Monetary policy is not expansionary despite widespread belief otherwise.

The general assumption by the Federal Reserve is that by providing excess reserves to the banking system, the banks would then lend to businesses and individuals to expand economic activity. Furthermore, as discussed previously, the Federal Reserve’s entire premise of inflating asset prices was the subsequent boost to economic activity from an increased “wealth effect.”

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate the most recent action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.” – Ben Bernanke

However, after more than a decade of “monetary policy,” there is little evidence that supports those claims. Instead, there is sufficient evidence that “monetary policy” leads to greater wealth inequality and slower economic growth.

Prima Facie Evidence

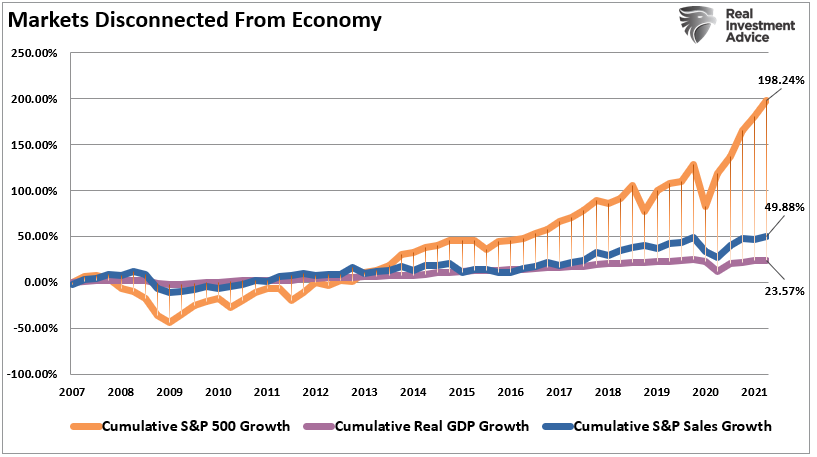

The only reason Central Bank liquidity “seems” to be a success is when viewed through the lens of the stock market. Through the end of Q2-2021, using quarterly data, the stock market has returned almost 198% from the 2007 peak. Such is more than 8x the GDP growth and 3.9x the increase in corporate revenue. (I have used SALES growth in the chart below as it is what happens at the top line of income statements and is not AS subject to manipulation.)

