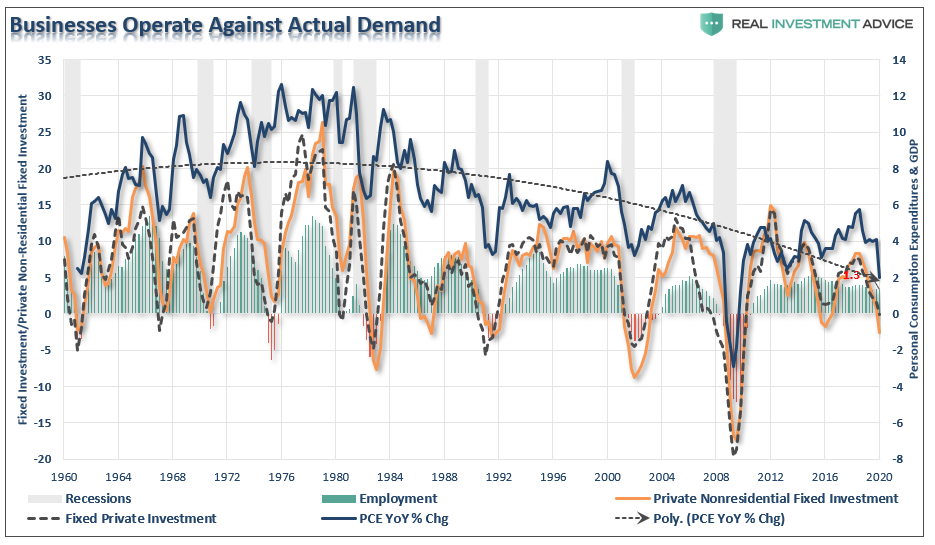

“The economic destruction playing out in real-time will eventually weigh on markets. There is a negative feedback loop between employment and consumption. As unemployment rises, consumption falls due to a lack of income. Since businesses operate based on demand for goods and services, the correlation between PCE, fixed investment, and employment is high.”

As noted, even with the reopening of the economy, businesses will not immediately return to full operational activity, until consumption returns to normalized levels. Without a ready vaccine, if there is a second wave of the virus, consumer confidence would likely reverse. Such would put further pressure on sales and, ultimately, corporate profits.

As I concluded in a note last year:

“It is hard for consumers to remain ‘confident’ and continue spending when they have lost their source of income.“

While the markets have indeed managed a strong “rally” from the March lows, there are reasons to be cautious.

We are just entering into what will likely be a more protracted, deeper, and more damaging recession than what we saw in 2008. Defaults and bankruptcies are only in the very early stages. Liquidity from the Fed has repaired credit spreads for the time being. Still, the longer this recession drags on, the higher the risk is the Fed only delayed the inevitable.

The Federal Reserve did move quickly to assist the credit markets in remaining operational, as discussed here. However, those “emergency measures” don’t translate into more robust economic prosperity, revenues, or corporate profits.

Despite the bounce in retail sales, there will still be no “V-shaped” recovery.

Invest accordingly.