via mishtalk:

The Black Knight Mortgage Monitor shows the first annual rise in defaults since the crisis.

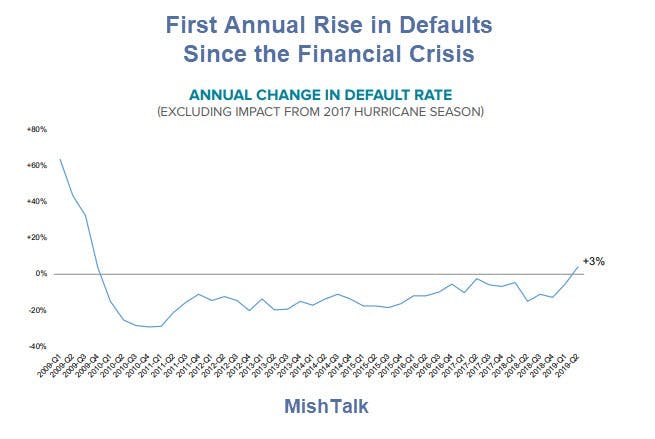

First Lien Defaults by Quarter

- An estimated 243K borrowers defaulted on first lien mortgages in Q2 2019

- While the quarter ending on a Sunday certainly played a factor in the rise in defaults, a noticeable overall slowdown in the decline in default activity has been observed.

- The national default rate rose by 3% compared to Q2 2018, the first such annual rise since the financial crisis (adjusting for the 2017 hurricane season)

Delinquencies

- The national delinquency rate fell by 7% in July, offsetting the bulk of June’s calendar-related spike

- At 3.46%, July 2019’s delinquency rate is the lowest of any July on record (dating back to 2000)

- Serious delinquencies (all loans 90 or more days delinquent but not in active foreclosure) fell below 445,000 for the first time since June 2006

- Despite the Q2 year-over-year rise in defaults, overall seriously delinquent inventory (loans 90 or more days past due) is down by 17% from last year due to continued strong cure activity

Refinancing Stats

- Prepayment activity jumped 26% from June to its highest level in nearly three years and 58% above this time last year as falling interest rates continue to fuel refinance incentive

- There are now 9.7M refinance candidates in the market.

- Rates have since fallen to 3.50% near a two-and-a-half year low, resulting in the most refinance incentive in the market since late 2016

Notes

The above Black Knight chart and bullet points contain some unpublished numbers. Those bullet points do not match the link at the top.

Black Knight was gracious enough to send me an updated numbers and an unpublished chart.

Refinance Candidates Under Different Interest Rate Scenarios

Another 1/8 point decline in rates would increase the number of refinance candidates by 1.5M to 9.7M – a 18% rise in refi incentive.

Likewise, a 1/8 point increase in the 30-year rate would decrease the number of refinance candidates by 1.3M to 6.9M, a 16% decline.

Refinance Comments from Raymond James’ Director of Agency Trading

Steven Childress, Managing Director of Agency MBS Trading, at Raymond James offered these thoughts on refinancing.

- Just looking at the number of refinance-eligible loans in the money is not the best way to look at refinance eligibility. It’s better to consider how much is in the money as a percentage what is outstanding.

- Outstanding has grown to ~6.5 trillion in just fixed MBS (FNMA/FGLMC/GNMA). However, today’s raw number is a smaller percentage.

- The vast majority of eligible refis are from 2018 production, when new loans were put on at higher rates. And even though they are now in the money, it doesn’t mean people will actually refinance.

- A refinance boom could happen, but the impact may not be as great as the raw eligibility numbers imply.

Affordability Illusions

Black knight says falling interest rates make homes more “affordable”.

“The decline in 30-year rates has been equivalent to a 15% increase in buying power, meaning that prospective homebuyers shopping for the average priced home could now pay $45,000 more for a home than last fall while keeping monthly payments the same.”

Let’s not confuse monthly payments with what a house is worth. A home is not worth $45,000 more (or less) based on what the interest rate is.

Moreover, and very importantly, home price increases have far outstripped wages.

Housing Bubble Reblown

The Fed re-blew the housing bubble. The Last Chance for a Good Price Was 7 Years Ago.

“Affordability” based on declining interest rates is an illusion.

People shy away from buying homes for one primary reason: sticker shock. They cannot afford the asking prices.

Interest rates have a minor role.

Thanks to Black Knight, Raymond James

Affordability issues aside, Black Knight puts out a solid set of stats every month.

Also, thanks to Steven Childress at Raymond James.

Mike “Mish” Shedlock