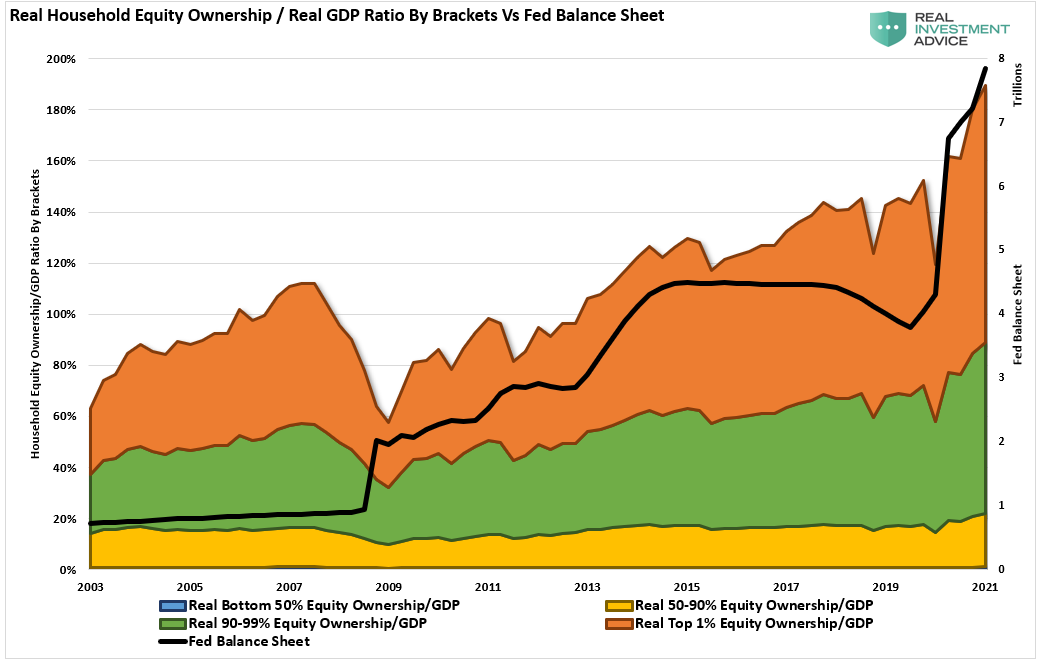

Unfortunately, the “wealth effect” impact has only benefited a relatively small percentage of the overall economy. Currently, the top 10% of income earners own nearly 90% of the stock market. The rest are just struggling to make ends meet. Thus, the impact of the Fed’s monetary interventions on the equity value of the top 1% is evident.

While short-term ongoing monetary interventions may appear to be expansionary, it creates negative incentives to economic activity and monetary velocity.

QE Has A Negative Incentive

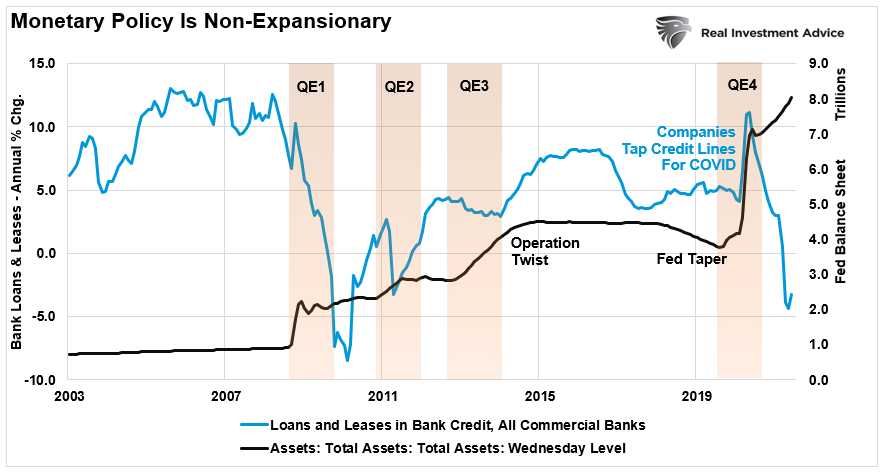

As noted above, the Fed suggests that by providing excess reserves to the banking system, the banks will then “lend” those reserves. In turn, as businesses borrow money to expand production or consumption, the economy gets a lift.

However, in reality, it is precisely the opposite. Each time the Fed has engaged in QE programs, the banks “hoard” those reserves as the “risk/reward” of loaning money into the economy is not justified. For example, in early 2020, as the economy was “shut down” due to the COVID pandemic, companies tapped credit lines at their banks to ensure sufficient capitalization. After that initial surge in lending activity, banks reversed back into a more “protectionary” mode.

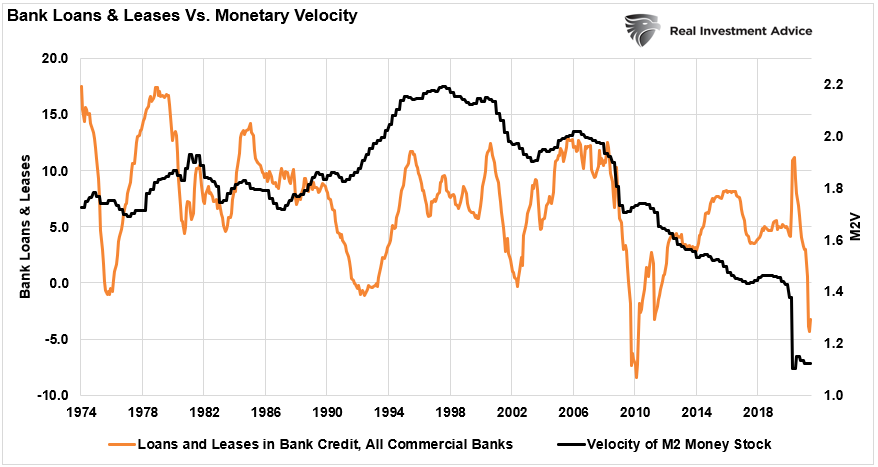

Another way to view the same is by looking at monetary velocity. Monetary velocity, or M2V, measures the rate at which money (M2) moves through the economy (GDP). As shown, velocity continues to plummet despite the banks contracting their lending.

