Rescue of housing market in March accidentally burned lenders

Variety of pressures keeping rates from going even lower

The Federal Reserve’s emergency rescue of the U.S. mortgage market should have set off celebration among lenders trying to keep up with demand from borrowers. Instead, executives at Quicken Loans got a hefty margin call.

That was just a fraction of the pain the Fed unintentionally inflicted on lenders in mid-March when it announced plans to buy a massive amount of mortgage securities. The move, meant to steady the market, caught many lenders by surprise and tipped their routine hedges deep into the red.

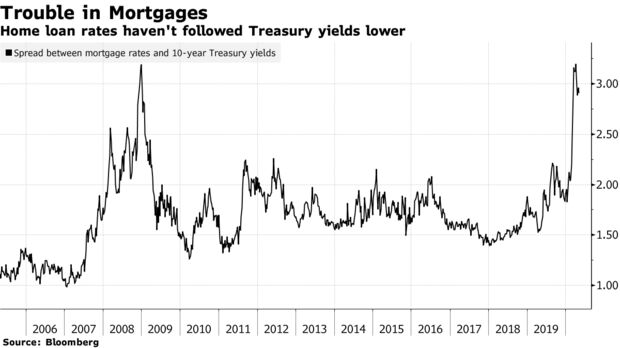

It’s added to strains throughout the industry that have left the gap between mortgage rates and benchmark Treasuries the widest since 2009. Back then, bank failures and concerns about the housing market kept home loans from becoming cheaper for borrowers. Now, it’s obscure parts of the financial world that are holding back efforts to shave thousands of dollars from many Americans’ biggest expenses — their mortgages.

“The Fed came in trying to help, but they overshot,” said Phil Rasori, chief operating officer of Mortgage Capital Trading Inc., which says it handles hedging for about 20% of the mortgage market. He estimates margin calls initially drained as much as $5 billion from lenders before the Fed eased off, posing “an existential threat” to some nonbanks that operate on thin cash cushions, selling off loans as soon as they’re made.

Mortgage lenders promise to lock in interest rates for borrowers weeks before loans are finalized, then hedge that risk by shorting mortgage-related securities. But the Fed’s buying drove up prices for those assets, turning the safeguards into sudden demands for cash. Quicken, among the largest U.S. mortgage lenders, met its obligations during the period, spokesperson John Perich said.

“Every responsible lender hedges their interest-rate risk,” with money shifting daily to keep the contracts in parity, Perich said. “The significant price fluctuations in March meant that large margin balances flowed back and forth between lenders and broker-dealers. Quicken Loans was able to easily meet these obligations thanks to our fortress balance sheet — thus enabling us to continue originating record volumes.” He declined to comment on the size of the margin call Quicken received.

In a sign of the concern among investors, Quicken’s two 10-year bonds traded below 91 cents on the dollar in late March, from above par at the end of February. Those prices have mostly recovered, with both trading around 98 cents on Friday. For a time, market turbulence prompted lenders including Quicken to stop offering rate locks near the start of the mortgage process. Perich said that standard practice is resuming at Quicken.

As the coronavirus pandemic sent global markets into a tailspin, the Fed slashed interest rates almost to zero and embarked on a series of programs to pump cash into markets, opening up lending facilities and buying assets ranging from Treasuries to risky corporate debt. Mortgage bonds were among the first it targeted.

The opportunity to refinance into a cheaper rate is now grabbing headlines. But the trend captivating Wall Street is the canyon between the U.S. government’s cost of borrowing money and rates offered to homeowners. Normally, 10-year U.S. Treasuries set the tone for 30-year mortgages, but the gap between them is now 2.9 percentage points, near levels last seen in late 2008 and early 2009. In the last five years, it’s averaged closer to 1.74.

Consumers could grab rates as low as 2.25% on traditional 30-year government-backed mortgages if markets were behaving normally, according to Optimal Blue LLC, whose software is used by much of the industry. Bankrate.com was showing average rates above 3.5% on Friday.

The Fed’s aim is to support the smooth functioning of mortgage-securities markets so that American households can benefit from lower rates, Lorie Logan, who leads the central bank’s open-market operations desk in New York, said in a speech last month. She cautioned that the Fed’s support doesn’t mean “restoring every aspect of market functioning to its level before the coronavirus crisis.” A spokesperson for the New York Fed had no additional comment.

In interviews, executives at mortgage lenders, service providers and across the securitization industry said the margin calls created enormous tensions. The need to pony up cash set off a stampede by nonbank lenders to finish up loans and get them off their books. But to do that, they needed help from other parts of the industry facing their own challenges amid the pandemic.

Several senior executives said the impact of margin calls is abating but will continue to be felt through June, when mortgages from the spring are finally closed and sold. In the meantime, that means less competition to drive down rates.

United Wholesale Mortgage, one of the country’s biggest home loan providers, agreed to make a record number of loans in March but pulled back in April in response to the market turbulence, said Alex Elezaj, the company’s chief strategy officer. It cut underwriting time from a few days to just hours so it could close loans as quickly as possible.