Such is not surprising given that 80% of the population are living primarily paycheck to paycheck. The risk of repayment and defaults remains a disincentive to lend.

Fed Actions Are Disinflationary

Another thesis that requires correcting was summed up well in a recent email question.

“Given the Fed is buying 100% of the Treasury bills plus other bonds at auction…I believe the Fed is manipulating bond yields lower.” – T. Stephenson

The problem for the Federal Reserve is that the fiscal and monetary stimulus imputed into the economy is, in reality, “dis-inflationary.”

“Contrary to the conventional wisdom, disinflation is more likely than accelerating inflation. Since prices deflated in the second quarter of 2020, the annual inflation rate will move transitorily higher. Once these base effects are exhausted, cyclical, structural, and monetary considerations suggest that the inflation rate will moderate lower by year end and will undershoot the Fed Reserve’s target of 2%. The inflationary psychosis that has gripped the bond market will fade away in the face of such persistent disinflation.” – Dr. Lacy Hunt

While the economic growth rate may be booming momentarily, inflation, which is destructive when not paired with rising wages, will be transient. Given the massive surge in prices for homes, autos, and food, the reversal will cause a substantial disinflationary drag on economic growth.

The most considerable risk is a divergence among Fed policymakers which possibly leads to a policy mistake of tapering too quickly or even hiking rates.

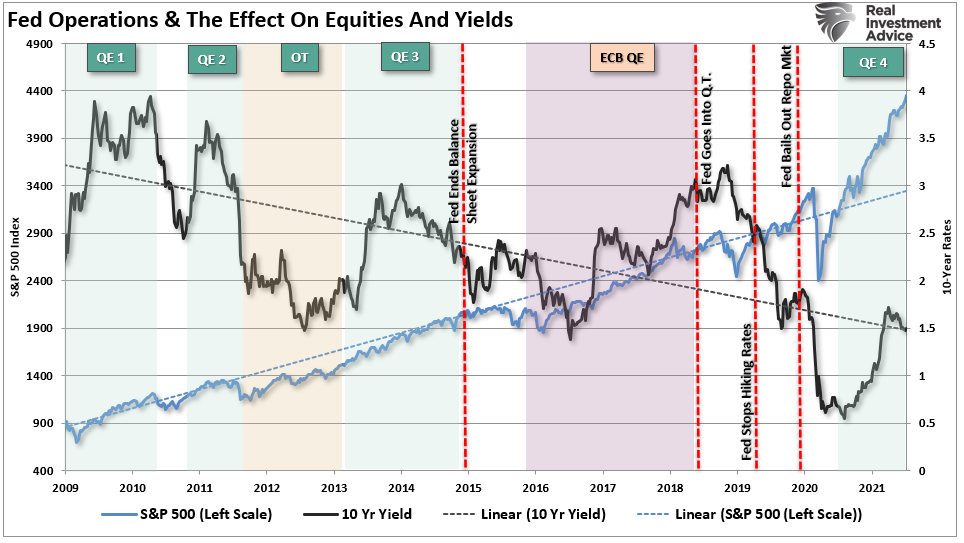

Fed Buying Drives Rates Higher

The majority of the inflation and economic growth pressures are artificial, stemming from the stimulus injections over the last year. However, with those inputs fading as year-over-year comparisons become more challenging, the “deflationary” impact could be more significant than expected.

There is also one other point about the Fed tapering the purchases. As shown in the chart below, rates rise during phases of QE as money rotates from bonds to stocks for the “risk-on” trade. The opposite occurs when they start to taper, suggesting a decline in rates if “taper talk” increases.

Such is because, after more than a decade of monetary interventions, the Fed has created a “psychological” link between “QE” and the equity markets. As a result, the liquidity provision creates an asset preference of “risk-on” assets, equities, versus “risk-off” assets, bonds.

(It is also worth noting the massive current deviation of the equity market from the liner growth trend.)

The result is that during QE programs, interest rates rise due to the psychological impact of asset preference.

Fed Requires Debt Issuance

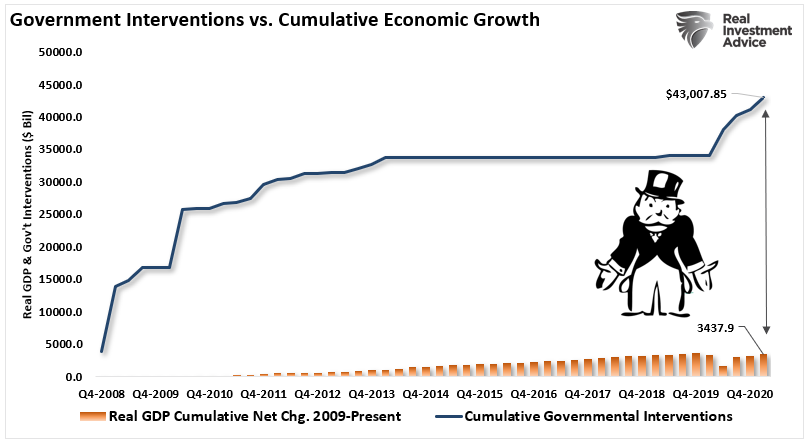

Of course, the Federal Reserve requires debt issuance by the Government to facilitate Quantitative Easing. Since the “Financial Crisis,” total Government interventions surpassed $43 Trillion into the economy to keep it “afloat.”

I say “afloat” rather than “growing” because, since 2008, the total cumulative growth of the economy is just $3.5 trillion. In other words, for each dollar of economic growth since 2008, it required $12 of monetary stimulus. Such sounds okay until you realize it came solely from debt issuance.

Government Spending Has A Negative Multipler

Here is the problem. Excess “debt” has a zero to a negative multiplier effect. Such was shown in a study by the Mercatus Center at George Mason University by economists Jones and De Rugy.

“The multiplier looks at the return in economic output when the government spends a dollar. If the multiplier is above one, it means that government spending draws in the private sector and generates more private consumer spending, private investment, and exports to foreign countries. If the multiplier is below one, the government spending crowds out the private sector, hence reducing it all.

The evidence suggests that government purchases probably reduce the size of the private sector as they increase the size of the government sector. On net, incomes grow, but privately produced incomes shrink.”

Notably, politicians spend money based on political ideologies rather than sound economic policy. Therefore, the findings should not surprise you. However, the conclusion of the study is most telling.

“If you think that the Federal Reserve’s current monetary policy is reasonably competent, then you actually shouldn’t expect the fiscal boost from all that spending to be large. In fact, it could be close to zero.

This is, of course, all before taking future taxes into account. When economists like Robert Barro and Charles Redlick studied the multiplier, they found once you account for future taxes required to pay for the spending, the multiplier could be negative.”

Monetary policy, in its current form, is not helping the economy. As a result, the Federal Reserve has lost the ability to influence economic growth.

Conclusion

The Federal Reserve has no real options unless they are willing to allow the system to reset painfully.

Unfortunately, we now have a decade of experience of watching monetary experiments only succeed in creating a massive “wealth gap.”

Most telling is the current economists’ inability to realize the problem is trying to “cure a debt problem with more debt.”

In conclusion, the Keynesian view that “more money in people’s pockets” will drive up consumer spending, with a boost to GDP being the result, has been wrong. It hasn’t happened in 40 years.

The reality is that monetary policy is not expansionary but rather contractionary. Unfortunately, deflation remains the most significant threat as permanent growth doesn’t come from an artificial stimulus or debt.

But such is a lesson that has yet to get learned.